In the high-stakes arena of global biopharmaceuticals, cash is king, but timing is everything. As Eli Lilly and Company announces its bold move to acquire CAR-T innovator Kelonia Therapeutics in a deal valued at up to $7 billion, the industry is watching with a mixture of admiration and trepidation.

Lilly, currently riding an unprecedented wave of success fueled by its tirzepatide franchise, is aggressively deploying its newfound capital to build a diversified, next-generation pipeline. However, the move invites an inevitable comparison to Pfizer’s $43 billion acquisition of Seagen—a deal that, while strategically sound on paper, became emblematic of a "post-COVID hangover" as the company struggled to integrate massive assets while its primary revenue drivers cratered. Can Lilly avoid the "Pfizer trap," or is it destined to navigate the same turbulent waters?

The Core Facts: Lilly’s Strategic Pivot

Eli Lilly’s acquisition of Kelonia marks a significant expansion into in vivo CAR-T cell therapies. By leveraging Kelonia’s proprietary technology, Lilly aims to simplify the delivery of complex cancer therapies, moving away from the laborious, expensive, and time-consuming ex vivo manufacturing processes that currently limit the reach of cell therapy.

This acquisition is not an isolated event. It is part of a broader, deliberate strategy to reinvest the windfall generated by its metabolic blockbuster, tirzepatide (marketed as Mounjaro and Zepbound). Beyond Kelonia, Lilly has recently inked a potentially $2.75 billion collaboration with Insilico Medicine to harness AI-driven drug discovery for preclinical oral therapeutics. These moves signal a transition from a company defined by a single category—obesity and diabetes—to a diversified powerhouse looking toward the next decade of oncology, immunology, and genetic medicine.

Chronology of a Growth Spree

To understand the current trajectory, one must look at the timeline of capital deployment.

- 2022–2023: The COVID Era Divergence. While Pfizer was aggressively spending its record-breaking COVID-19 windfall on late-stage assets like Seagen, Biohaven, and Global Blood Therapeutics, Lilly was quietly scaling its manufacturing capacity for tirzepatide.

- 2024: Building the Foundation. Lilly began its current M&A wave by acquiring Morphic Therapeutic for $3.2 billion, signaling a deeper commitment to gastrointestinal and immunology research.

- 2025: Expanding the Reach. The company continued its trend of targeting earlier-stage, high-potential platforms, including deals with Scorpion Therapeutics (up to $2.5 billion), Verve Therapeutics (approx. $1.3 billion), and SiteOne Therapeutics (up to $1.0 billion).

- 2026: Scaling and Diversification. The Kelonia acquisition and the Insilico partnership underscore a move toward more complex, "platform-based" biotech assets. Simultaneously, the FDA’s approval of Foundayo (orforglipron) on April 1, 2026, provided a critical oral growth vector, further solidifying the company’s dominance in metabolic health.

Supporting Data: The Tale of Two Giants

The divergence between Lilly’s current strategy and Pfizer’s recent struggles is best illustrated by the financial metrics of their respective deal-making cycles.

Revenue Dynamics

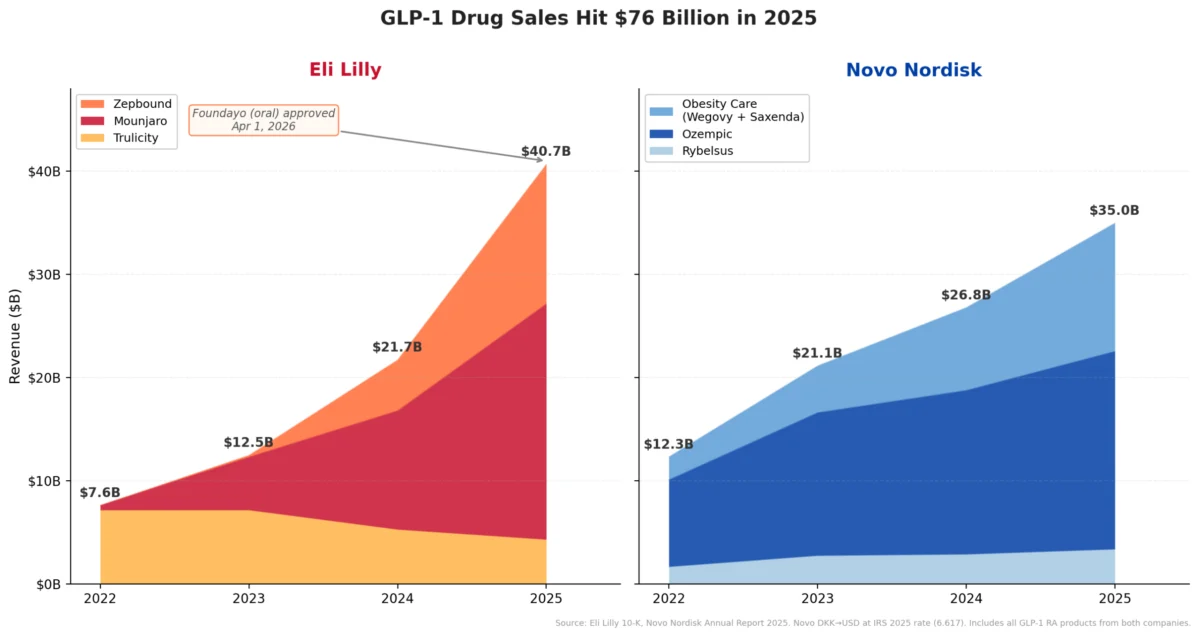

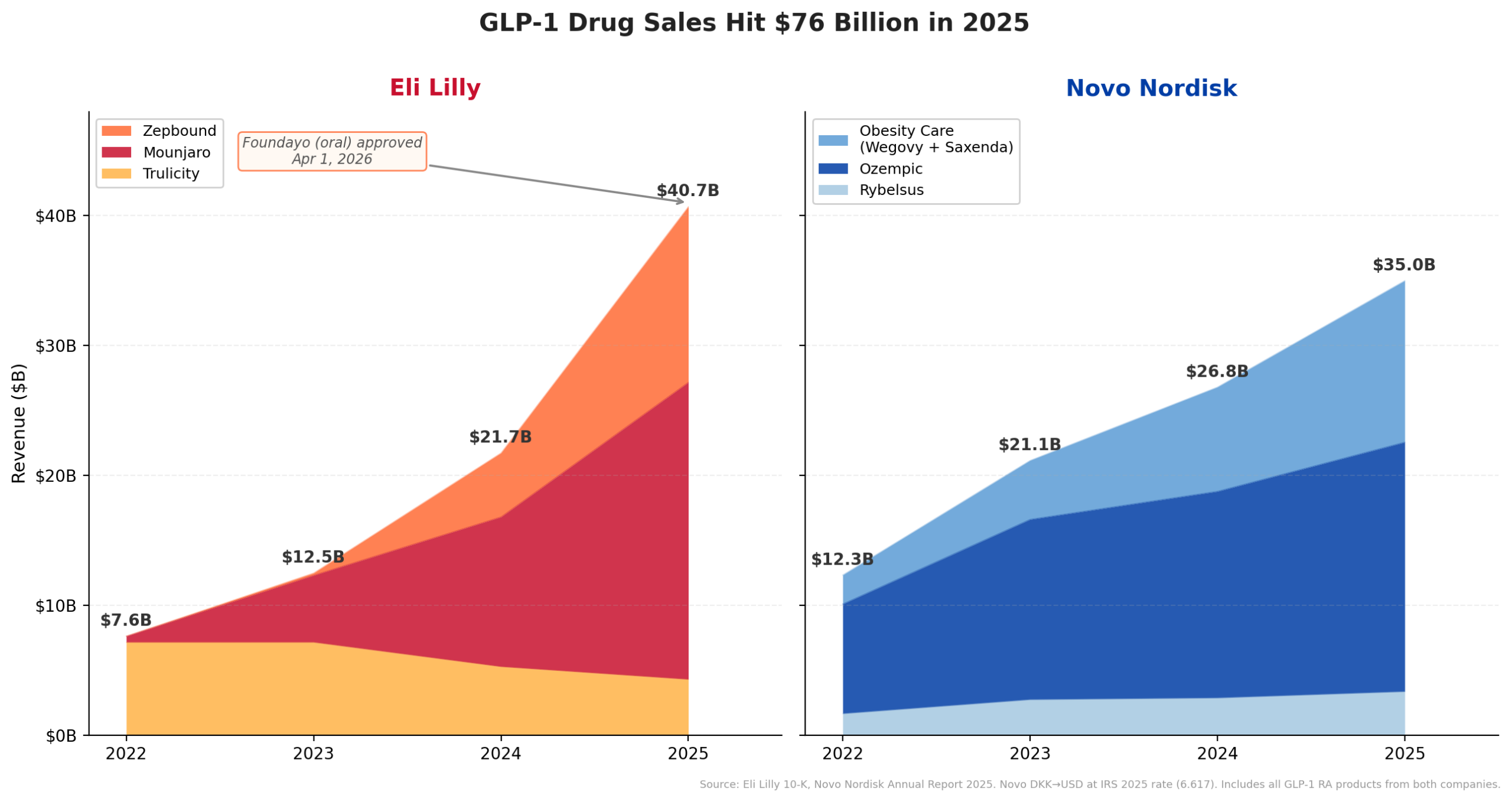

Lilly’s tirzepatide franchise has shown exceptional momentum. In 2025, tirzepatide generated approximately $36.5 billion of the company’s $65.2 billion total revenue. Projections for 2026 suggest revenue will climb to between $80 billion and $83 billion. Conversely, Pfizer’s revenue collapsed from $100.3 billion in 2022 to $58.5 billion in 2023, as demand for Comirnaty and Paxlovid plummeted. Pfizer was buying assets to replace a disappearing revenue cliff; Lilly is buying assets to leverage a revenue mountain.

The Acquisition Profile

Lilly’s strategy focuses on "platform bets"—mostly Phase 1 and Phase 2 assets—aimed at long-term innovation. Pfizer, by contrast, prioritized "commercial-ready" or late-stage assets. While this gave Pfizer immediate revenue streams, it also carried the heavy burden of high purchase premiums and the risk of immediate market stagnation.

| Metric | Eli Lilly (Current) | Pfizer (Post-COVID) |

|---|---|---|

| Cash Engine | Growing (Tirzepatide) | Declining (COVID Products) |

| Primary M&A Focus | Early-stage, Platform | Late-stage, Commercial |

| Market Cap (Apr 2026) | ~$830B – $880B | ~$155B |

| Operational Cash Flow | ~$16.8B (FY2025) | ~$11.7B (FY2025) |

Official Responses and Industry Outlook

In recent investor communications, Lilly management has emphasized that their M&A strategy is dictated by "scientific synergy" rather than "revenue replacement." By investing in the Kelonia platform, the company is betting on the future of manufacturing, effectively attempting to solve the bottleneck of cell therapy delivery before they even enter the commercial phase.

Analysts remain generally optimistic, noting that Lilly’s "durable playbook" is fundamentally different from that of its closest rival, Novo Nordisk. While Novo Nordisk is currently projecting a 5% to 13% decline in adjusted sales as it struggles with supply constraints and market saturation, Lilly is aggressively launching new delivery formats, such as the oral GLP-1 Foundayo, which is priced at an accessible $149/month for the lowest dose.

Implications: Can Lilly Avoid the "Pfizer Fate"?

The "Pfizer Fate" refers to the dilution of shareholder value and the operational fatigue caused by integrating massive, high-cost acquisitions during a period of declining core revenue. For Lilly, the risk is different.

1. The Risk of Over-Extending

By focusing on early-stage, platform-based biotech, Lilly faces the risk of high attrition rates. Unlike buying a product with an existing FDA approval, an early-stage CAR-T platform may take years to yield a viable, scalable, and safe drug. If the technology fails, billions in acquisition costs could be written down as goodwill impairments.

2. The Power of the "Oral" Pivot

The approval and rollout of Foundayo is perhaps the most significant hedge against the future. By offering an oral alternative to the injectable tirzepatide, Lilly is not just selling a drug; it is creating a lifecycle management system that can dominate the obesity market for decades. This allows them to use their cash for M&A without the frantic desperation that characterized Pfizer’s post-COVID shopping spree.

3. The AI Integration

The partnership with Insilico Medicine is a signal that Lilly is not just buying pipelines; it is buying efficiency. If AI can successfully shorten the drug discovery cycle—a notoriously expensive and slow process—Lilly could theoretically generate a higher Return on Invested Capital (ROIC) than any other firm in the history of the industry.

4. Cultural Integration

The biggest hidden danger for any company on a "buying run" is cultural dilution. Integrating a small, nimble startup like Kelonia into a massive, multi-national corporation requires surgical precision. Pfizer struggled with the sheer scale of the Seagen integration; Lilly’s challenge will be maintaining the innovation-first culture of its acquired biotech units while leveraging its massive global manufacturing and regulatory infrastructure.

Conclusion: A New Era of Pharma

Lilly’s current strategy suggests that it has learned the primary lesson of the last five years: don’t wait for the revenue to stop growing before you decide what comes next. By investing while its core business is at its absolute peak, Lilly is effectively "buying the future" at a time when its balance sheet can withstand the volatility of clinical development.

Whether this culminates in a transformation into a diversified powerhouse or a cautionary tale of over-diversification remains to be seen. However, given the current financial metrics—with Lilly boasting a market cap that dwarfs its peers—the company has arguably bought itself the luxury of being wrong a few times. As the pharmaceutical sector watches the Q1 2026 earnings release due on April 30, the primary question will be whether the market believes these early-stage bets can eventually replace the massive success of the GLP-1 era. For now, the "Lilly Playbook" remains the gold standard for navigating the complex intersection of massive success and future-proofing.