For decades, Medicare has served as the bedrock of the American social safety net, promising peace of mind to millions of citizens as they transition into retirement or navigate life with long-term disabilities. However, a stark reality is emerging: for a significant portion of the 70 million Americans currently enrolled in the program, Medicare is no longer the ironclad financial shield it once was. As health care costs continue to outpace inflation and savings, beneficiaries are increasingly finding themselves caught in a vice of rising premiums, high out-of-pocket expenses, and the crushing weight of medical debt.

According to recent polling from KFF, health care costs and affordability have surged to the top of the public’s list of economic anxieties. Perhaps most alarming is that this concern is not limited to the uninsured; even those with comprehensive Medicare coverage are reporting significant difficulty in accessing necessary care due to financial constraints. With nearly half (49%) of Medicare beneficiaries aged 65 and older telling KFF they expect their health care to become even less affordable in the coming year, the program is facing a reckoning that threatens the financial stability of the nation’s most vulnerable populations.

The Economic Reality: Low Incomes and Modest Savings

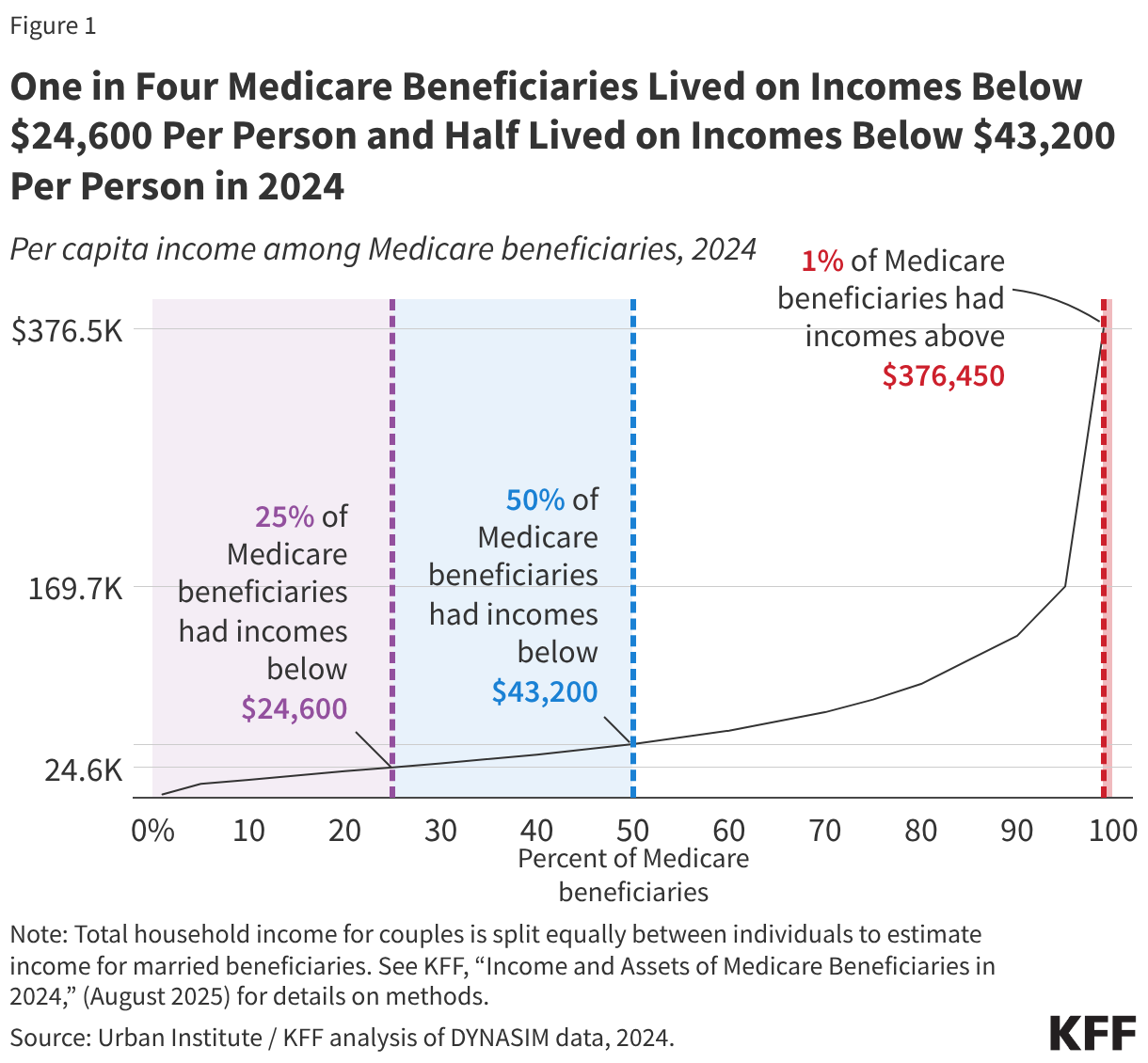

The assumption that all seniors enter retirement with significant nest eggs is a dangerous misconception. Data from 2024 reveals a sobering picture: one in four Medicare beneficiaries lives on an annual income below $16,600, and half subsist on less than $32,200. When these figures are weighed against the rising costs of modern medical care, the margin for error effectively vanishes.

Many beneficiaries rely almost exclusively on Social Security for their survival. For these individuals, a sudden health event—or even the incremental rise in Medicare Part B premiums—can trigger a cascade of financial instability. When a household’s fixed income is already stretched thin by housing, food, and utilities, the "surprise" costs of deductibles and coinsurance become insurmountable barriers to care.

Chronology of the Affordability Gap

The current crisis is not a sudden phenomenon but the culmination of years of structural shifts in the healthcare landscape:

- Pre-2010s: Medicare costs remained relatively stable, and the primary concern for beneficiaries was the "donut hole" in prescription drug coverage.

- 2015–2020: The rise of Medicare Advantage (MA) plans began to reshape the market. While MA offered lower upfront premiums and out-of-pocket maximums, it introduced complex network limitations and pre-authorization hurdles.

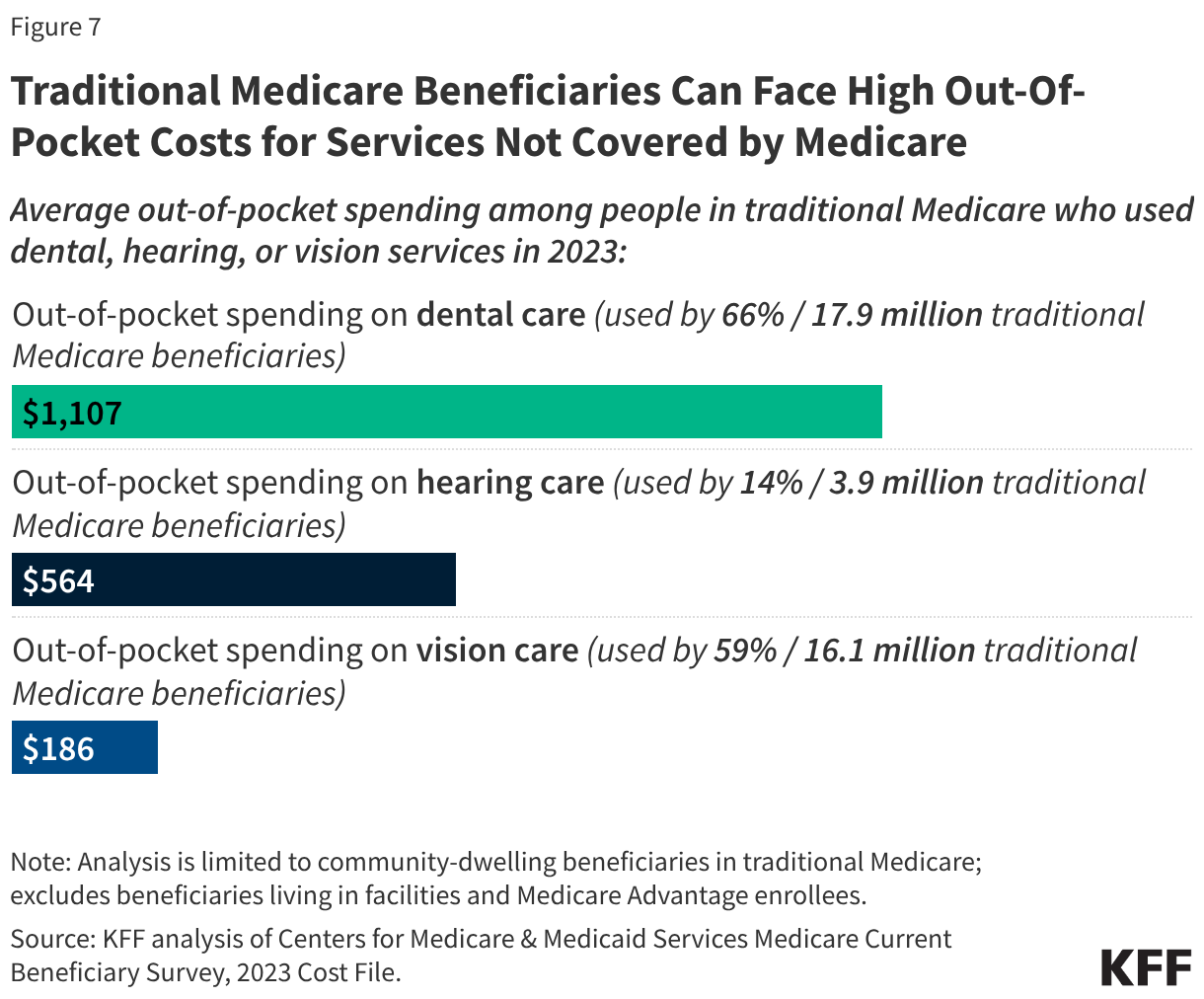

- 2021–2024: Post-pandemic inflation and the rising cost of medical technology and labor began to push health expenditures significantly higher. Traditional Medicare beneficiaries faced growing costs for services not covered by the program, such as vision, dental, and hearing.

- 2025–Present: The gap between fixed incomes and healthcare spending has reached a critical inflection point. Projections now suggest that between 2026 and 2034, premiums and deductibles for Part B could climb by approximately 70%, creating a trajectory that many believe is unsustainable for the average retiree.

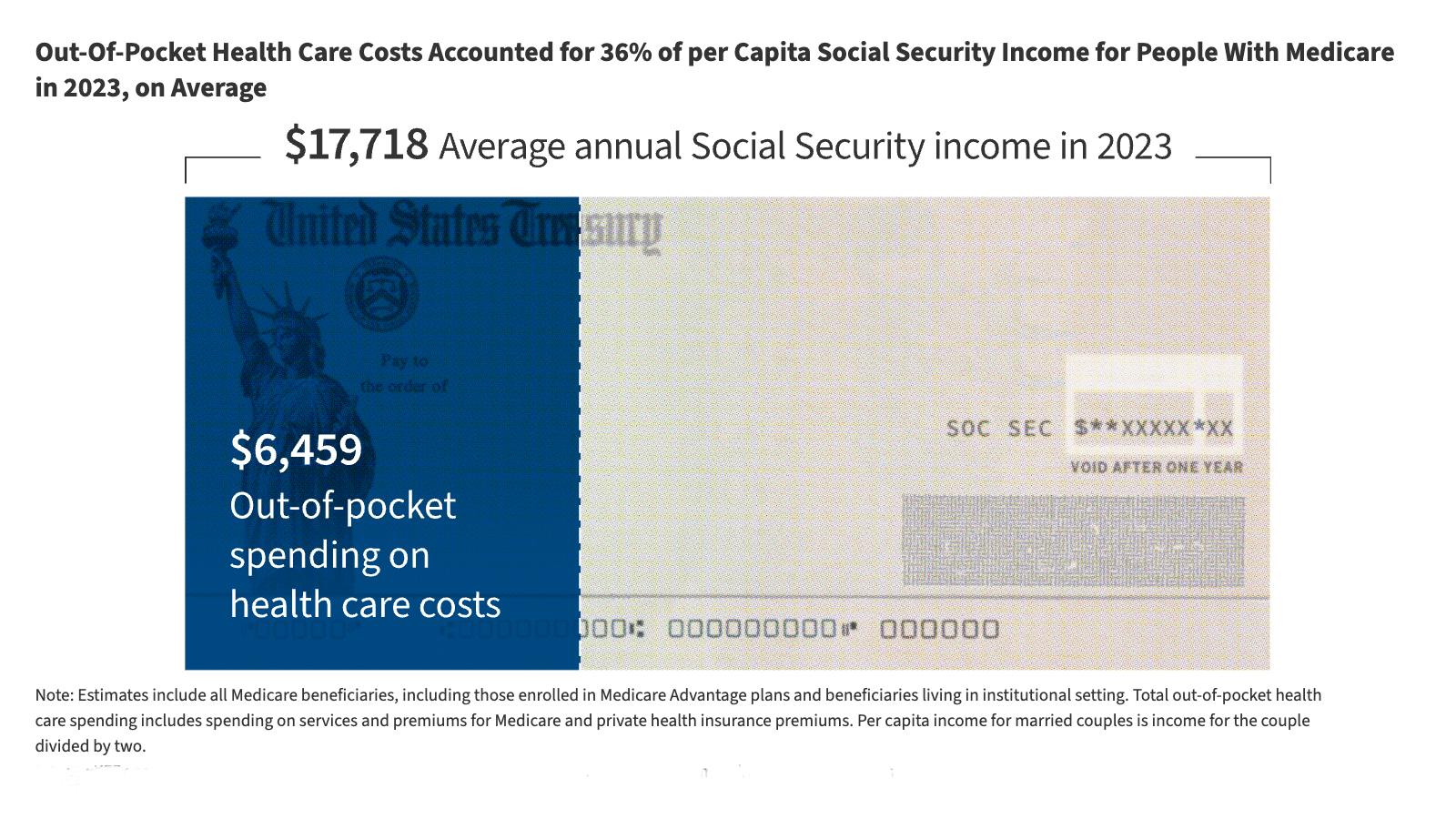

Supporting Data: The Burden of Out-of-Pocket Expenses

The financial burden of Medicare is multifaceted, encompassing everything from basic premiums to the lack of coverage for long-term support services.

The Trade-offs of Coverage

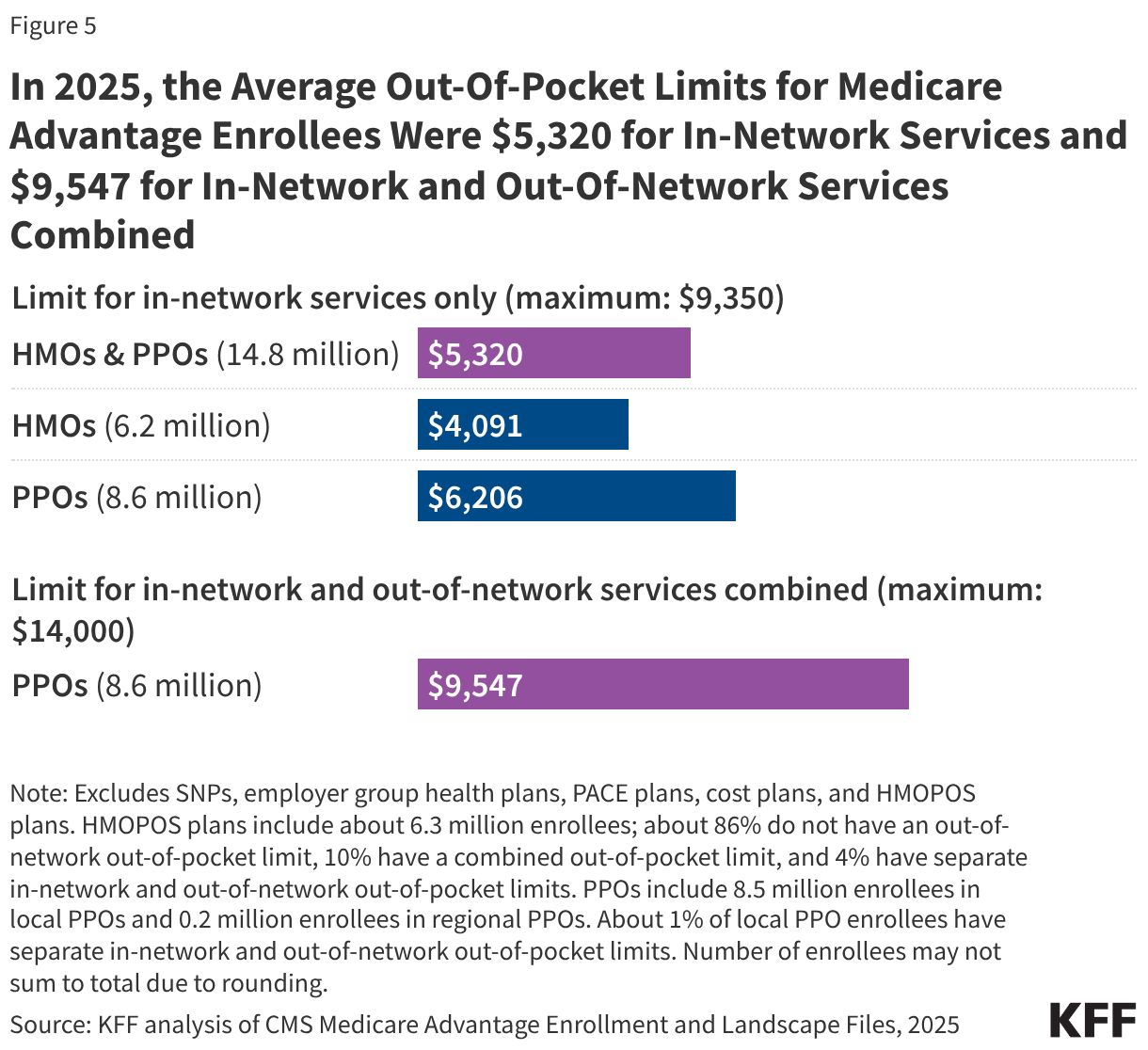

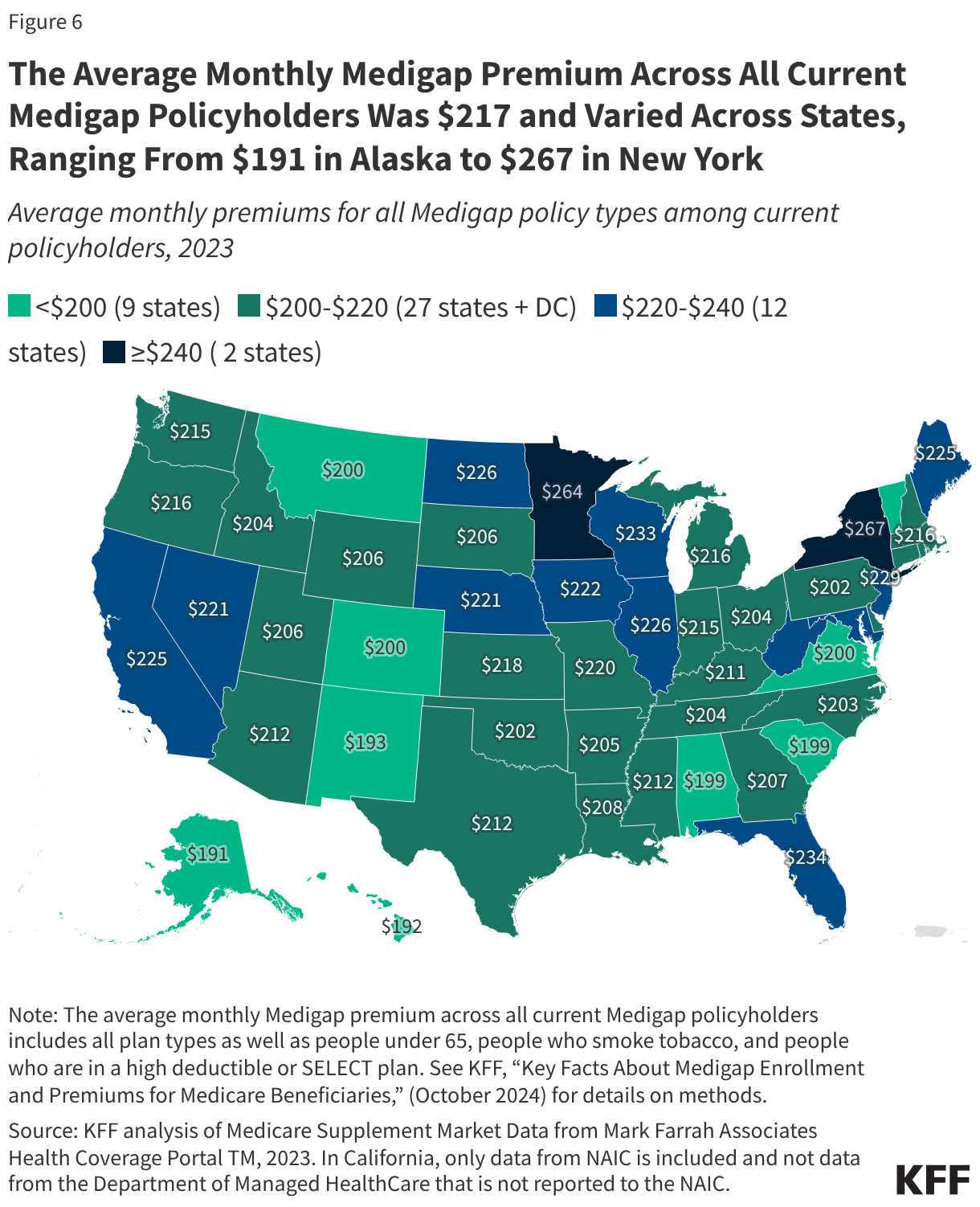

Beneficiaries are forced into a difficult choice between Traditional Medicare and Medicare Advantage. While Medicare Advantage plans provide an out-of-pocket maximum—averaging $2,320 for in-network services in 2025—this comes at the cost of narrower provider networks. Conversely, those who stick with Traditional Medicare often seek "Medigap" (supplemental) insurance to cover the gaps. However, Medigap premiums vary wildly by state and health status, adding another layer of financial volatility to a senior’s monthly budget.

The "Non-Covered" Trap

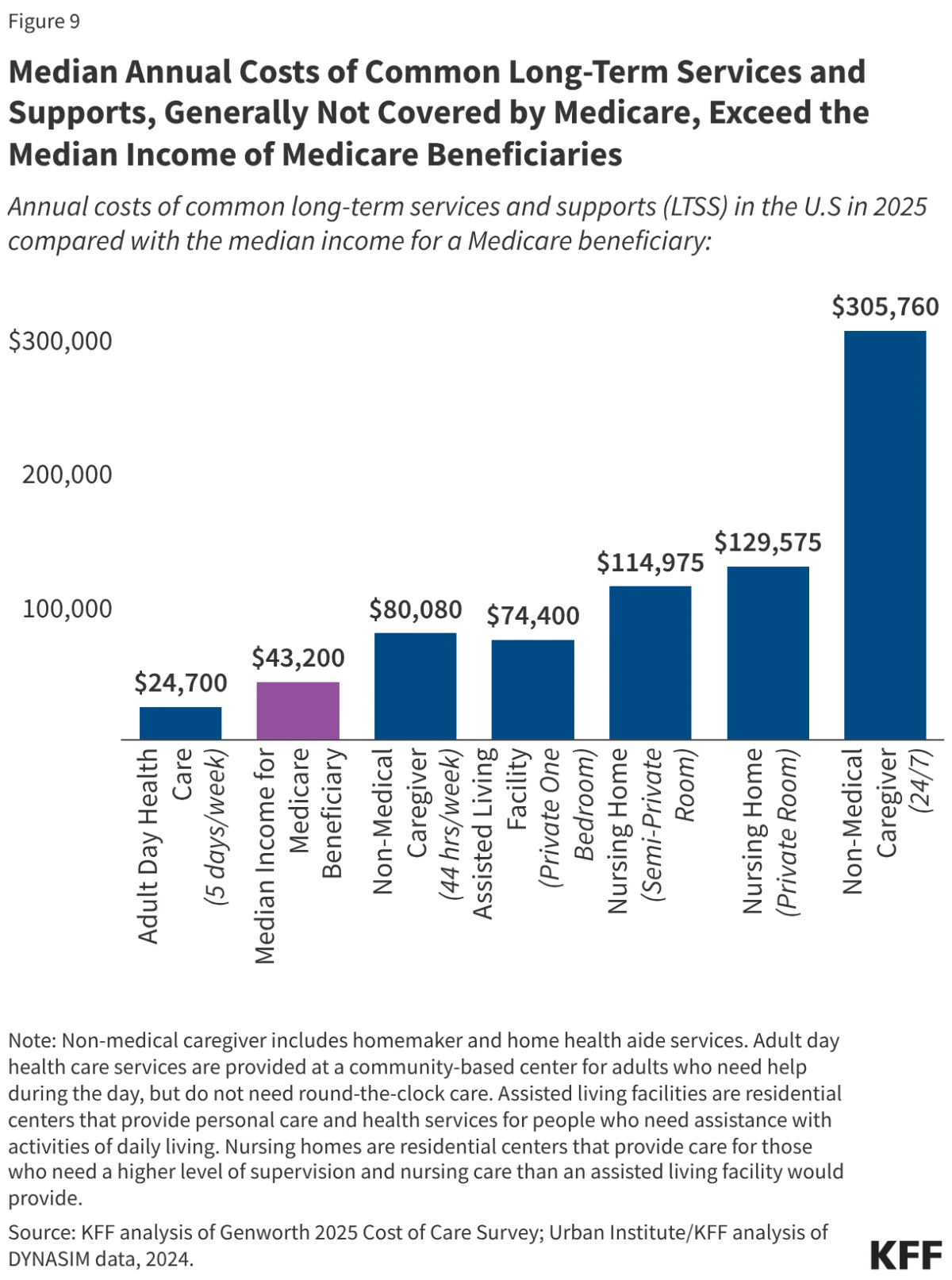

One of the most persistent issues remains the services Medicare simply does not cover. Long-term care, dental, vision, and hearing services are often left to the beneficiary to fund entirely out-of-pocket. The median annual costs for these long-term services now frequently exceed the median annual income of a Medicare beneficiary, effectively trapping many in a state of perpetual financial distress.

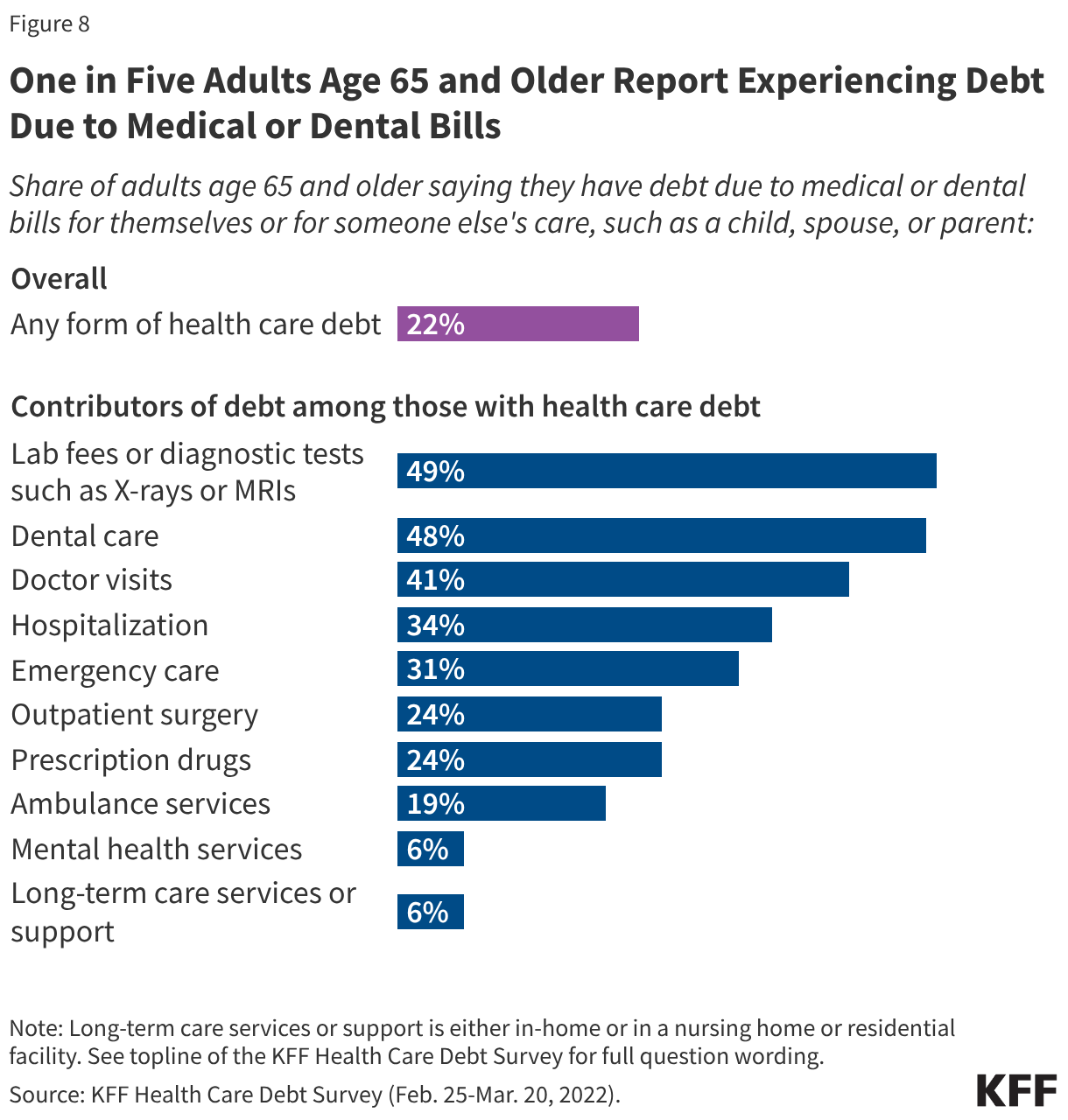

Furthermore, medical debt has become a widespread epidemic. One in five adults aged 65 and older now reports carrying debt related to medical or dental bills. This is not merely a "bill" issue; it is a health issue. When seniors are forced to choose between paying for heart medication and paying for groceries, they often ration their care, leading to poorer health outcomes and, ironically, higher system-wide costs in the long run.

Official Responses and the Role of Medicaid

The federal government has acknowledged the strain through the existence of the Medicare Savings Programs (MSPs), which allow Medicaid to bridge the gap for approximately 12 million low-income beneficiaries. Medicaid provides crucial "wraparound" support, covering premiums, deductibles, and co-pays that Medicare recipients would otherwise be unable to afford.

However, enrollment in these programs is often hampered by bureaucratic hurdles, confusing eligibility criteria, and the persistent stigma associated with public assistance. Policy experts argue that until these programs are streamlined and made more accessible, millions of eligible seniors will continue to fall through the cracks.

Regarding prescription drugs, Medicare Part D continues to offer protection against catastrophic costs, but for those not receiving low-income subsidies, the out-of-pocket burden remains high. Patients in fair or poor health, who require more complex medication regimens, spend roughly twice as much as their healthier counterparts, creating a "sickness tax" that penalizes the most vulnerable.

Implications for the Future

The implications of these findings are profound. If the growth in Medicare spending continues at its projected rate, the program risks becoming a source of poverty rather than a source of security.

Policy Shifts

Legislators are under increasing pressure to consider structural reforms. These might include:

- Out-of-Pocket Caps for Traditional Medicare: Unlike Medicare Advantage, Traditional Medicare has no "stop-loss" provision, leaving patients exposed to unlimited costs. Introducing such a cap could prevent financial ruin for those with chronic illnesses.

- Expanding Coverage to Include Dental, Vision, and Hearing: As these are essential components of aging, their exclusion from standard coverage is increasingly viewed as an anachronism.

- Targeted Subsidy Reform: Reforming the low-income subsidy thresholds to reflect the modern cost of living would help those just above the current poverty line who are currently "too rich" for help but "too poor" to afford care.

The Societal Cost

Ultimately, the affordability crisis is not just a line item in a budget; it is a moral test for the American healthcare system. When the elderly are forced to trade their financial independence for access to basic medical services, the social contract is fundamentally broken.

The trajectory of the next decade suggests that without significant intervention, we are heading toward a scenario where the "golden years" of retirement are increasingly overshadowed by the constant, looming threat of medical bankruptcy. Policymakers, healthcare providers, and the public must confront these data points not as abstract statistics, but as an urgent mandate for reform. The stability of the Medicare program is inextricably linked to the stability of the American middle class, and the time to bridge the affordability gap is narrowing.