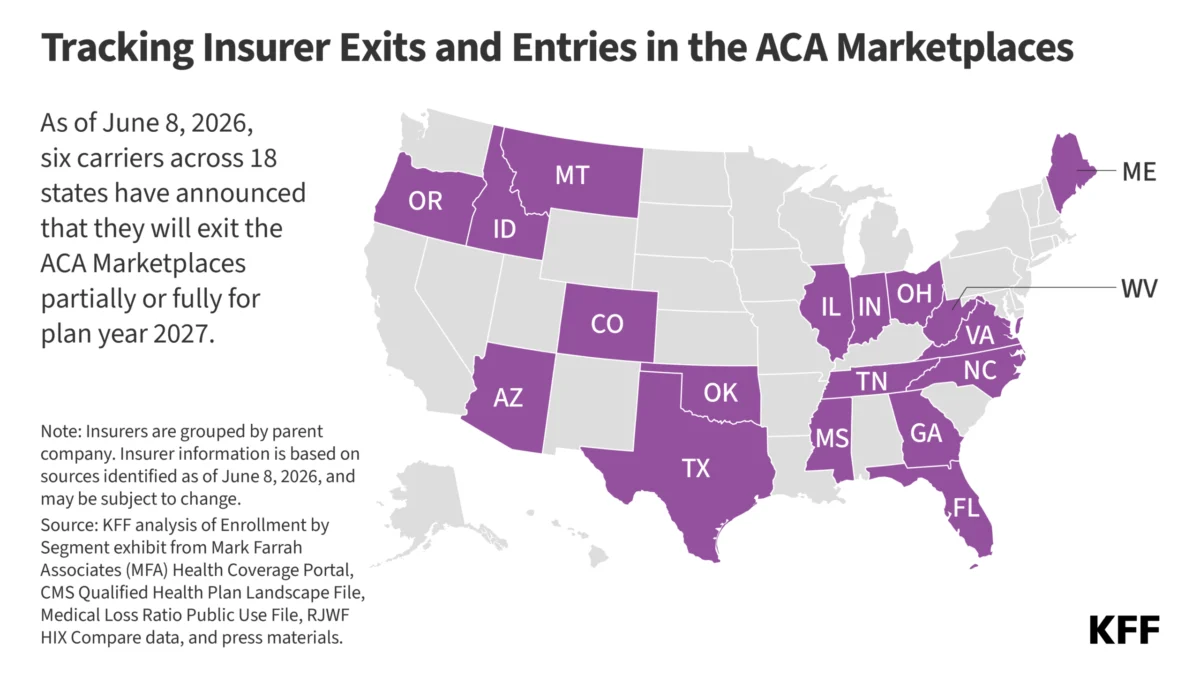

As of June 8, 2026, the landscape of the Affordable Care Act (ACA) Marketplaces is undergoing a significant transformation. A wave of insurer exits has been announced for the 2027 plan year, signaling a pivotal shift in the stability and accessibility of the individual health insurance market. Six major carriers—Cigna Health, CareSource, PacificSource, Scott and White, Providence Health, and Taro Health—have confirmed they will either partially or fully withdraw from Marketplace participation across various states.

This withdrawal, which is projected to impact roughly one-third of the nation, follows a period of mounting volatility characterized by the expiration of enhanced premium tax credits at the end of 2025. These subsidies had previously served as a vital engine for growth, but their lapse has triggered a ripple effect that threatens to reshape the American healthcare ecosystem.

Main Facts: A Market in Transition

The primary catalyst for the current instability is the convergence of policy shifts and market dynamics. The expiration of enhanced subsidies has led to a marked decline in enrollment—a drop of over one million individuals between the 2025 and 2026 Open Enrollment periods. This decline is not merely a statistical anomaly; it represents a fundamental change in the Marketplace’s risk pool.

When healthier enrollees are the first to drop coverage due to rising costs, the risk pool becomes "sicker," leading to higher claims costs for insurers. This, in turn, forces insurers to re-evaluate their financial sustainability within the exchange. For many carriers, the ACA Marketplace has evolved from a growth platform into a stagnant or declining segment of their business portfolios.

Chronology: From Expansion to Retrenchment

To understand the current crisis, one must look at the recent timeline of the ACA Marketplaces:

- 2023–2024: The ACA Marketplaces reached a period of relative maturity and stability, bolstered by high enrollment numbers fueled by expanded federal subsidies.

- December 31, 2025: The expiration of the enhanced premium tax credits marked a turning point. As premiums rose for many, affordability concerns led to a significant exodus of consumers.

- Early 2026: Enrollment figures for the 2026 plan year showed a deficit of over one million participants compared to the previous year.

- 2026 (Ongoing): Aetna CVS Health initiated the trend of major departures, exiting the exchanges.

- June 2026: Six additional carriers, including industry giant Cigna, announced their intention to exit or scale back operations for the 2027 plan year.

This chronology reveals a clear trend: the market is contracting in direct response to the withdrawal of federal fiscal support. While the "bare county" phenomenon—where no insurer offers a plan—remains a concern of the past, the current contraction is shifting toward "choice-limited" markets, where consumers have fewer options and less competitive pricing.

Supporting Data: The Erosion of Competition

The math behind the current crisis is stark. In 2025, the average state boasted 9.6 insurers participating in the ACA Marketplace. By 2026, that figure had already dipped to 9.0, largely due to the exit of Aetna CVS. With the latest round of announcements for 2027, this number is expected to fall further.

Geographic Impact

The withdrawals are not uniform. In states like Indiana, Oregon, and Texas, multiple carriers are pulling out simultaneously. For example, in Indiana, the dual departure of CareSource and Cigna leaves the market with only three remaining providers, assuming no new entrants fill the vacuum.

Enrollment Trends

Cigna’s departure serves as a case study for the broader trend. With over 350,000 individuals enrolled in their on-exchange plans as of early 2026, the company’s decision to exit 11 states is a major blow to consumer choice. The company has explicitly stated that the segment is "shrinking" and no longer aligns with their core growth platforms, illustrating that even for large, diversified health groups, the ACA Marketplace is becoming an increasingly difficult environment in which to turn a profit.

The Lone Exception: New Entrants

Despite the gloom, the market is not entirely stagnant. Colorado Access has signaled its intent to enter the market for 2027. This suggests that while large national carriers are pivoting away, some regional or mission-driven insurers may still see opportunities in specific pockets of the country where local infrastructure and provider networks remain strong.

Official Responses and Strategic Shifts

The decision to exit is rarely taken lightly by insurance executives. In statements to shareholders, representatives from major payers have emphasized a "return to basics."

The Cigna Perspective

Cigna’s leadership, including executives who have spoken on recent earnings calls, have framed the move as a strategic reallocation of capital. By exiting the individual market, Cigna intends to intensify its focus on core growth areas. As one executive noted, "This is small business for us today, and it’s been shrinking in recent years." This admission highlights the friction between the public health goals of the ACA and the fiduciary responsibilities of publicly traded insurance companies.

Regulatory Silence

While the federal government has not yet released a comprehensive policy response to the 2027 exit announcements, there is growing pressure on policymakers to address the "subsidy cliff." Without federal intervention to restore or replace the enhanced tax credits, analysts suggest that the current wave of exits may only be the beginning.

Implications: The Consumer Burden

The implications of these exits for the average American are multifaceted and largely negative.

1. Reduced Plan Options

The most immediate effect of insurer exits is a reduction in the number of plans available to consumers. A smaller list of carriers often translates to less competition, which historically leads to higher premiums and more restrictive networks (e.g., fewer doctors or specialists covered).

2. Risk Pool Instability

The fear among health policy analysts is the "death spiral" dynamic. If the healthiest individuals—those who use the least healthcare—drop coverage first, the average cost per enrollee rises. This forces insurers to raise premiums, which in turn causes the next group of moderately healthy enrollees to drop their coverage. The result is a market that becomes increasingly expensive and increasingly skewed toward the chronically ill, making it harder to sustain long-term.

3. The "Choice-Limited" Reality

While we have avoided the return of "bare counties" (areas where no insurance is available), the emergence of "choice-limited" markets is a subtle but significant decline in the quality of the ACA. When consumers are limited to one or two insurers, they lose the ability to "vote with their feet," effectively stripping the market of the consumer-driven pressure that keeps premiums in check.

4. Long-Term Uncertainty

The uncertainty surrounding the 2027 plan year creates a barrier to entry for new, smaller insurers. Why would a regional health plan invest the significant resources required to build a network if the regulatory and financial environment of the ACA is perceived to be in a state of permanent flux?

Conclusion: A Critical Juncture for the ACA

The ACA Marketplaces are entering a period of forced consolidation. The departure of six carriers, including major national players, suggests that the private sector’s appetite for the individual exchange market is waning in the absence of robust, sustained federal subsidies.

While the system is far from collapse, it is undeniably fragile. The stability of the ACA has historically relied on a delicate balance: enough competition to keep prices low, and enough government support to keep enrollment high. With the loss of the enhanced tax credits, that balance has been disrupted.

As we move toward the 2027 enrollment period, the focus will shift to how remaining insurers adjust their rates and how state regulators respond to the sudden gaps in coverage. For millions of Americans, the promise of the ACA—affordable, accessible coverage—is currently being tested by the realities of market economics. The coming months will determine whether the current wave of exits is a temporary correction or a long-term retreat from the individual insurance market.