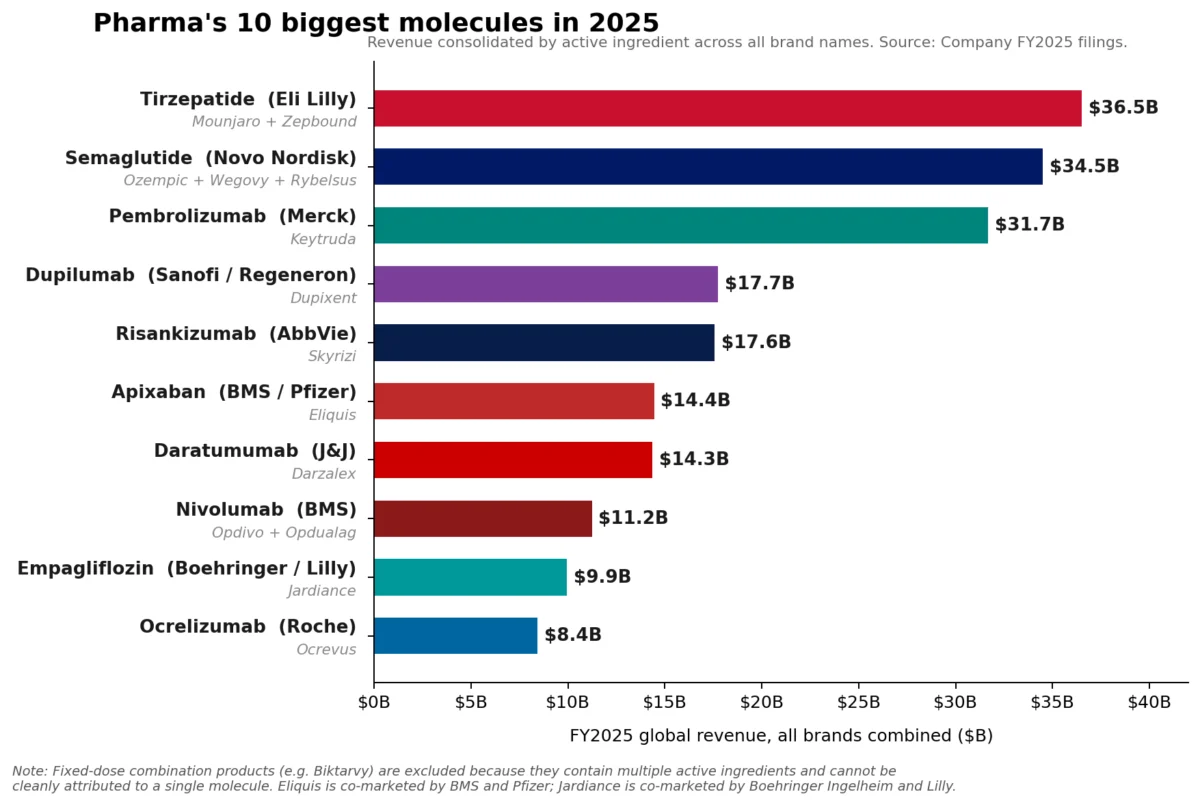

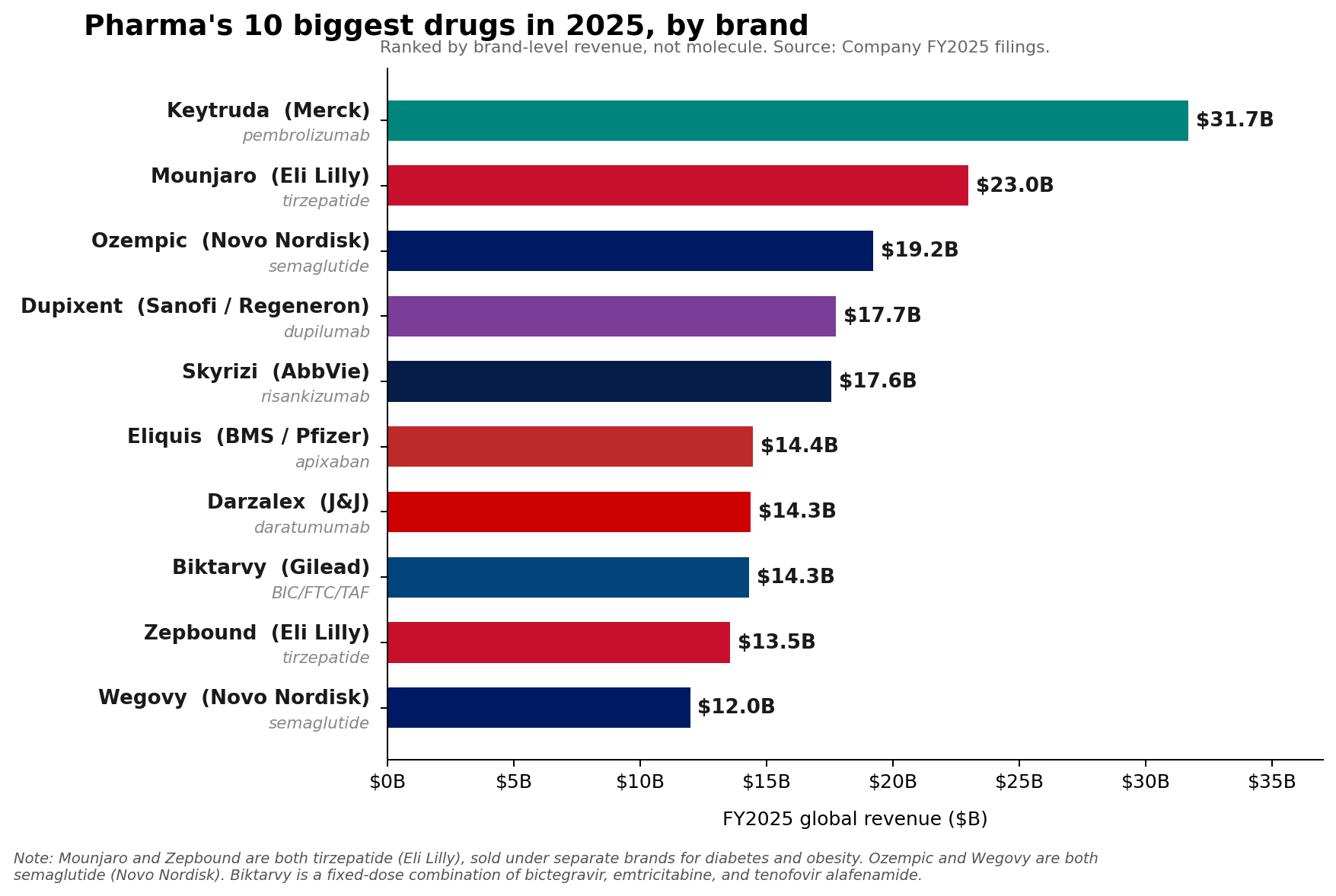

The landscape of the global pharmaceutical industry has undergone a seismic shift as of fiscal year 2025. For years, Merck’s powerhouse oncology drug, Keytruda (pembrolizumab), has reigned supreme as the undisputed king of the pharmacy shelf. While it successfully defended its title as the industry’s top-selling individual brand in 2025 with a staggering $31.7 billion in revenue, the throne is no longer secure when viewed through the lens of molecular dominance.

The rapid ascent of the GLP-1 receptor agonist class—specifically Eli Lilly’s tirzepatide and Novo Nordisk’s semaglutide franchises—has fundamentally altered the hierarchy of pharmaceutical wealth. As the industry navigates a post-pandemic reality defined by chronic disease management, the competitive dynamics between traditional oncology blockbusters and the new wave of metabolic treatments are setting the stage for a dramatic 2026.

Main Facts: The Changing of the Guard

In FY2025, Merck’s Keytruda demonstrated resilience with a 7% growth rate, continuing to provide a bedrock of revenue for the pharmaceutical giant. However, the molecule-level data tells a different story. When combining the revenue from Lilly’s Mounjaro ($22.965 billion) and Zepbound ($13.542 billion), the tirzepatide franchise reached a combined annual haul of approximately $36.5 billion.

Simultaneously, Novo Nordisk’s semaglutide portfolio—encompassing the household names Ozempic, Wegovy, and Rybelsus—surged to roughly $34.5 billion. By these metrics, the GLP-1 revolution has officially eclipsed the dominance of single-brand oncology staples in terms of total molecular revenue generation.

This is not merely a story of metabolic medicine; it is a story of diversification. Other heavyweights, such as AbbVie’s Skyrizi and Rinvoq, along with Sanofi’s Dupixent, continue to exhibit high-double-digit growth, proving that the pharmaceutical "Pharma 50" is not evolving into a monoculture of weight-loss drugs, but rather a more robust, multi-pillar ecosystem.

Chronology: A Trajectory of Transformation

The shift in market power did not occur overnight; it is the culmination of years of R&D investment and aggressive commercial scaling.

- 2018: Eli Lilly secures a critical license from Chugai for the small-molecule GLP-1 agonist, orforglipron, laying the groundwork for a future oral pill strategy.

- 2023–2024: Mounjaro and Ozempic experience explosive growth as clinical data confirms their efficacy beyond glycemic control, extending into cardiovascular and weight-management arenas.

- January 2026: Novo Nordisk launches the Wegovy pill, signaling a pivot toward oral delivery mechanisms for the semaglutide franchise.

- April 1, 2026: A landmark day for the industry as the FDA grants approval to Eli Lilly’s Foundayo (orforglipron), the first oral small-molecule GLP-1 for weight loss.

- April 9, 2026: Commercial availability of Foundayo begins in the United States, officially sparking a new battle for market share in the oral metabolic space.

Supporting Data: Beyond the Obesity Hype

While the headlines are dominated by GLP-1s, the underlying data from the Citeline 2026 Pharma R&D Annual Review suggests a more complex reality. While the total number of pipeline compounds has seen a slight contraction, the anti-obesity category has exploded by 30.7%, now boasting 588 active compounds.

However, the "immunology engine" remains a formidable force. AbbVie provides the clearest example of this stability. In 2025, Skyrizi ($17.562 billion) and Rinvoq ($8.304 billion) combined for $25.866 billion in revenue. This duo represents roughly 42% of AbbVie’s $61.160 billion total annual revenue. These drugs are not just "products"—they are essential, high-growth platforms that provide sustainable, long-term cash flow that rivals the absolute revenue growth of the metabolic giants.

Furthermore, Novartis has seen its oncology asset, Kisqali, climb 58% to reach $4.783 billion. These figures demonstrate that while the GLP-1s are capturing the public imagination and the highest volume of new pipeline investment, the commercial durability of established immunology and oncology franchises remains the bedrock of modern pharmaceutical finance.

Official Responses and Strategic Outlook

Merck CEO Rob Davis remains characteristically measured regarding the future of Keytruda. As the drug approaches its eventual loss of exclusivity (LoE) in the coming years, Davis has strategically framed the transition as "more of a hill than a cliff." Merck is actively extending the Keytruda lifecycle through new indications and the development of subcutaneous delivery methods like QLEX. Despite these efforts, Merck’s FY2026 revenue guidance of $65.5 billion to $67.0 billion fell slightly below Wall Street’s optimistic expectations, reflecting investor anxiety regarding the inevitable post-Keytruda era.

Conversely, Eli Lilly is leaning into its aggressive growth phase. Having guided to $80 billion to $83 billion in revenue for 2026, the company is betting heavily on the Foundayo launch. Yet, management has tempered expectations regarding the immediate impact of the new pill, noting that the Q1 2026 results were largely driven by the established Mounjaro and Zepbound franchises. The real test for orforglipron will be its performance over the remainder of the 2026 fiscal year.

Novo Nordisk is navigating a more cautious path. Despite the launch of the Wegovy pill, the company has provided 2026 guidance of negative 5% to negative 13% adjusted sales growth at constant exchange rates. This conservative outlook highlights the harsh realities of the current market: pricing pressure, heightened competition from Lilly, and the complexities of U.S. healthcare access dynamics.

Implications: The New Era of Pharma Competition

The transition from a "Keytruda-centric" market to a multi-polar environment has three major implications for the industry:

1. The Rise of Oral Metabolic Therapy

The approval of Foundayo represents a strategic inflection point. If oral GLP-1s can successfully transition patients from injectables to pills, the addressable market for obesity treatment could expand significantly. However, this shift risks commoditizing the space, forcing manufacturers to compete on price and accessibility rather than just clinical efficacy.

2. The Resilience of Immunology

The data suggests that the industry is not becoming a "GLP-1 monoculture." The 20.6% growth in the immunology sector, despite a broader pipeline contraction, confirms that investors and payers alike remain committed to chronic, high-cost therapy areas where clinical differentiation is easier to prove. AbbVie’s success with Skyrizi and Rinvoq serves as a roadmap for other firms looking to build "compounding franchises" that offer a hedge against the volatility of the metabolic market.

3. The "Hill vs. Cliff" Reality

Merck’s experience with Keytruda will serve as the industry’s bellwether for the next decade. If a company with the scale and clinical reach of Merck can successfully navigate a major LoE, it will validate the strategy of "lifecycle management"—using subcutaneous formulations and new indications to maintain a product’s relevance long after its initial patent protection begins to erode.

Conclusion

As we look further into 2026, the pharmaceutical industry finds itself in a state of productive tension. The meteoric rise of tirzepatide and semaglutide has successfully dethroned the oncology-heavy status quo, creating a more diverse and highly competitive environment. While the "weight-loss gold rush" continues to dominate the headlines, the sustained performance of immunology giants reminds us that the industry’s true strength lies in its ability to simultaneously address multiple global health crises.

For investors, policymakers, and patients, the message is clear: the pharmaceutical leaderboard is no longer a static list of brands, but a dynamic, fast-moving landscape defined by the constant struggle between new, blockbuster-potential metabolic therapies and the enduring, compounding power of specialized immunology and oncology medicines. The "Pharma 50" has officially entered its most competitive era yet.