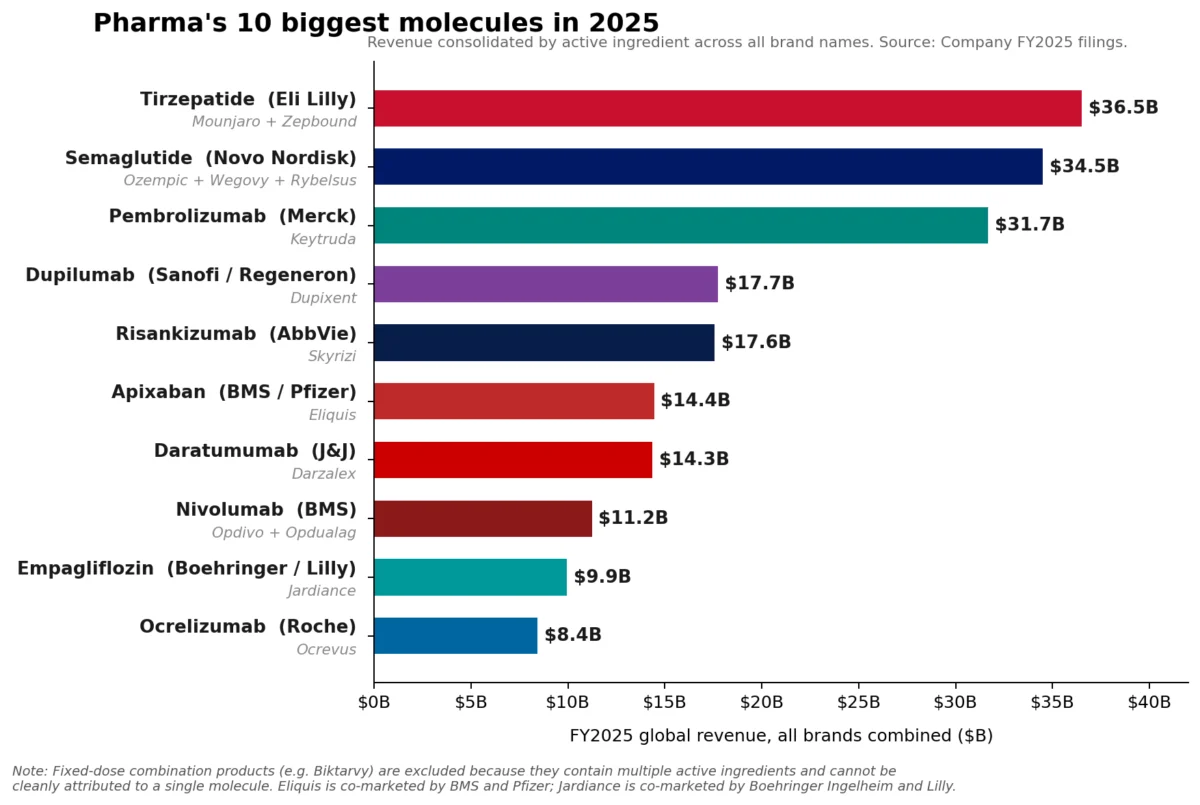

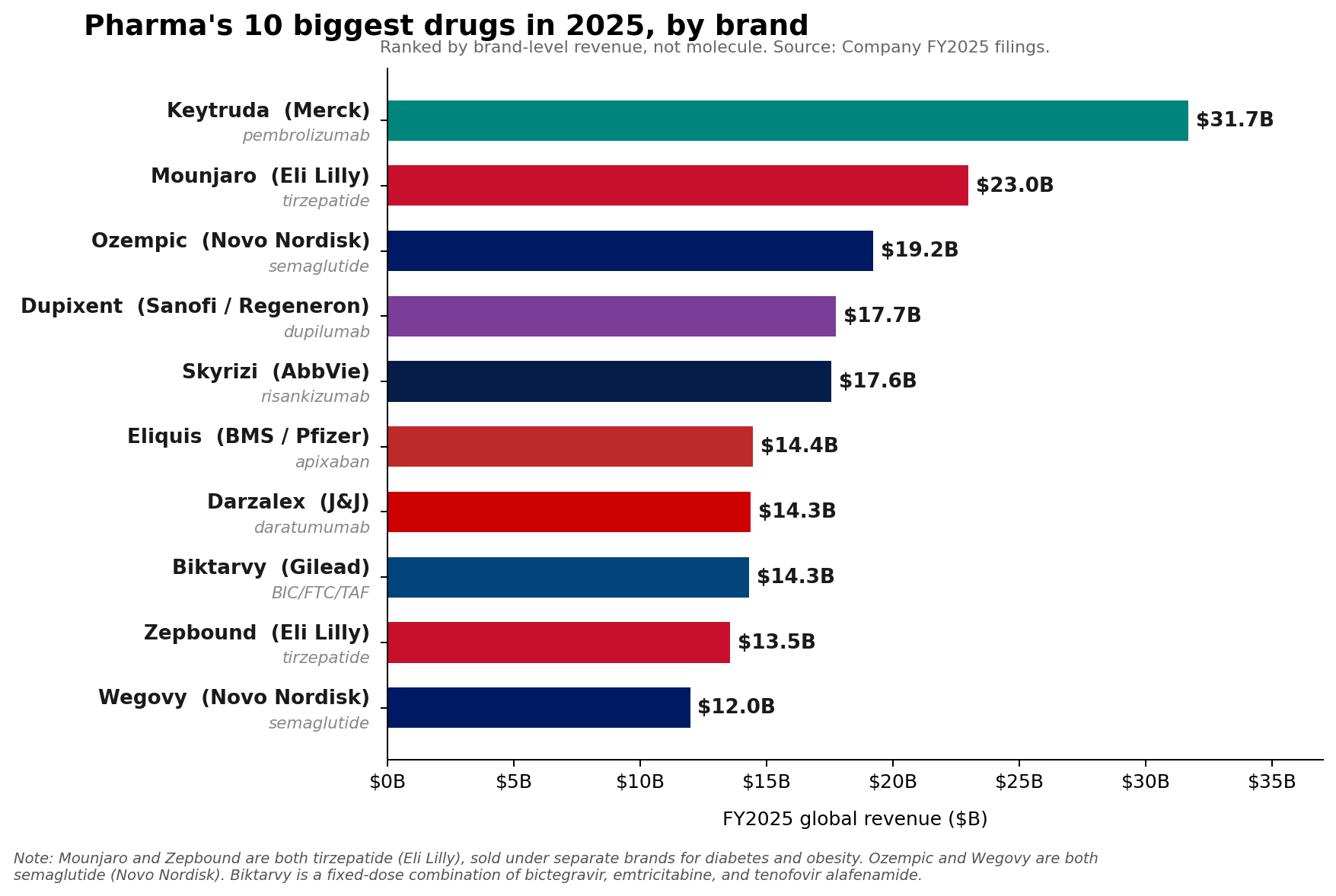

The global pharmaceutical landscape has undergone a seismic shift. For years, Merck’s oncology powerhouse, Keytruda (pembrolizumab), stood as the undisputed monarch of the industry. However, fiscal year 2025 marked a definitive turning point: while Keytruda remains the top individual brand globally with $31.7 billion in revenue, it has been eclipsed at the molecule level by the twin juggernauts of the metabolic era: Eli Lilly’s tirzepatide and Novo Nordisk’s semaglutide.

As the industry pivots toward a future dominated by GLP-1 receptor agonists and high-growth immunology franchises, the traditional hierarchy of blockbuster drugs is being rewritten. This transition is not merely a change in rankings; it represents a fundamental rebalancing of R&D investment and market power, setting the stage for a volatile and highly competitive 2026.

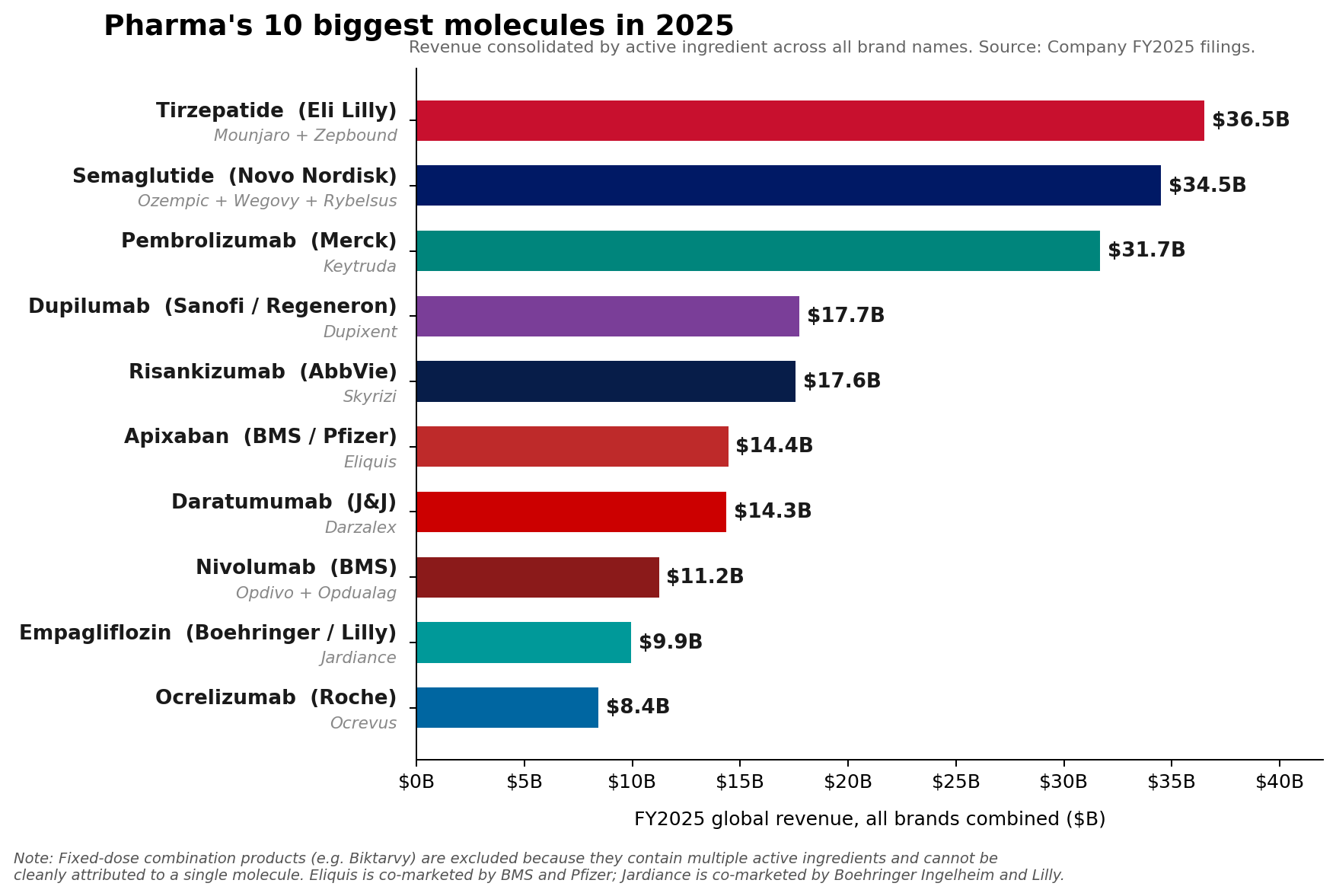

Main Facts: The New Revenue Order

In FY2025, Merck’s Keytruda demonstrated impressive resilience, recording a 7% year-over-year growth to reach $31.7 billion. Yet, this figure is no longer the ceiling for a single therapeutic agent. Eli Lilly’s tirzepatide franchise—encompassing both Mounjaro for diabetes and Zepbound for weight management—surged to a combined $36.5 billion in 2025. Simultaneously, Novo Nordisk’s semaglutide portfolio, anchored by Ozempic, Wegovy, and the oral Rybelsus, hit approximately $34.5 billion.

This transition highlights a "GLP-1 pivot." While oncology has long been the primary driver of pharmaceutical valuation, the metabolic space has reached an unprecedented scale, transforming from a niche therapeutic category into a massive, multi-billion-dollar engine of growth that is reshaping the balance sheets of the world’s largest pharma companies.

Chronology: The Road to the 2026 Shift

The evolution of the pharma hierarchy did not happen overnight, but the pace of change accelerated sharply in 2025 and early 2026.

- 2018–2022: The foundation for the current shift was laid as Lilly and Novo Nordisk ramped up clinical trials for their respective GLP-1 assets.

- FY2025: The year of transition. Mounjaro and Zepbound reached a combined $36.5 billion, while semaglutide products reached $34.5 billion, officially pushing Keytruda into the second-tier position at the molecule level.

- January 2026: Novo Nordisk launched the oral Wegovy pill, signaling a move to capture the oral GLP-1 market.

- April 1, 2026: A critical inflection point occurred when the FDA granted approval to Eli Lilly’s Foundayo (orforglipron), the company’s once-daily oral small-molecule GLP-1.

- April 6–9, 2026: Commercial shipping of Foundayo began, marking its entry into a highly contested and rapidly expanding obesity market.

Supporting Data: Beyond the GLP-1 Monoculture

Despite the meteoric rise of obesity drugs, the broader pharmaceutical sector remains surprisingly diverse. According to the Citeline 2026 Pharma R&D Annual Review, while the overall pipeline count has dipped, immunological therapeutics are experiencing a renaissance, growing by 20.6% in 2026.

This is best exemplified by AbbVie, which has successfully transitioned its portfolio away from its legacy Humira-dependence. In 2025, Skyrizi generated $17.562 billion, while Rinvoq contributed $8.304 billion. Together, these two assets account for roughly 42% of AbbVie’s $61.16 billion total revenue. Similarly, Sanofi’s Dupixent continued its ascent to €15.714 billion, and Novartis’s Kisqali saw a 58% surge, hitting $4.783 billion.

The data suggests that the industry is not coalescing into a "GLP-1 monoculture." Instead, we are witnessing the rise of "super-blockbuster" franchises in oncology and immunology that are compounding at rates that rival, and in some cases exceed, the growth trajectories of older, established brands.

Official Responses and Strategic Guidance

Merck, facing the inevitable loss of exclusivity for Keytruda in the coming years, has maintained a cautious but confident stance. CEO Rob Davis has famously characterized the patent cliff as "more of a hill than a cliff," emphasizing that Merck’s strategy involves extending the Keytruda franchise through new indications and lifecycle management moves, such as the development of a subcutaneous version (QLEX).

However, Wall Street remains skeptical of the near-term outlook. Merck’s FY2026 revenue guidance—projected between $65.5 billion and $67.0 billion—fell short of analyst expectations, reflecting the uncertainty surrounding the transition period for its lead asset.

Conversely, Eli Lilly has provided an aggressive outlook, guiding toward $80 billion to $83 billion in 2026 revenue. The strategic deployment of Foundayo is central to this, though leadership acknowledges that Mounjaro and Zepbound will remain the primary drivers of cash flow throughout the year, given their established market penetration.

Novo Nordisk, meanwhile, faces a more complex path. While it is pushing hard into the oral GLP-1 space, its 2026 guidance remains conservative, forecasting adjusted sales growth of -5% to -13% at constant exchange rates (CER). This reflects a realistic assessment of pricing pressure and the competitive dynamics currently playing out in the U.S. market.

Implications: A Market in Flux

The implications of this shift are profound for both investors and patients.

1. The "Hill, Not a Cliff" Reality

Merck’s ability to navigate the post-Keytruda era will set the benchmark for how "Big Pharma" handles the sunsetting of its most successful products. By pivoting toward subcutaneous delivery and novel oncology combinations, the company is attempting to maintain its premium status. If they succeed, it will provide a roadmap for others facing similar patent expirations.

2. The Obesity Arms Race

The approval of orforglipron (Foundayo) introduces a new variable into the obesity market. While analysts are divided on its immediate revenue impact, it confirms that the market is rapidly moving toward oral, small-molecule options. This will likely exert downward pressure on the pricing of existing injectable GLP-1s and increase the intensity of the commercial "land grab" in 2026.

3. The Resilience of Immunology

The robust performance of Skyrizi, Rinvoq, and Dupixent proves that the market for autoimmune and inflammatory disease treatments remains a bedrock of the industry. Investors who have over-indexed on GLP-1s might be overlooking the "durable growth" potential inherent in these immunology franchises, which appear less susceptible to the pricing volatility currently hitting the metabolic sector.

4. R&D Contraction vs. Therapeutic Expansion

The Citeline data indicating a 30.7% jump in anti-obesity pipeline compounds to 588, set against a backdrop of overall industry pipeline contraction, reveals a clear trend: companies are prioritizing high-conviction, high-reward metabolic targets. This "flight to quality" means that smaller, less-proven programs are being jettisoned, as pharma giants concentrate their capital on areas where market demand is already proven.

Conclusion: Looking Ahead to 2027

As we move deeper into 2026, the industry is defined by two competing narratives. The first is the meteoric, headline-grabbing growth of the GLP-1 franchise, which has successfully unseated the long-reigning king of pharma. The second is the quiet, steady compounding of immunology and oncology franchises that are building the "durable growth" needed to sustain companies once the initial obesity gold rush levels off.

For the pharmaceutical industry, 2026 is a year of consolidation and strategic recalibration. Companies that can effectively bridge the gap between their legacy blockbusters and their next-generation metabolic portfolios will dictate the future of the top 50. The leaderboard is no longer a static list of the largest brands; it is a dynamic, shifting landscape that rewards agility, pipeline focus, and the ability to manage the transition from the blockbuster era to the era of hyper-competitive, specialized medicine.

Whether or not the GLP-1 market maintains its current trajectory will depend on pricing, access, and the long-term clinical data emerging from these new oral therapies. For now, however, the industry has clearly entered a new epoch—one where the molecule is the new brand, and metabolic health is the new battleground for global dominance.