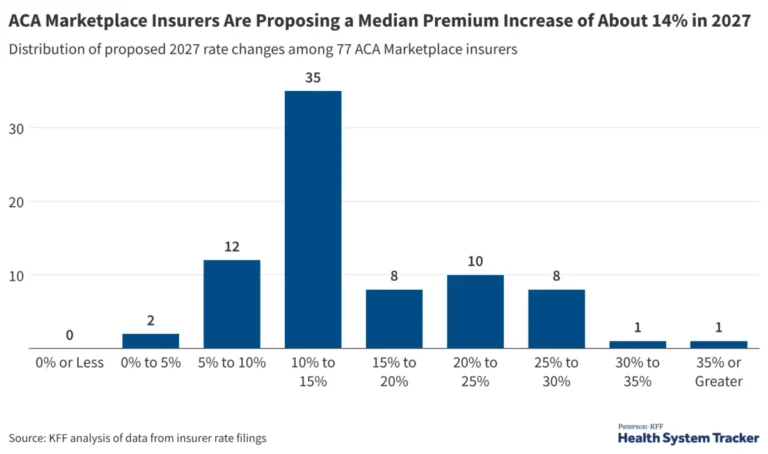

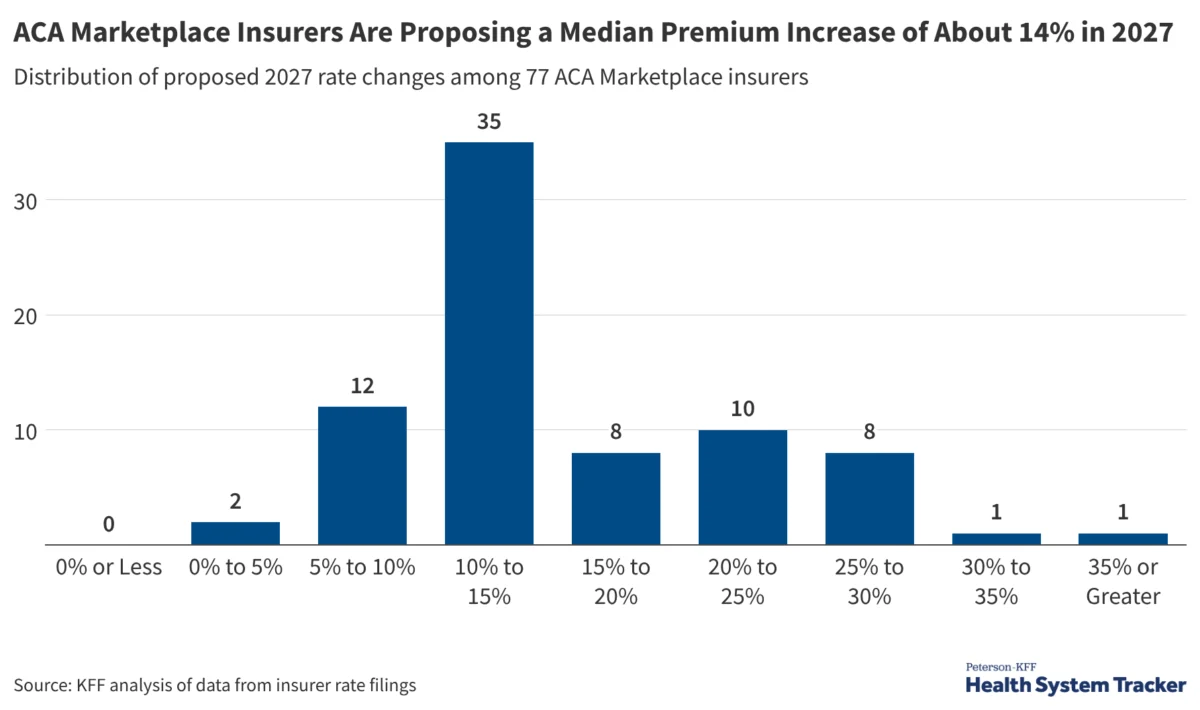

As the U.S. healthcare landscape prepares for the 2027 plan year, millions of Americans enrolled in Affordable Care Act (ACA) Marketplace plans are bracing for a potential financial shock. A new analysis of preliminary rate filings from 16 states and the District of Columbia reveals that insurers are proposing a median premium increase of 14%. If these requested rates are finalized, it would mark the second consecutive year of double-digit premium growth, signaling a significant trend toward rising healthcare affordability challenges.

The Main Facts: A Trajectory of Increasing Costs

The data, provided by the Peterson-KFF Health System Tracker, paints a concerning picture for consumer budgets. For the 77 insurers analyzed across the reporting jurisdictions, the trend is overwhelmingly upward. Most insurers are seeking rate adjustments between 10% and 20%, while a notable cohort—20 individual insurers—are requesting increases exceeding 20%.

If these proposed rates are implemented without modification, the cumulative effect will be profound. Analysts estimate that between 2025 and 2027, typical premiums for participating ACA Marketplace insurers could jump by more than one-third. This rapid escalation threatens to erode the stability that has characterized the Marketplace in recent years, potentially forcing consumers to choose between reduced coverage options or shouldering a much heavier portion of their household expenses.

Chronology: How We Arrived at the 2027 Outlook

To understand the current volatility, one must look at the timeline of factors shaping the insurance market:

- 2021–2023 (The Era of Subsidies): The American Rescue Plan Act (ARPA) and subsequent extensions provided enhanced premium tax credits, which significantly lowered out-of-pocket costs for millions, driving record-high enrollment in the ACA Marketplace.

- 2024–2025 (The Return of Normalcy and Cost Pressures): Following the post-pandemic stabilization, insurers began to see a return to "normal" utilization rates, coupled with the rising cost of medical services and pharmaceutical spending.

- 2026 (The First Wave of Double-Digit Hikes): Insurers began adjusting for medical inflation and the narrowing window of federal subsidy support, resulting in the first major round of double-digit premium increases.

- July 15, 2026 (The Filing Deadline): This critical date served as the benchmark for the current round of preliminary filings. As insurers submitted their 2027 proposals, the industry signals became clear: the upward trajectory is accelerating.

- Late 2026 (Review and Approval): State regulators and federal oversight bodies are currently evaluating these filings. This phase is critical, as regulators often negotiate with insurers to trim excessive requests before the final rates are locked in for the upcoming open enrollment period.

Supporting Data: Dissecting the Drivers of Inflation

The Peterson-KFF analysis highlights that these premium hikes are not arbitrary; they are reactions to a convergence of systemic pressures. Insurers cite three primary drivers:

1. The Rising Cost of Health Services

Medical inflation is currently outstripping general inflation. Hospitals and medical providers, facing their own labor shortages and rising supply chain costs, are renegotiating contracts with insurance carriers. When a hospital charges more for procedures, imaging, and routine care, those costs are passed directly to the insurer, which in turn must raise premiums to maintain solvency.

2. The Expiration of Enhanced Premium Tax Credits

Perhaps the most significant policy-driven factor is the looming expiration of the enhanced premium tax credits. While the ACA provides a baseline of support, the "enhanced" levels that have made plans affordable for middle-income earners are set to expire. Without legislative intervention, the federal government will effectively shift a larger portion of the premium burden back onto the consumer.

3. Federal Regulatory Changes

Insurers are also adjusting their models to account for evolving federal regulations. Changes to the "risk adjustment" formulas, updates to the Essential Health Benefits (EHB) requirements, and adjustments in how insurers are compensated for covering high-risk populations have all contributed to a more conservative pricing strategy. When uncertainty regarding federal support increases, insurers historically respond by increasing premiums to hedge against potential losses.

Official Responses and Industry Perspectives

The insurance industry, through trade groups and individual filings, has maintained a consistent narrative: they are caught in a "cost-push" environment. Representatives from major carriers argue that the premiums reflect the true, underlying cost of providing high-quality care in an inflationary environment.

"We are committed to providing access to care, but we cannot ignore the fundamental reality of medical trends," stated a spokesperson for a regional health plan involved in the filings. "If the cost of a knee replacement or a specialty drug rises by 8%, and we are paying for millions of such services, our premium structure must adjust to ensure we can pay those claims."

Consumer advocates, conversely, are calling for more stringent regulatory oversight. They argue that while inflation is a factor, insurers should be held accountable for high administrative costs and executive compensation. They urge state insurance commissioners to scrutinize these 14% median requests closely, suggesting that some insurers may be overestimating future costs to pad their margins.

Implications: What This Means for the Consumer

The implications of these potential increases are far-reaching.

The Burden on Middle-Income Families

The primary risk is a phenomenon known as "premium shock." Families who have relied on the enhanced subsidies to keep their coverage within a manageable budget may find that, come 2027, their monthly premiums are no longer sustainable. This could lead to a decrease in the number of insured individuals, as some may choose to "go bare" (uninsured) rather than pay the increased rates.

The Shift in Plan Selection

We are likely to see a "downward shift" in plan selection. Consumers who currently opt for "Gold" or "Silver" plans may be forced to downgrade to "Bronze" plans to keep their monthly costs stable. While this keeps them in the system, these plans often come with significantly higher deductibles and out-of-pocket maximums, which may discourage these individuals from seeking care when they actually need it—the very problem the ACA was designed to solve.

The Political Spotlight

As the 2027 plan year approaches, the ACA Marketplace will inevitably become a focal point in national political discourse. The expiration of subsidies and the subsequent premium hikes will force Congress to decide whether to provide further relief or allow the market to recalibrate to pre-subsidy levels. The upcoming legislative sessions will be pivotal, as the outcome will determine whether the U.S. health system continues on a path of broad, subsidized access or shifts toward a more fragmented model of coverage.

Conclusion: A Critical Juncture for the ACA

The preliminary filings for 2027 serve as a warning light on the dashboard of the U.S. healthcare system. A median increase of 14% is not merely a statistical anomaly; it is a symptom of deep-seated issues regarding medical inflation, the uncertainty of federal support, and the fragile balance between insurer solvency and consumer affordability.

As the review process continues, the focus must remain on transparency. Policyholders, policymakers, and industry analysts must work in tandem to ensure that these premium increases are justified by actual clinical costs rather than administrative bloat or market volatility. For millions of Americans, the stakes are high: the ability to access and afford healthcare in 2027 hinges on the decisions made in the coming months. The Peterson-KFF Health System Tracker will continue to monitor these developments, providing the data necessary to navigate this challenging landscape.

For those currently enrolled in the Marketplace, the advice from experts is clear: prepare for the upcoming Open Enrollment period by comparing plans thoroughly, understanding the impact of potential subsidy changes, and engaging with state-run consumer assistance programs. The path to 2027 is paved with uncertainty, but informed decision-making remains the consumer’s strongest tool.