As U.S. households continue to rank health care affordability as a top-tier national concern, a critical driver of the crisis has moved into the spotlight: the escalating cost of hospital care. Representing roughly one-third of all national health care expenditures, hospitals are the single largest component of the U.S. medical economy. Between 2022 and 2024 alone, hospital spending was responsible for 40% of the total growth in national health spending, signaling a systemic trend that is squeezing employer budgets, suppressing wage growth, and ballooning out-of-pocket costs for millions of Americans.

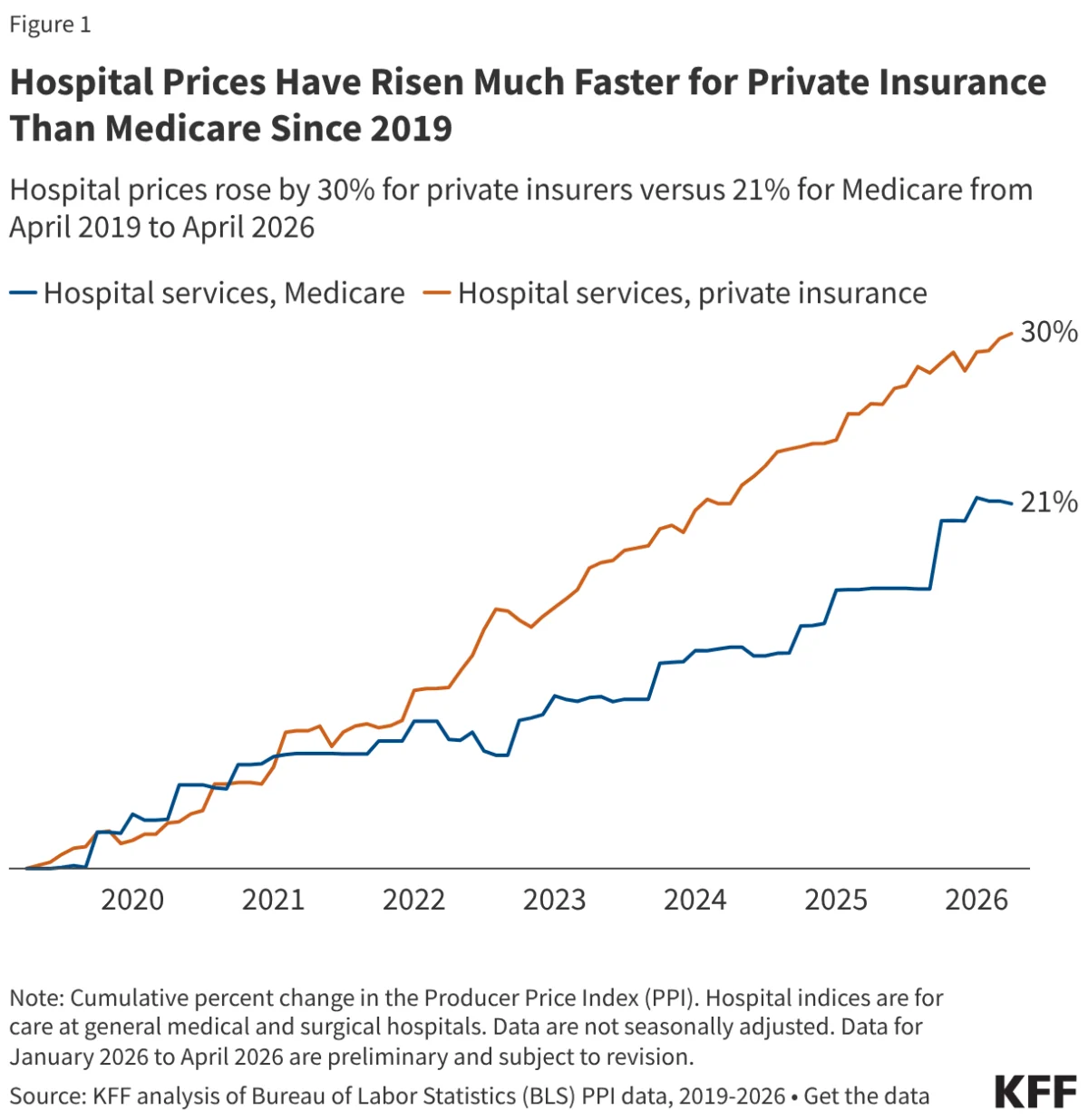

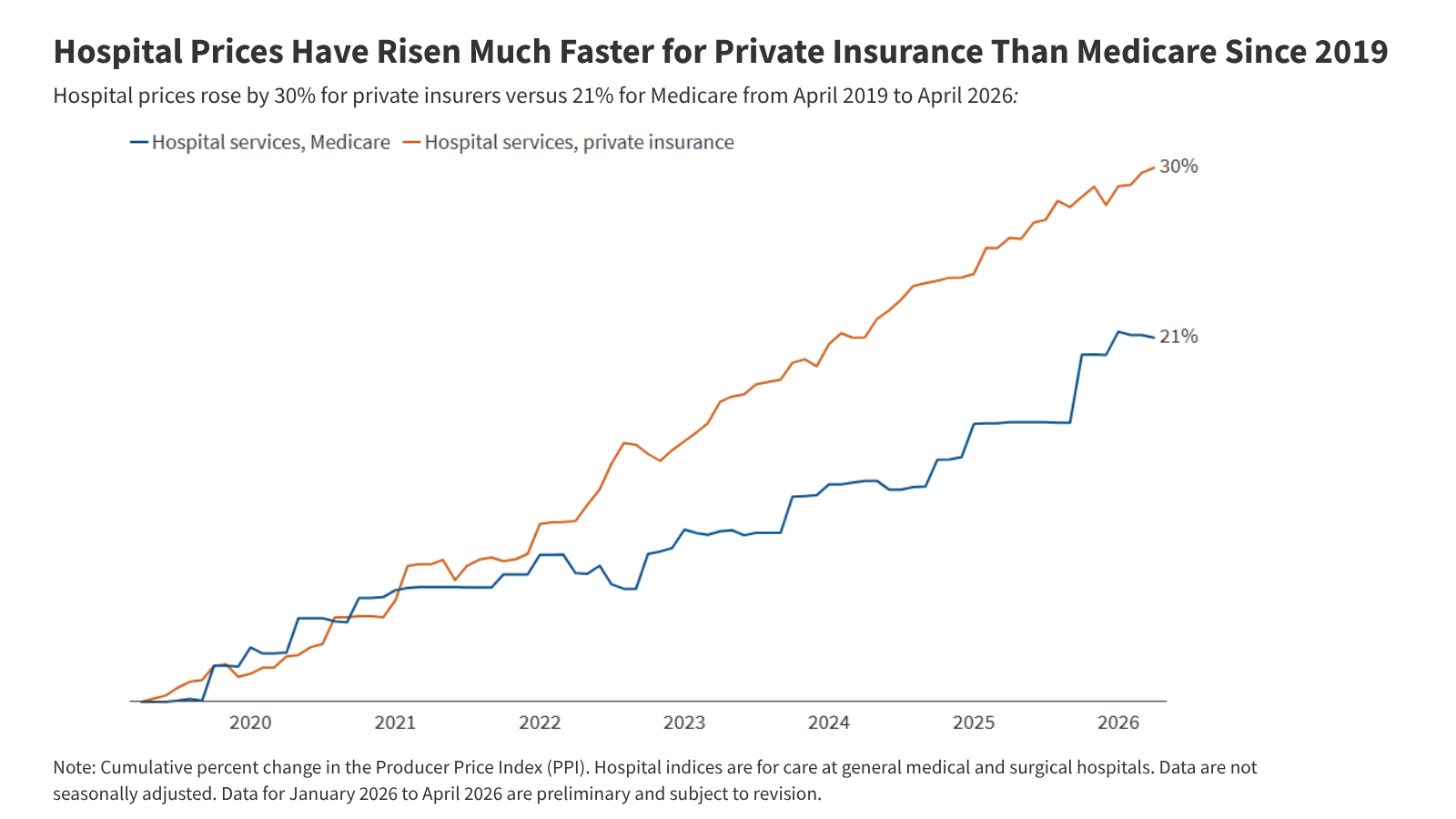

New data from the Bureau of Labor Statistics (BLS) Producer Price Index (PPI) paints a stark picture: from April 2019 to April 2026, private insurance payments for hospital services rose by 30%, significantly outpacing the 21% growth observed in Medicare rates. This disparity underscores a growing divide in the healthcare marketplace, where private insurers—and by extension, the patients and employers they cover—are facing a steeper financial trajectory than the federal government’s primary health program.

The Chronology of Divergence: A Seven-Year Trend

To understand the current inflationary environment, it is necessary to examine the trajectory of hospital pricing since the onset of the COVID-19 pandemic. The analysis period, beginning in April 2019, provides a baseline that captures both the pre-pandemic stability and the subsequent economic shocks.

The Pandemic Baseline (2019–2020)

In the initial year of the study, the growth rates for private insurance and Medicare were remarkably aligned. Both sectors faced similar pressures as the healthcare system grappled with the early stages of a global health crisis. During this period, the mechanisms for price negotiation and federal rate-setting operated in relative synchronization.

The Inflationary Surge (2020–2025)

Starting in 2020, the paths began to diverge sharply. Each year, from 2020 through 2025, private insurance prices consistently grew at a faster rate than Medicare rates. This period saw a massive spike in economy-wide inflation, which peaked in mid-2022. While hospitals negotiated aggressively for higher reimbursement rates from private insurers to cover rising labor and supply costs, Medicare rates—which are set through statutory formulas—responded more sluggishly.

The Recent Plateau (2025–2026)

Interestingly, the period between April 2025 and April 2026 saw private insurance price growth slow to a rate lower than that of Medicare. While this brief reprieve offers a moment of stabilization, it does not erase the cumulative 47% faster growth rate that private insurance experienced compared to Medicare over the entire seven-year duration.

Supporting Data: Understanding the Market Mechanics

The core of this issue lies in how prices are determined for different payers. The discrepancy between the 30% growth in private insurance pricing and the 21% in Medicare is not merely a result of market forces; it is a reflection of fundamentally different regulatory and bargaining environments.

The Role of Market Consolidation

A significant factor driving the private insurance price index upward is the increasing concentration of hospital market power. According to recent KFF analysis, 83% of metropolitan areas in the United States now feature a landscape where one or two health systems control at least 75% of the market for inpatient care. In these monopolistic or oligopolistic environments, hospitals possess significant leverage during contract negotiations with private insurers. Because private insurance networks are often required to include major local hospital systems to remain viable for employers, insurers have limited ability to push back against price hikes.

Medicare’s Regulatory Constraints

Conversely, traditional Medicare prices are updated annually by the Centers for Medicare and Medicaid Services (CMS) through the Inpatient and Outpatient Prospective Payment Systems (IPPS and OPPS). These updates are tied to statutory formulas that incorporate estimates of hospital input costs.

Crucially, Medicare’s growth is intentionally tempered by productivity adjustments mandated by the Affordable Care Act (ACA). These adjustments assume that hospitals will achieve greater efficiencies over time, effectively baking a "cost-saving" mechanism into the federal reimbursement schedule. Furthermore, automatic sequestration—a budget-neutralizing mechanism—has periodically curtailed Medicare payments, acting as a structural brake that does not exist in the private, contract-based world of commercial insurance.

Official Responses and Policy Perspectives

The persistent gap between private and public rates has prompted a variety of responses from policymakers and industry stakeholders.

The Case for Price Regulation

Recognizing that market competition alone has failed to curb rising costs, several states have begun to experiment with direct price regulation. Indiana, for instance, recently enacted legislation that will eventually cap private insurance prices for nonprofit hospitals within the state. Similarly, Oregon has utilized a policy since 2019 that limits hospital prices to 200% of traditional Medicare rates for its state employee insurance plans. Proponents argue these measures are necessary to shield the public from the outsized influence of consolidated hospital systems.

The Industry’s Defense

The hospital industry frequently argues that the focus on price growth ignores the underlying "cost-plus" reality of providing care. Industry leaders point to the significant underestimation of inflation by CMS in recent years. When Medicare rates were set for 2022, the inflation forecasts used by regulators were significantly lower than the actual economic inflation experienced by hospitals. While some industry groups have lobbied for retrospective adjustments to account for these forecasting errors, CMS has largely maintained that its projections are accurate over long-term cycles, even if they miss the mark in any single, volatile year.

Economic Implications: The Burden on Households

The implications of this price gap are profound and ripple through the entire U.S. economy. When hospitals secure higher payment rates from private insurers, those costs are rarely absorbed by the insurers themselves. Instead, they are passed down to households through three primary channels:

- Higher Premiums: Employers, faced with rising medical costs, often shift the burden to employees in the form of higher monthly premiums.

- Increased Cost-Sharing: To manage rising expenses, insurers and employers have moved toward plans with higher deductibles, copayments, and coinsurance, making the point-of-service cost of care a significant barrier for many families.

- Wage Stagnation: Economic research has consistently shown that in the U.S., total compensation is a zero-sum game. When the portion of an employee’s compensation package allocated to health benefits grows disproportionately, the portion available for take-home pay shrinks. In essence, the rising cost of hospital services acts as a "hidden tax" on the American workforce.

Future Outlook and Methodological Context

The data provided by the PPI offers a unique lens for observing this phenomenon. Unlike the Consumer Price Index (CPI), which tracks prices from the perspective of the consumer and excludes certain government payers, the PPI tracks the producer’s perspective. By separating payers into Medicare and private insurance, the PPI reveals that the "healthcare inflation" experienced by the average American is fundamentally different from the fiscal realities managed by the federal government.

As lawmakers look toward the 2026 midterms and beyond, the debate over hospital pricing is unlikely to subside. Whether through antitrust enforcement aimed at breaking up consolidated hospital networks, or through state-level rate setting and price caps, the focus is shifting from "how to pay for healthcare" to "why the underlying cost of care is rising faster than the rest of the economy."

Without structural changes to how private contracts are negotiated or more aggressive oversight of provider market consolidation, the divergence between private and Medicare rates is poised to continue. For the American household, this means that even if general inflation stabilizes, the specific inflation associated with the hospital bedside may continue to be a persistent and unpredictable drag on personal financial health. The path forward will likely require a delicate balance between ensuring hospitals remain financially solvent to provide high-quality care and protecting the broader economy from the inflationary pressures of a hyper-consolidated provider market.