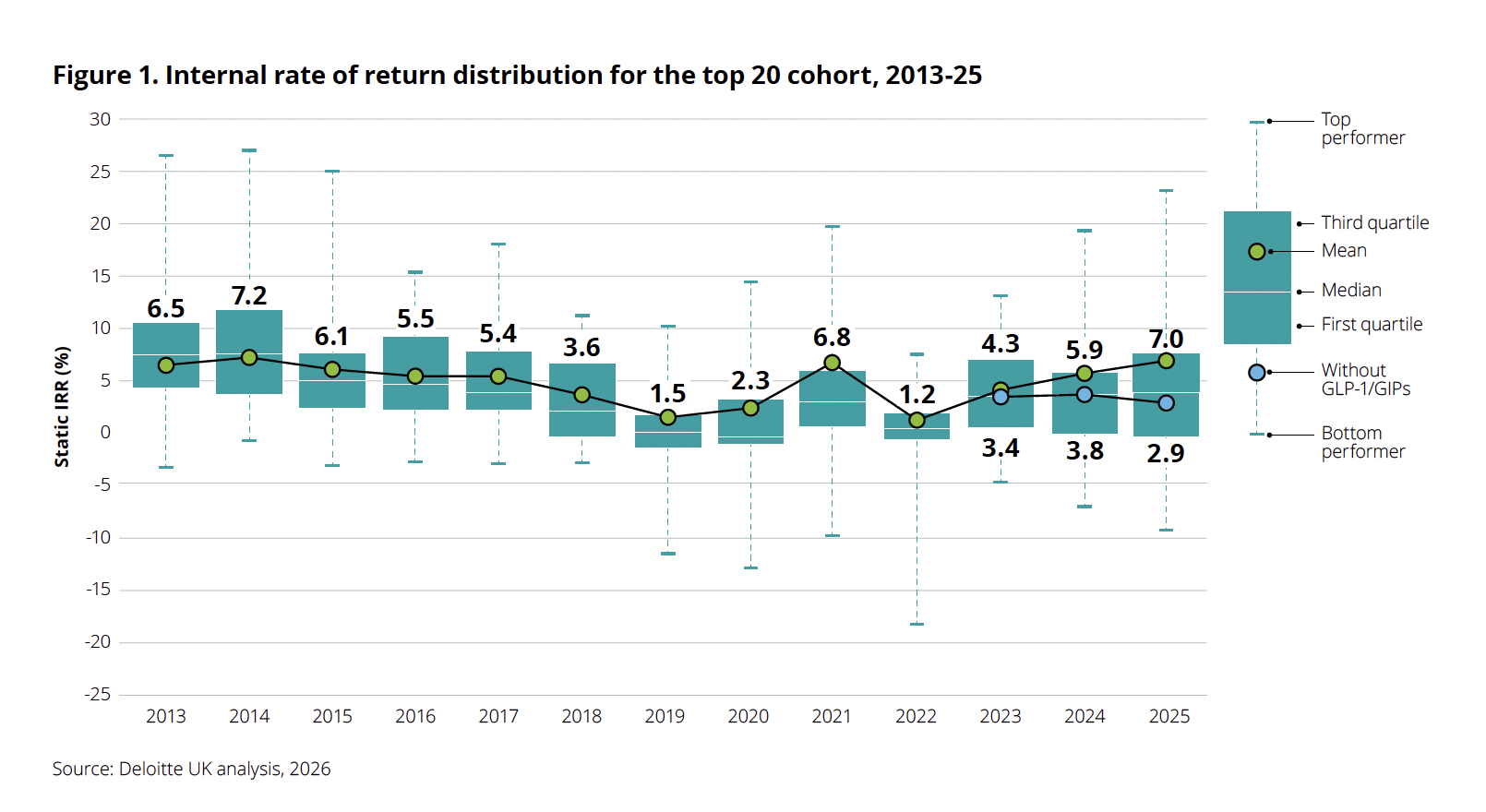

After years of pandemic-induced volatility and a prolonged era of declining research and development (R&D) productivity, the global pharmaceutical sector appears to be entering a season of renewal. According to the 16th edition of Deloitte’s annual Measuring the Return from Pharmaceutical Innovation report, the projected internal rate of return (IRR) for late-stage pipeline assets has climbed for the third consecutive year, reaching 7.0% in 2025. This marks a notable recovery from the 5.9% recorded the previous year.

However, beneath this veneer of industry-wide recovery lies a more complex, and perhaps more precarious, reality. The report, titled Navigating the GLP-1 Boom, suggests that the "springtime" currently enjoyed by Big Pharma is disproportionately fueled by a single, hyper-lucrative class of therapies: glucagon-like peptide-1 (GLP-1) and glucose-dependent insulinotropic polypeptide (GIP) receptor agonists.

The Core Finding: A Productivity Paradox

The primary takeaway from the 2026 data is that while headline returns are trending upward, the underlying health of the broader pharmaceutical pipeline remains stagnant or even in decline. When Deloitte analysts isolate the data and remove the GLP-1/GIP category—which now accounts for an unprecedented 38% of all projected commercial inflows—the industry’s IRR collapses from 7.0% to a mere 2.9%.

For context, in 2024, the IRR without these weight-loss blockbusters was 3.8%. This suggests that when the current "obesity gold rush" is stripped away, the core engine of drug discovery is actually producing less value than it was a year ago.

"There are two different messages here," explains Kevin Dondarski, principal for life sciences strategy at Deloitte Consulting. "The market is clearly valuing the transformative potential these therapies have on public health, which is a success story. But at the same time, it raises a significant question of sustainability. If a single class of drugs accounts for the vast majority of your value, what happens when the pipeline needs to replenish? That creates a massive responsibility for companies to identify the next generation of blockbuster assets."

Chronology of the GLP-1 Surge and Subsequent Market Turbulence

To understand the current state of the industry, one must track the trajectory of the obesity drug phenomenon over the past 18 months.

- Early 2025: The momentum behind GLP-1s reaches a fever pitch. Investors flock to Eli Lilly and Novo Nordisk, driving valuations to historic highs.

- November 2025: Faced with immense pressure, Novo Nordisk initiates a radical restructuring, including the departure of seven board members and the planned layoff of 9,000 employees to streamline operations and save $1.3 billion annually.

- February 2026: The competitive landscape shifts when Novo Nordisk’s highly anticipated CagriSema combination therapy fails to demonstrate non-inferiority against Eli Lilly’s Zepbound in the REDEFINE 4 trial, delivering 23% weight loss compared to Lilly’s 25.5%.

- January–April 2026: Novo Nordisk officially launches its oral Wegovy pill, generating DKK 2.26 billion in its first quarter, while Eli Lilly launches its own oral GLP-1, Foundayo (orforglipron).

- May 2026: Despite record revenue, investor sentiment begins to sour. Eli Lilly’s stock experiences a 10–13% year-to-date decline, signaling that even the strongest players are not immune to questions regarding price realization and market saturation.

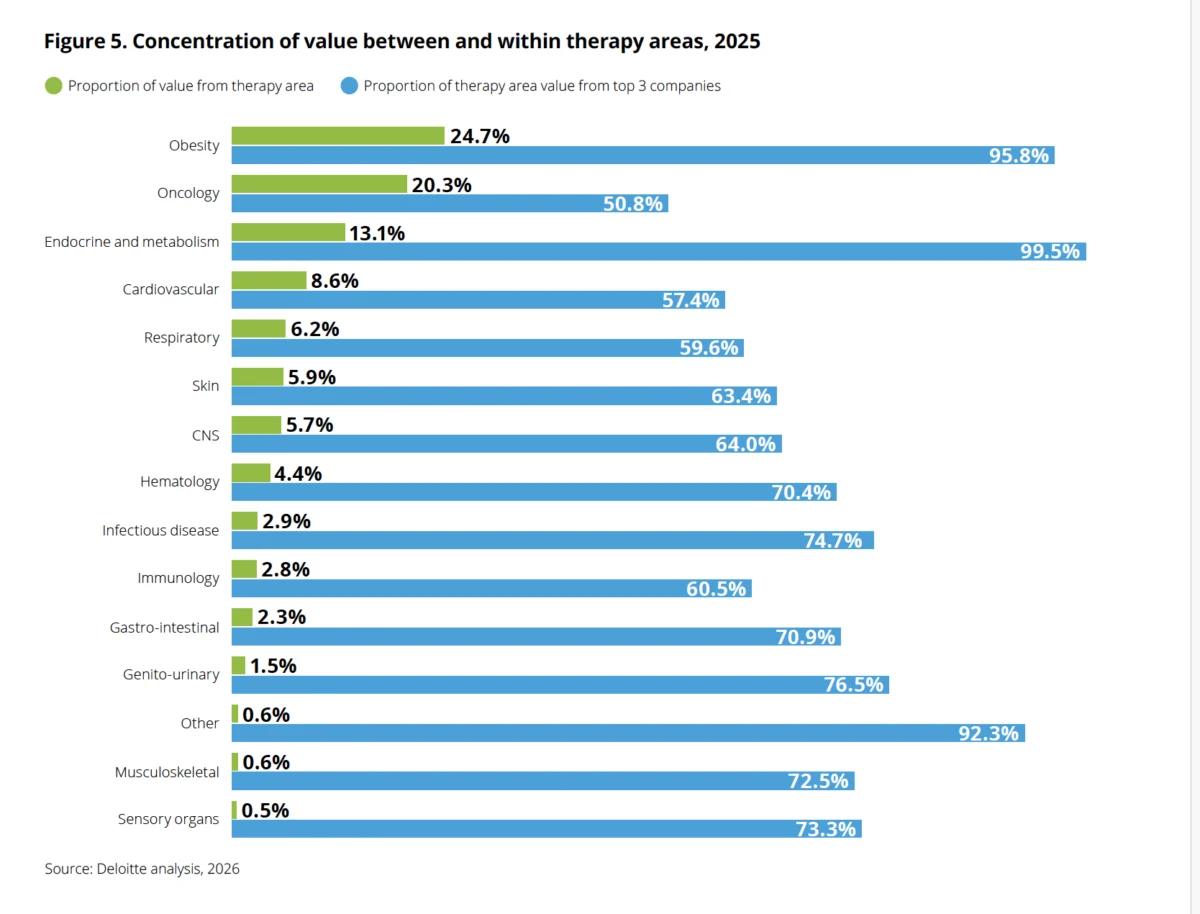

Supporting Data: The Concentration of Wealth

The Deloitte report highlights a startling shift in therapeutic dominance. For the first time in the report’s 16-year history, obesity has surpassed oncology as the leading category for late-stage pipeline value, commanding 24.7% of the total, compared to oncology’s 20.3%.

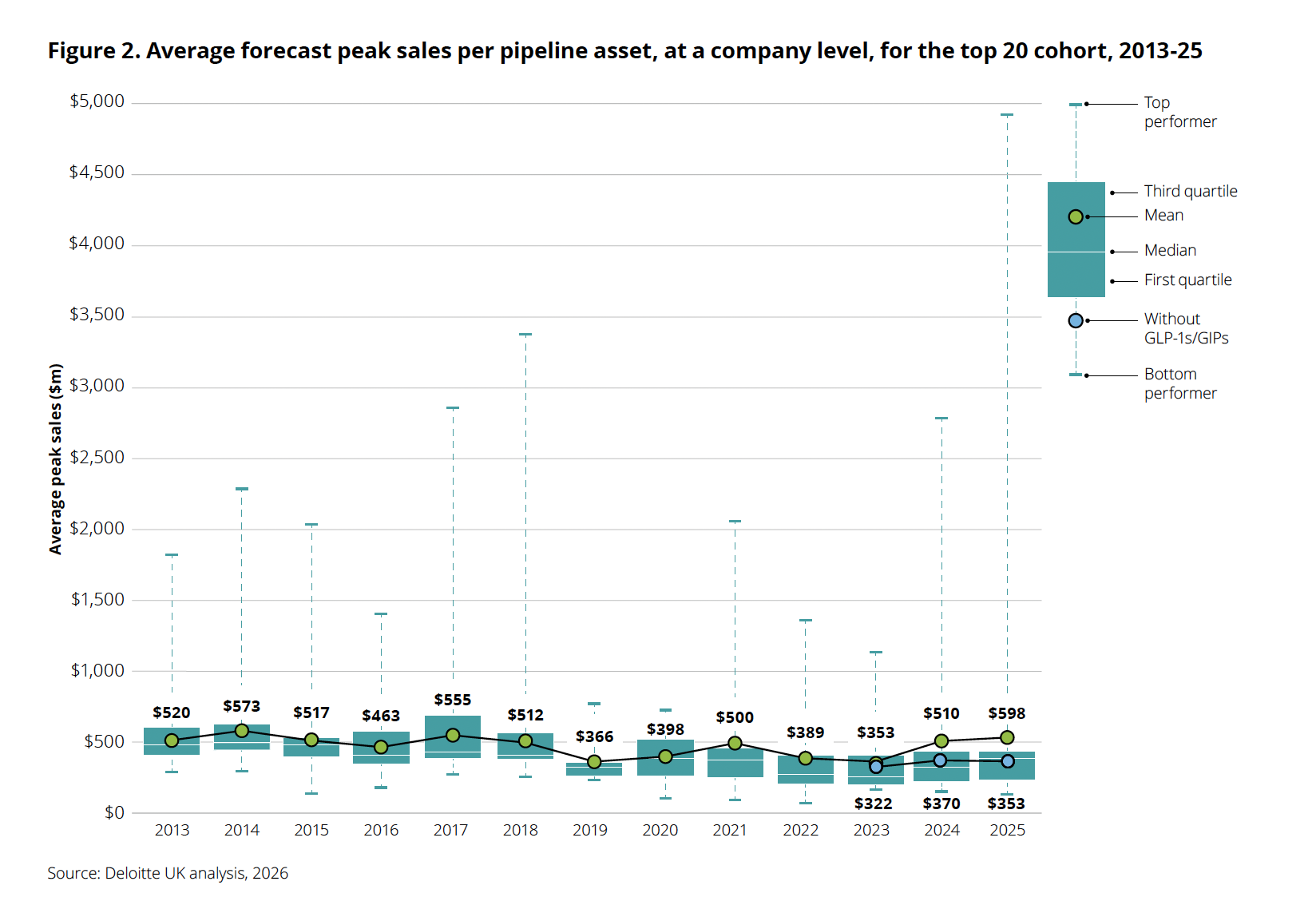

However, the wealth is remarkably concentrated. Nearly 96% of the value within the obesity segment is held by just three major companies. This lack of diversification is a strategic vulnerability. Furthermore, the average forecast peak sales per pipeline asset have jumped to $598 million, but this average is heavily skewed by a few top performers nearing the $5 billion mark. When the "GLP-1 effect" is removed, the average peak sales value per asset drops to $353 million—a figure lower than that of the previous year.

Rising Costs and the R&D "Death Valley"

Compounding the concern over product concentration is the runaway cost of drug development. The average cost to bring a drug from discovery to launch has hit $2.67 billion, an increase from $2.23 billion in 2025.

Dondarski notes that this is not an isolated phenomenon. "We saw the cost increase for 17 out of the 20 companies we analyzed, so it is a pervasive theme," he stated. Three distinct factors are driving this:

- Inflationary Pressures: R&D costs are rising significantly faster than general consumer price inflation.

- M&A Bloat: Large-scale acquisitions, while necessary to fill pipelines, are inflating the cost base for R&D departments.

- Pipeline Attrition: A 4–5% reduction in the total number of late-stage programs means that the remaining, successful drugs must shoulder the financial burden of a larger number of failed trials.

The AI Promise: Still Waiting for Liftoff

In the 2025 report, "Be Brave, Be Bold," Deloitte strongly advocated for the rapid adoption of AI-powered platforms, automation, and predictive analytics to solve the productivity crisis. Yet, one year later, the data suggests that AI has yet to move the needle on a systemic level.

Clinical cycle times remain stubbornly long, and costs continue to mount. Deloitte now acknowledges that the promise of AI has not been realized at scale. The report attributes this failure to a "pilot-driven, function-by-function approach." Many pharmaceutical firms are experimenting with AI in silos—optimizing specific protein structures or predicting molecular binding—but have yet to integrate these tools into the end-to-end development process in a way that truly accelerates time-to-market.

"Everybody is actively focusing on AI, and everybody has had some degree of success," says Dondarski. "But from our vantage point, there is a significant delta between organizations that are merely experimenting and those that are scaling those efforts to maximize value creation."

Implications: The Road Ahead

The implications for the industry are profound. First, the reliance on a single, high-growth therapy class has created a "barbell" effect in the pharmaceutical market: immense profitability at the top, but a thinning and increasingly expensive pipeline underneath.

Second, the price-volume trade-off is becoming visible. As seen in Eli Lilly’s recent Q1 results, a 65% increase in volume was partially offset by a 13% decline in realized prices. This suggests that the "easy money" phase of the GLP-1 boom—where high prices and high volume converged—is giving way to a more competitive, margin-pressured environment, particularly as government intervention through initiatives like the TrumpRx pricing program continues to gain traction.

For the pharmaceutical industry to maintain its current momentum, executives must navigate a narrow path. They must maximize the commercial footprint of their current GLP-1 assets while simultaneously reinvesting those profits into a more diversified R&D portfolio. The era of relying on a single blockbuster class to mask the inefficiencies of a $2.67 billion development cycle is coming to an end.

The "spring" that Deloitte describes is real, but it is currently a fragile one. Whether the industry can transition from a dependency on obesity drugs to a broader, more sustainable model of innovation will be the defining challenge for the next decade of biopharma. For investors and patients alike, the next few years will reveal whether this era of innovation is a sustainable evolution or merely a fleeting, albeit lucrative, exception to the rule.