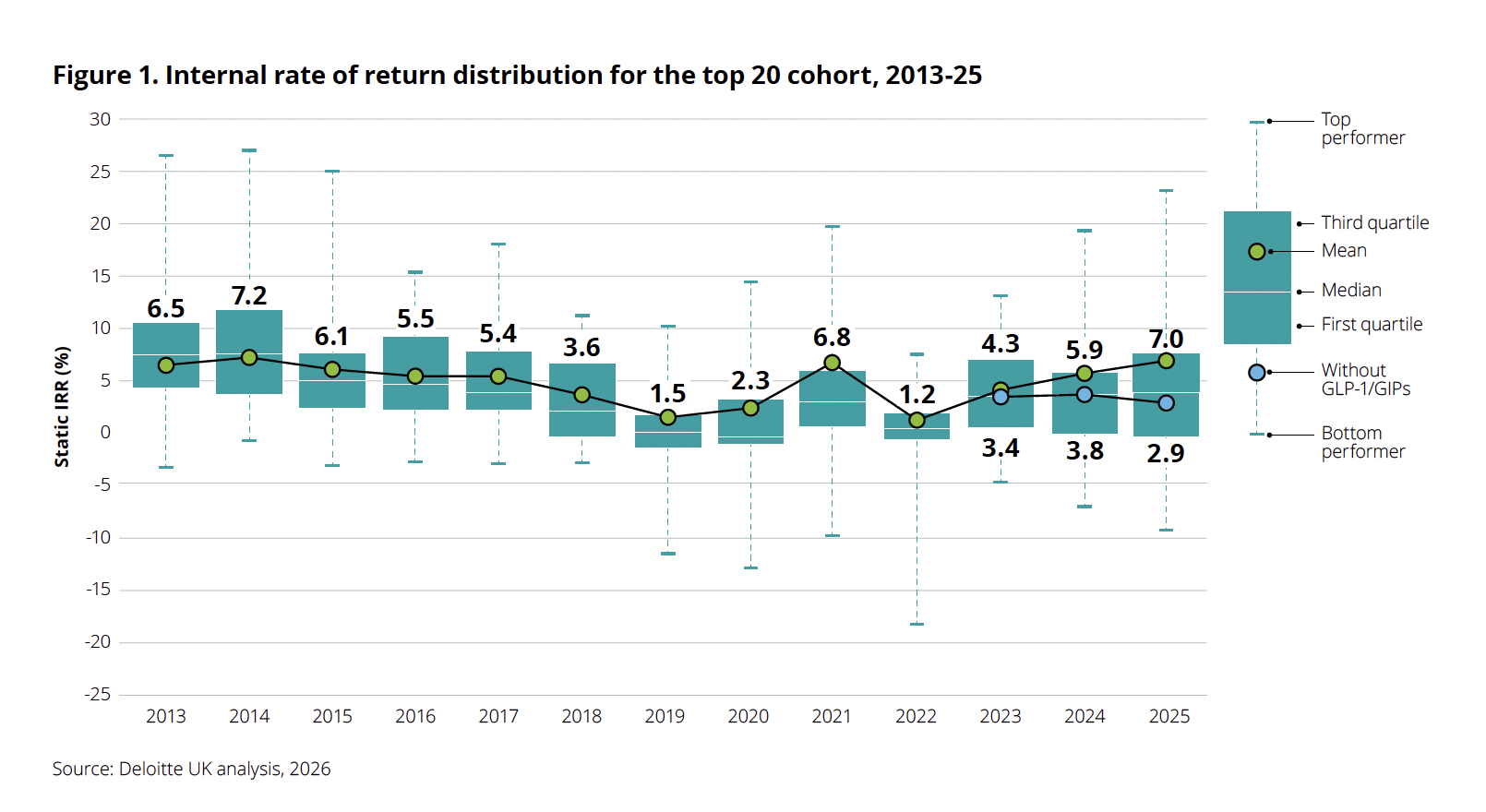

After years of grappling with stagnant returns and the post-pandemic "hangover" that plagued the biopharmaceutical sector, a fresh wave of optimism has hit the industry. According to the 16th edition of Deloitte’s annual Measuring the Return from Pharmaceutical Innovation report, the internal rate of return (IRR) on late-stage R&D assets has climbed to 7.0% in 2025, marking the third consecutive year of growth and a significant recovery from the 5.9% recorded in 2024.

However, beneath this veneer of prosperity lies a complex, and perhaps fragile, reality. The industry’s return to form is not a broad-based revival of pharmaceutical innovation, but rather a hyper-concentration of value centered on a single therapeutic class: GLP-1/GIP receptor agonists. As the industry navigates what Deloitte terms the "GLP-1 boom," stakeholders are left questioning whether this surge represents a sustainable new era of drug discovery or a transient reliance on a single, high-performing "golden goose."

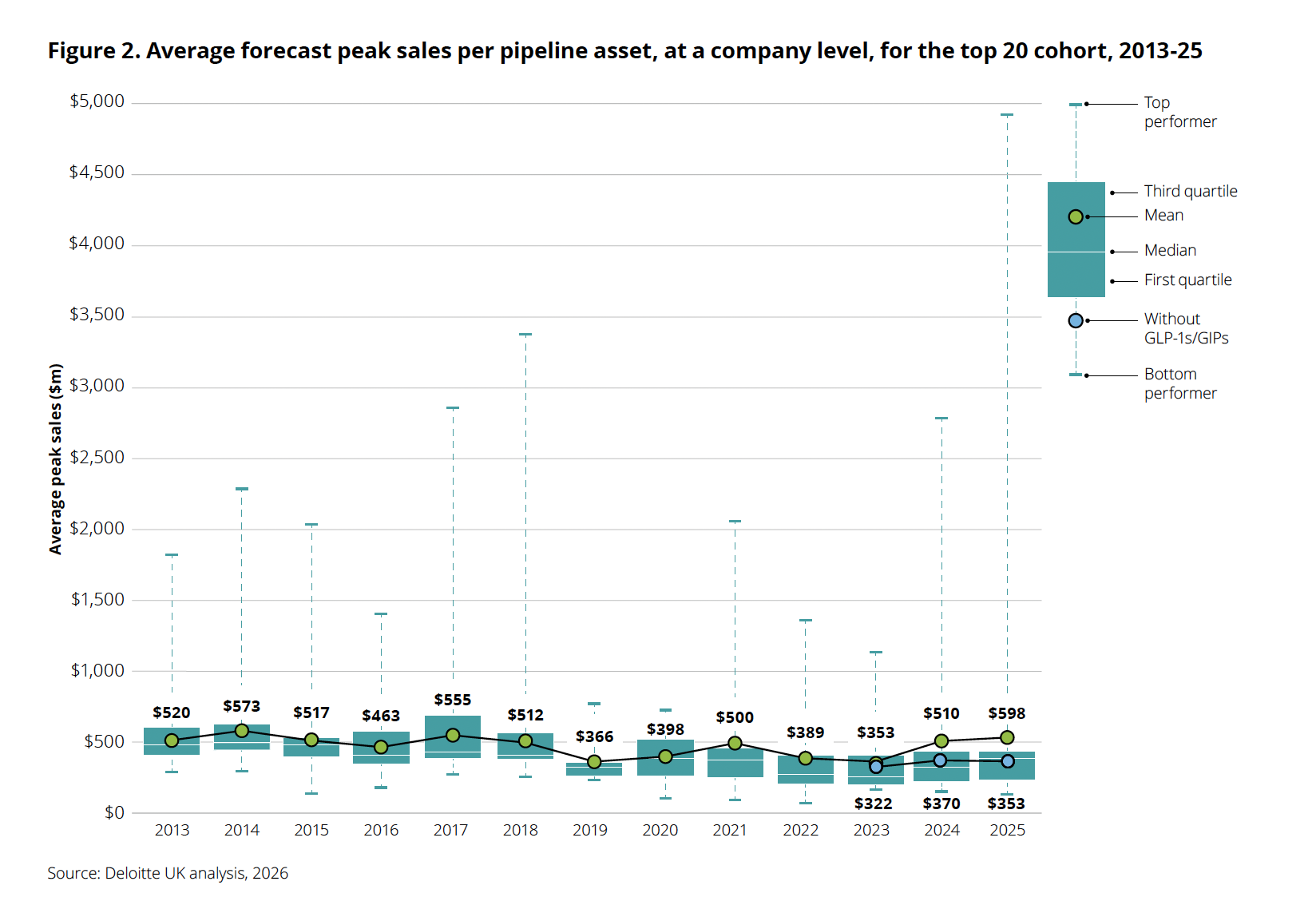

The Core Data: A Sector Transformed by Obesity Drugs

The headline figure of 7.0% is undeniably positive, signaling that the "winter" of declining R&D productivity—a trend that dominated the industry for over a decade—has finally given way to a more productive spring. Yet, the delta between that 7.0% and the reality of the broader pipeline is stark.

When Deloitte analysts stripped the GLP-1 and GIP drugs out of their calculations, the projected IRR for the remaining late-stage pipeline plummeted from 7.0% to a mere 2.9%. To put this into perspective, even in 2024, the IRR without these weight-loss blockbusters sat at 3.8%. This implies that, excluding the obesity segment, the underlying productivity of the pharmaceutical pipeline is not just stagnant; it is actively contracting.

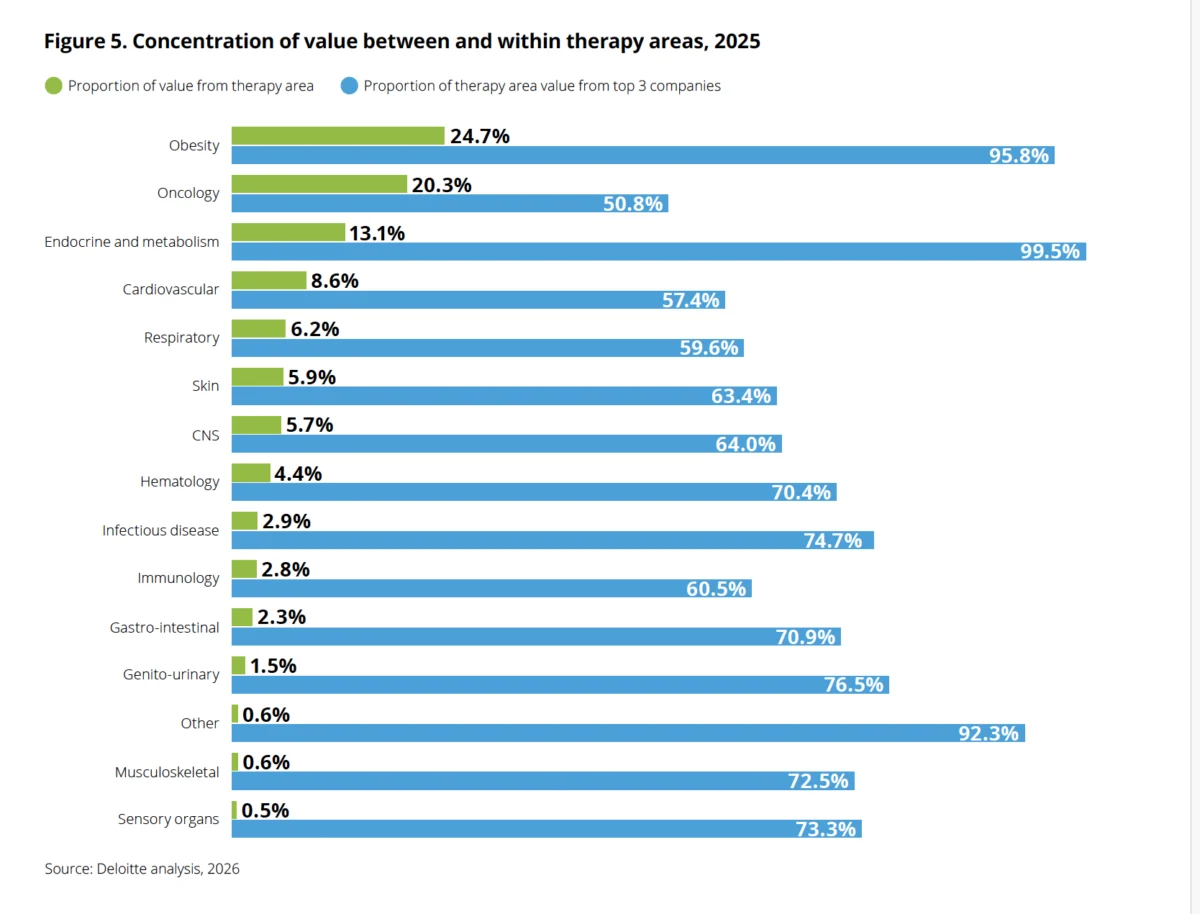

Kevin Dondarski, principal for life sciences strategy at Deloitte Consulting, describes this as an "analytically unprecedented" divergence. In the 16-year history of the report, analysts have often seen specific therapeutic classes carry disproportionate weight, but never to this extent. The GLP-1 class now accounts for an estimated 38% of all projected commercial inflows from the 2025 late-stage pipeline, effectively masking the softening performance of other therapeutic areas.

Chronology of a Market Shift: From Pandemic Pivot to Weight-Loss Mania

To understand how the industry arrived at this point, one must look at the transition over the last three years.

- 2023: The sector was still reeling from the end of the COVID-19 vaccine and treatment windfall. Growth was uneven, and many firms were struggling to pivot their R&D focus toward long-term, non-pandemic revenue drivers.

- 2024: The first signs of the GLP-1 surge became evident. The IRR ticked up to 5.9% as clinical successes for therapies like tirzepatide began to demonstrate massive commercial potential.

- 2025: The "Boom" year. GLP-1s displaced oncology—long the crown jewel of pharma R&D—as the largest share of late-stage pipeline value (24.7% vs. 20.3%). This shift occurred while the average cost to develop a drug hit a staggering $2.67 billion per asset.

- Early 2026: Reality begins to bite. Despite record revenue forecasts, major players like Eli Lilly and Novo Nordisk have faced investor volatility, stock price corrections, and the harsh realization that even "blockbuster" drugs face pricing pressures, regulatory scrutiny, and high-stakes clinical failures.

The Cost of Innovation: R&D Inflation and Rising Hurdles

One of the most alarming takeaways from the 2026 data is the ballooning cost of the drug development lifecycle. The average cost per asset rose to $2.67 billion in 2025, up from $2.23 billion the prior year. This increase was not an anomaly confined to a few failed projects; 17 of the 20 companies analyzed by Deloitte reported higher R&D costs.

This rise is driven by three primary, converging factors:

- Persistent R&D Inflation: The cost of clinical trials, skilled labor, and specialized infrastructure continues to outpace general inflation.

- M&A-Driven Cost Bases: Large-scale acquisitions, while necessary to replenish pipelines, have served to inflate the R&D cost base, as companies pay a premium for existing assets that require further, expensive development.

- Pipeline Attrition: A 4-5% decrease in the number of late-stage programs means that the costs of a smaller, more concentrated pipeline are being spread across fewer assets, naturally inflating the cost-per-success metric.

Official Responses and Market Realities

The corporate response to these pressures has been swift, often painful, and highly public.

Novo Nordisk: Restructuring for Efficiency

Novo Nordisk, once the darling of the European markets, underwent a significant shake-up in 2025. The company replaced long-time CEO Lars Fruergaard Jorgensen with Maziar Mike Doustdar, a move intended to stabilize the company amidst slowing momentum. The subsequent overhaul included the departure of seven board members and a massive workforce reduction. While the company initially aimed to cut 9,000 roles, recent reporting suggests that the actual reduction may have reached 10,500, a move aimed at saving approximately $1.3 billion annually.

Eli Lilly: Volume vs. Price

Eli Lilly has reported massive revenue spikes—notably a 125% increase in Mounjaro sales—but the company faces the "volume-price" paradox. While volume growth is robust, realized prices for these therapies have seen a 13% decline. Investors are reacting to this signal, worrying that the long-term profitability of these drugs will be cannibalized by competitive pricing and government-negotiated mandates.

The Pricing Pressure

The "golden goose" is also being reined in by regulatory bodies. Both Lilly and Novo Nordisk have entered agreements to lower U.S. prices for GLP-1s through Medicare, Medicaid, and the "TrumpRx" initiatives. With monthly copays for weight-loss medications now capped and set at competitive rates ($149–$299), the profit margins that analysts once projected are being squeezed from the top down.

AI: The Promise vs. The Reality

Perhaps the most poignant aspect of the report is the status of Artificial Intelligence in drug discovery. Last year, Deloitte urged the industry to be "brave and bold" in adopting AI to break the cycle of high costs and long development times.

The 2025 data suggests that the industry is still in the "pilot phase." Despite widespread adoption of AI tools, the hoped-for reduction in development time and costs has not materialized at scale. Dondarski attributes this to a "function-by-function" approach—where AI is used to optimize specific, isolated tasks rather than being integrated into a holistic, company-wide drug development platform.

"Everybody is actively focusing on AI, and everybody’s had some degree of success," Dondarski noted. "But there’s a good amount of variability in the velocity at which organizations are scaling those efforts to maximize value creation." Until pharma companies transition from experimental pilots to end-to-end AI integration, the "productivity breakthrough" promised by technology remains a future aspiration rather than a present reality.

Implications for the Future of Pharma

The concentration of 96% of the obesity-related pipeline value among just three companies highlights a significant systemic risk. If these companies cannot find the "next generation" of assets to follow the GLP-1/GIP wave, the industry’s return on innovation will likely collapse back to historical lows.

Sustainability and Responsibility

The responsibility now lies with leadership teams to diversify their R&D spend. The current reliance on metabolic disease, while highly profitable, leaves the industry vulnerable to the inevitable plateauing of the GLP-1 market. As clinical failures—such as the disappointment seen with Novo’s CagriSema in the REDEFINE 4 trial—demonstrate, the path to the next blockbuster is fraught with risk.

A Call for Strategic Realignment

The 2025 Deloitte report serves as both a celebration and a warning. The biopharma sector has proven it can generate enormous value when it identifies a high-need, high-impact therapeutic target. However, the reliance on a single class to boost the sector’s internal rate of return is a signal that the broader, underlying R&D machinery requires a structural overhaul.

To achieve sustainable growth, the industry must:

- Scale AI beyond the pilot: Move toward fully integrated, data-driven R&D ecosystems.

- Address the cost-to-innovation ratio: Find ways to lower the cost of clinical trials through more efficient trial design and digital health integration.

- Diversify the portfolio: Reduce the over-reliance on metabolic blockbusters by reinvesting profits into high-risk, high-reward areas like gene editing, neurology, and personalized medicine.

The GLP-1 boom has given the industry a much-needed breathing room—a chance to recover from the post-pandemic slump. But as the market matures and pricing pressures intensify, the pharmaceutical sector must ensure that this "spring" is the beginning of a sustainable cycle of innovation, rather than a fleeting, single-season event. The clock is ticking, and for the world’s largest pharmaceutical companies, the search for the successor to the GLP-1 crown has already begun.