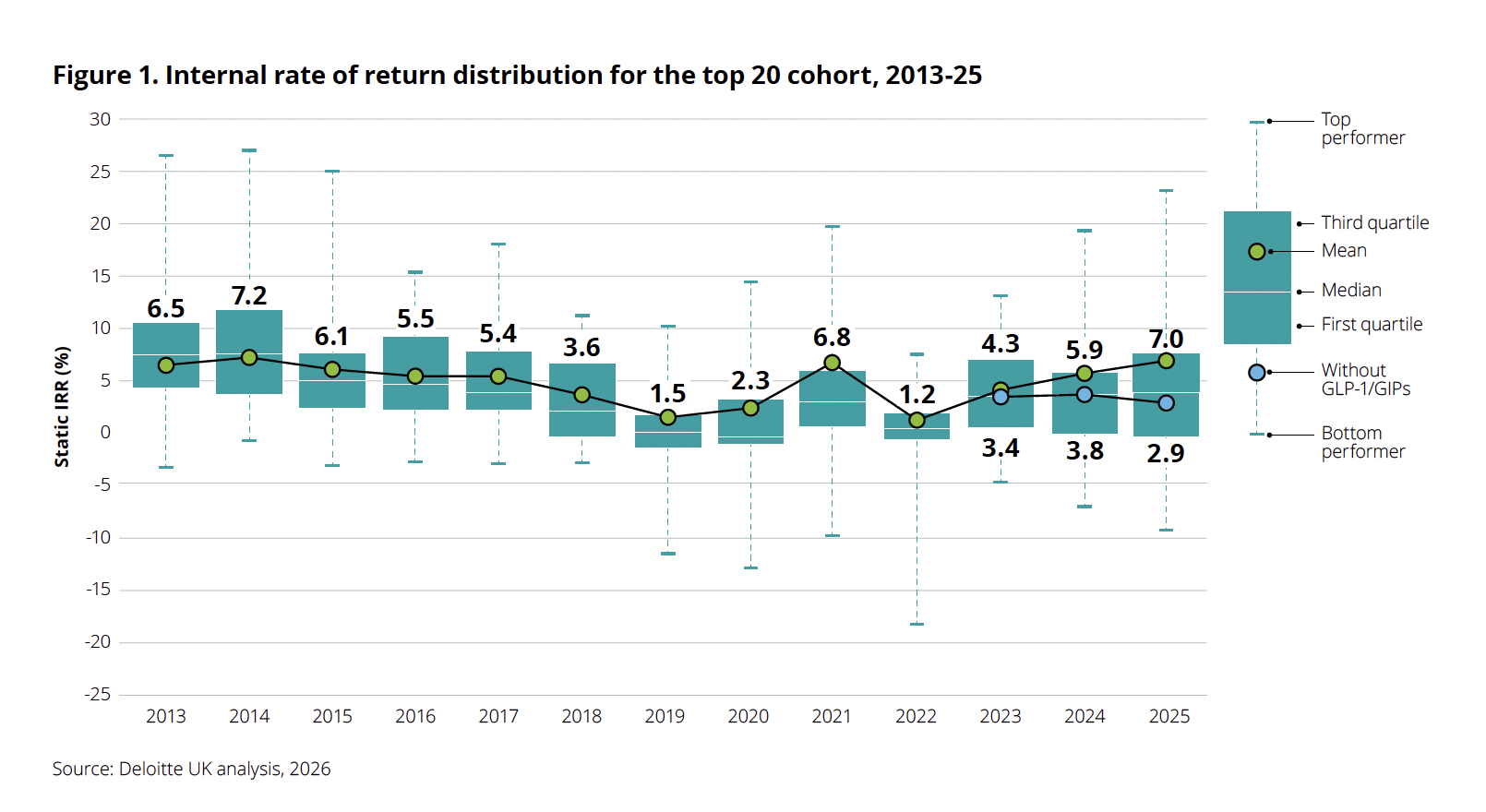

After years of grappling with declining R&D returns and the "post-pandemic hangover," the global biopharmaceutical sector has finally emerged from its winter. According to the 16th edition of Deloitte’s annual Measuring the Return from Pharmaceutical Innovation report—fittingly titled “Navigating the GLP-1 boom”—the internal rate of return (IRR) for late-stage pipeline assets climbed to 7.0% in 2025. This marks a significant recovery from the 5.9% recorded the previous year.

However, beneath the surface of this headline-grabbing growth lies a complex, perhaps precarious, reality. The sector’s newfound vitality is tethered disproportionately to a single class of therapeutics: GLP-1 and GIP receptor agonists. As the industry recalibrates, executives and investors alike are forced to confront a sobering question: Is this growth sustainable, or is the biopharma engine becoming overly reliant on a single, high-stakes metabolic narrative?

The Core Data: A Sector Transformed by Weight-Loss Blockbusters

For over a decade, the narrative surrounding biopharma innovation has been one of diminishing returns. "We went through a period of so many years where the returns kept declining, excluding the COVID impact in the middle," explains Kevin Dondarski, principal for life sciences strategy at Deloitte Consulting. "But the increase over the last few years is analytically unprecedented."

The data from the 2025 report reveals a stark bifurcation in the industry’s health. When GLP-1 and GIP drugs—the bedrock of the current obesity and metabolic disease revolution—are included in the calculation, the IRR reaches a promising 7.0%. Yet, if one strips these therapies from the analysis, the IRR craters to just 2.9%. To put this in perspective, in 2024, that same "ex-GLP-1" metric sat at 3.8%.

This reveals an uncomfortable truth: when looking at the broader pipeline, productivity is not merely stalling—it is actively declining. The industry’s aggregate growth is being carried by the sheer commercial scale of the obesity market, which now accounts for an estimated 38% of all projected commercial inflows from the late-stage pipeline.

A Chronology of the Boom and the Resulting Turbulence

The rise of the GLP-1 era has not been a smooth ascent. It has been marked by massive capital investment, aggressive restructuring, and intense clinical competition.

- 2023–2024 (The Peak of Euphoria): Following the massive success of Ozempic and Mounjaro, the industry began a total pivot toward metabolic health. Capital flooded into the sector, and M&A activity skyrocketed as companies scrambled to secure a foothold in the anti-obesity market.

- Late 2025 (The Reckoning): As the market matured, the pressure on "pure-play" leaders increased. Novo Nordisk, facing significant market pressure, initiated a massive leadership shakeup, replacing long-time CEO Lars Fruergaard Jorgensen with Maziar Mike Doustdar. Concurrently, the company announced a workforce reduction of approximately 9,000 roles to streamline operations.

- February 2026 (The Clinical Setback): Investor optimism took a hit when Novo’s highly anticipated CagriSema combination failed to show non-inferiority against Eli Lilly’s Zepbound in the REDEFINE 4 Phase 3 trial. Delivering 23.0% weight loss compared to the 25.5% achieved by tirzepatide, the failure highlighted the diminishing returns of incremental innovation in a crowded space.

- April 2026 (Strategic Expansion): Eli Lilly launched its oral GLP-1, orforglipron (marketed as Foundayo), signaling a shift toward more patient-friendly, non-injectable delivery methods. Despite this, Lilly’s stock experienced a 10–13% decline year-to-date, reflecting investor anxiety over the durability of pricing power in the face of government intervention.

Supporting Data: The Rising Price of Innovation

While the industry celebrates the commercial success of weight-loss drugs, the fundamental cost of bringing a drug to market continues to escalate. The average cost to shepherd a new medicine from discovery to launch hit a record $2.67 billion in 2025, up from $2.23 billion in 2024.

Deloitte’s analysis suggests this is not an anomaly driven by one or two expensive assets. "We saw the cost increase for 17 out of the 20 companies, so it was a persistent theme," Dondarski noted. The rising cost is driven by a trifecta of pressures:

- Inflationary R&D Costs: Operational expenses are outpacing general inflation.

- M&A Premiums: Large-scale acquisitions are inflating the R&D cost base for acquiring firms.

- Pipeline Attrition: A 4–5% reduction in the number of late-stage programs suggests that while we are spending more, we are successfully advancing fewer candidates to the finish line.

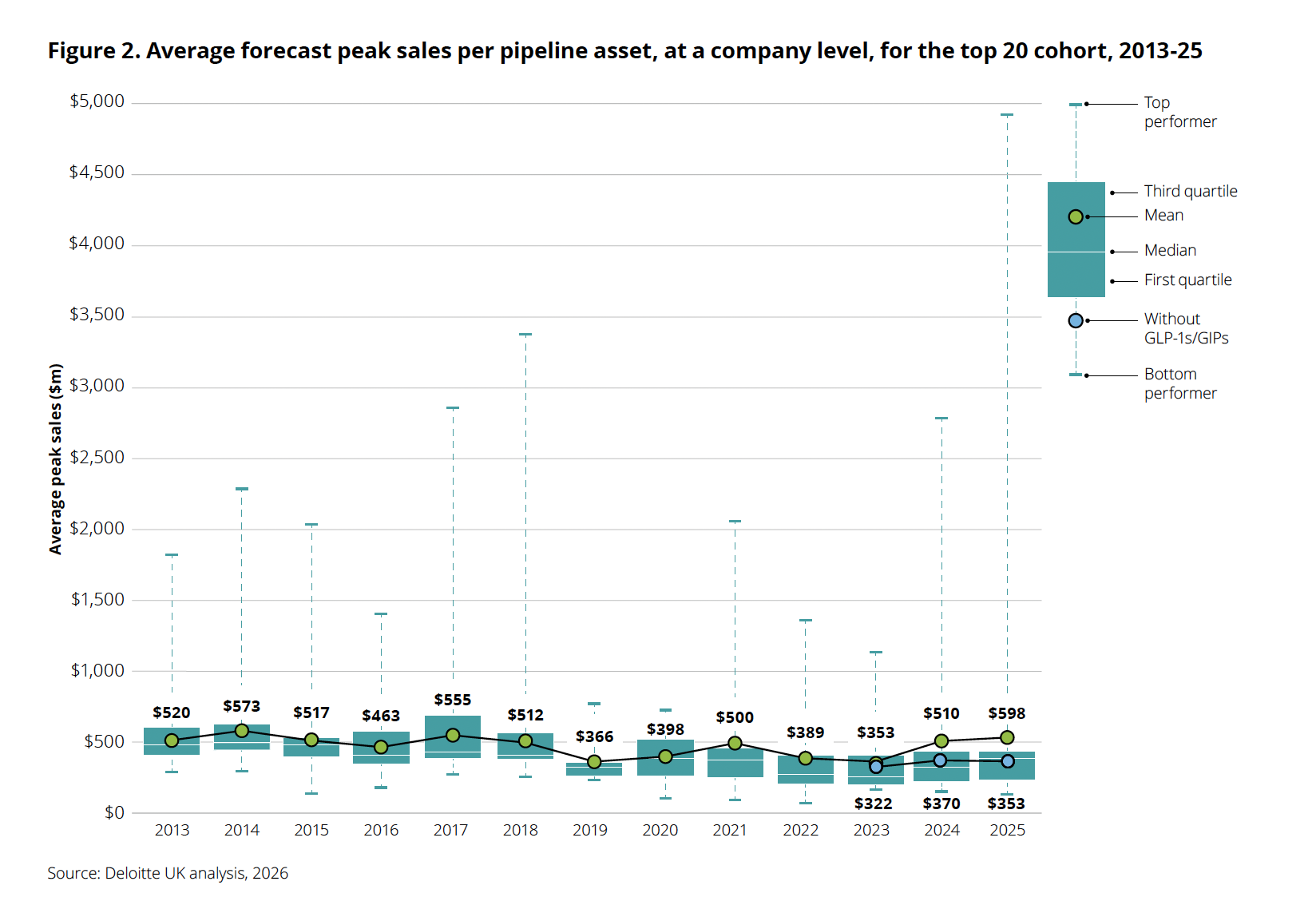

The "spread" in peak sales potential is also widening. While the average forecast peak sales per asset jumped to $598 million, the top-performing assets are approaching $5 billion, while the "without GLP-1s" marker has dropped to $353 million. This polarization suggests that the industry is becoming a "winner-take-all" landscape.

Official Responses and Strategic Implications

Industry leaders are now tasked with managing a dual-track strategy. On one hand, they must maximize the potential of the GLP-1 boom; on the other, they must diversify before the current wave reaches its zenith.

The Pricing Headwind

A significant development in late 2025 and early 2026 was the intervention of regulatory and public-policy mechanisms. Both Lilly and Novo Nordisk agreed to lower U.S. prices for GLP-1s via the TrumpRx initiative and expanded Medicare/Medicaid coverage. With the Wegovy pill now listed at $149 per month and Zepbound at $299, the era of premium-priced, high-margin weight loss may be coming to a close.

Lilly’s recent financial results highlight this tension: while revenue grew by 56% year-over-year in Q1 2026, driven by a 65% increase in volume, realized prices actually declined by 13%. This indicates that volume growth is currently shielding the sector from the reality of price compression, but this buffer will not last forever.

The AI Promise: A Gap Between Rhetoric and Reality

Last year’s Deloitte report challenged the industry to "Be brave, be bold" by adopting AI and advanced analytics to optimize R&D. Yet, the 2025 data paints a humbling picture. Despite massive investments in AI platforms, clinical cycle times remain stubbornly long, and development costs have not decreased.

Deloitte concedes that the promise of AI has "not yet been realized at scale." The issue, according to Dondarski, is not a lack of interest, but a lack of systemic implementation. Companies are largely trapped in a "pilot-driven, function-by-function approach" rather than a holistic, platform-based integration of AI into the drug discovery process.

Future Outlook: Replacing the Golden Goose

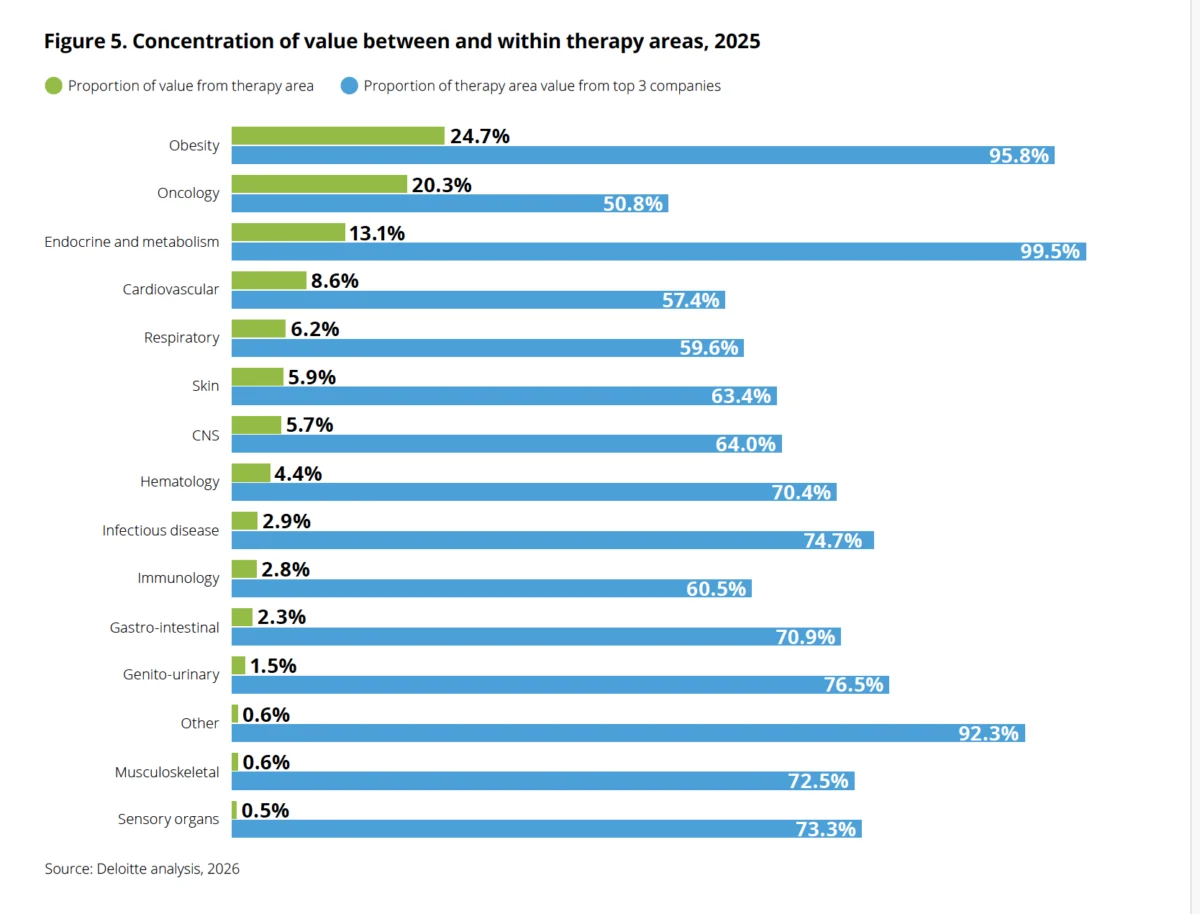

The core responsibility for biopharma executives in the coming years will be pipeline renewal. Obesity has officially displaced oncology as the largest share of late-stage pipeline value (24.7% versus 20.3%). However, the concentration is extreme: nearly 96% of that value is controlled by just three companies.

This concentration represents a significant systemic risk. If the next generation of metabolic therapies fails to deliver, or if pricing models for these drugs continue to collapse under political pressure, the industry’s R&D returns will be left exposed.

To achieve sustainable growth, the industry must look beyond the "GLP-1 boom." The transition from "winter to spring" is not guaranteed to last if it is built on a single pillar. The next chapter of biopharmaceutical innovation will require firms to:

- Scale AI beyond pilots: Moving from departmental use cases to enterprise-wide drug development transformation.

- Diversify the portfolio: Re-investing the windfalls from obesity drugs into diverse therapeutic areas such as neurodegeneration, immunology, and cell/gene therapy.

- Rationalize R&D spending: Addressing the underlying inefficiencies that cause the cost of drug development to rise faster than the rate of scientific breakthrough.

As the 2026 fiscal year progresses, the industry stands at a crossroads. The GLP-1 phenomenon has proven that biopharma can still produce "blockbuster" returns that capture the imagination of Wall Street and the public. But to ensure long-term stability, the sector must move from the novelty of the current boom to a more balanced, efficient, and diversified model of innovation. The "spring" has arrived, but the weather remains unpredictable.