Published: June 16, 2026

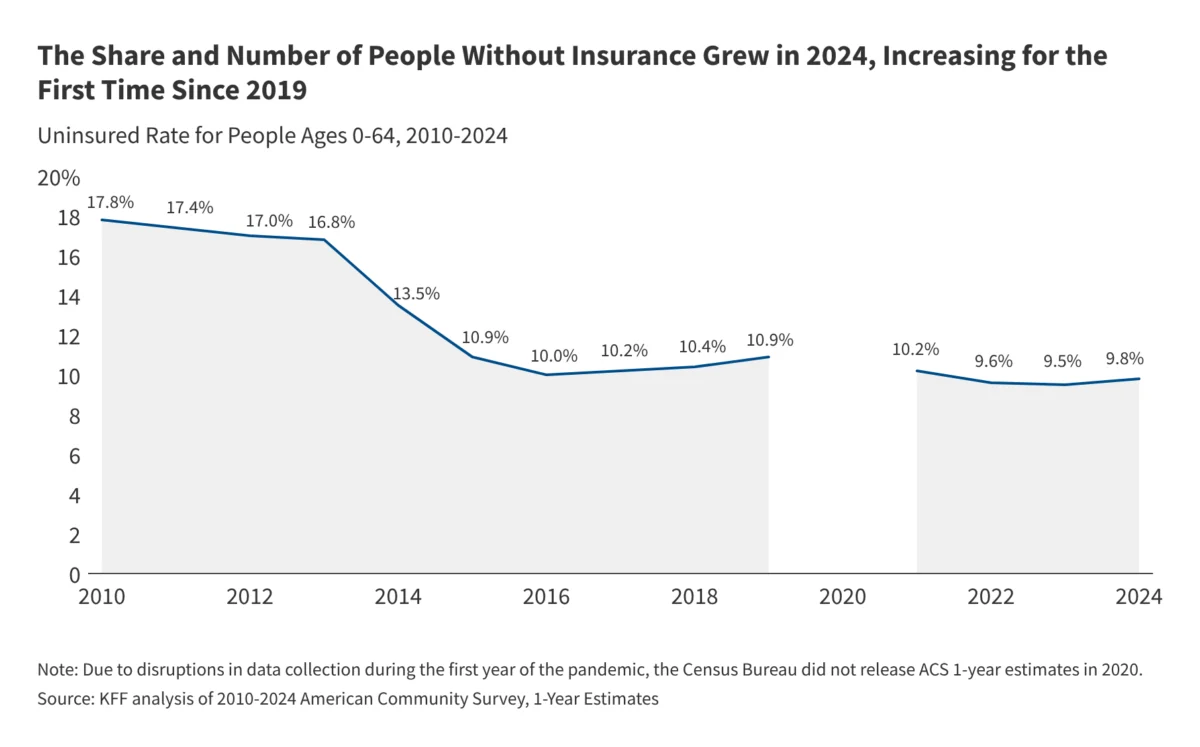

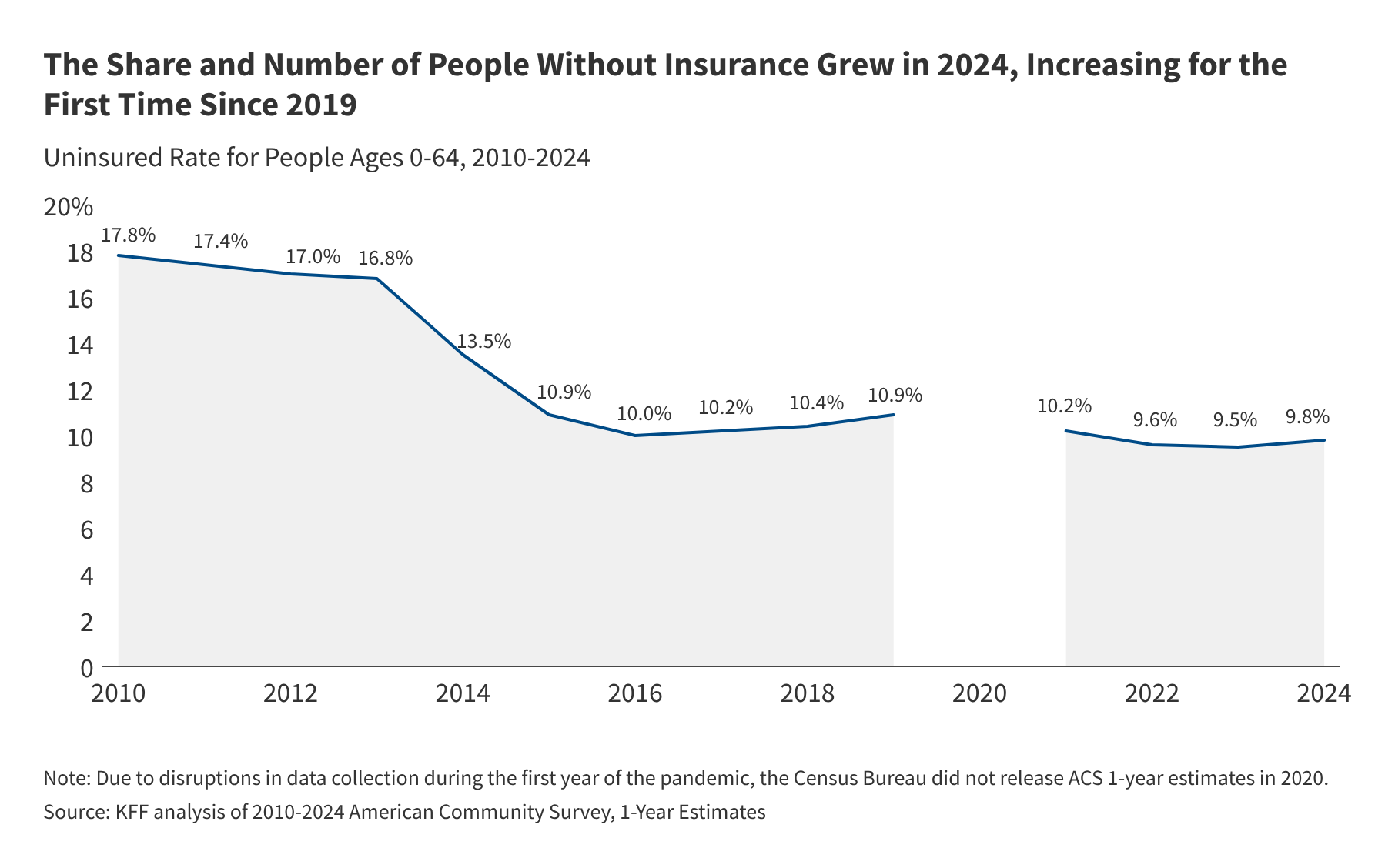

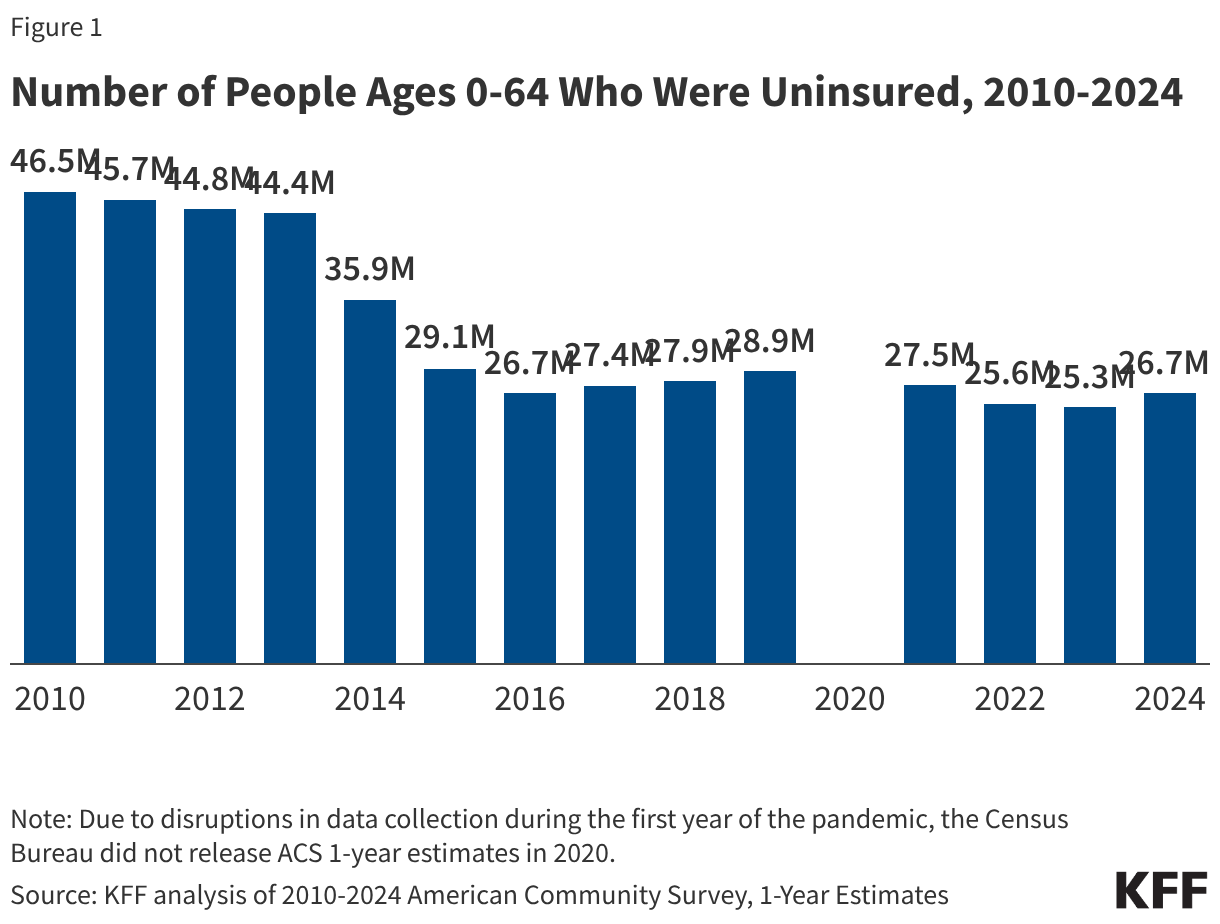

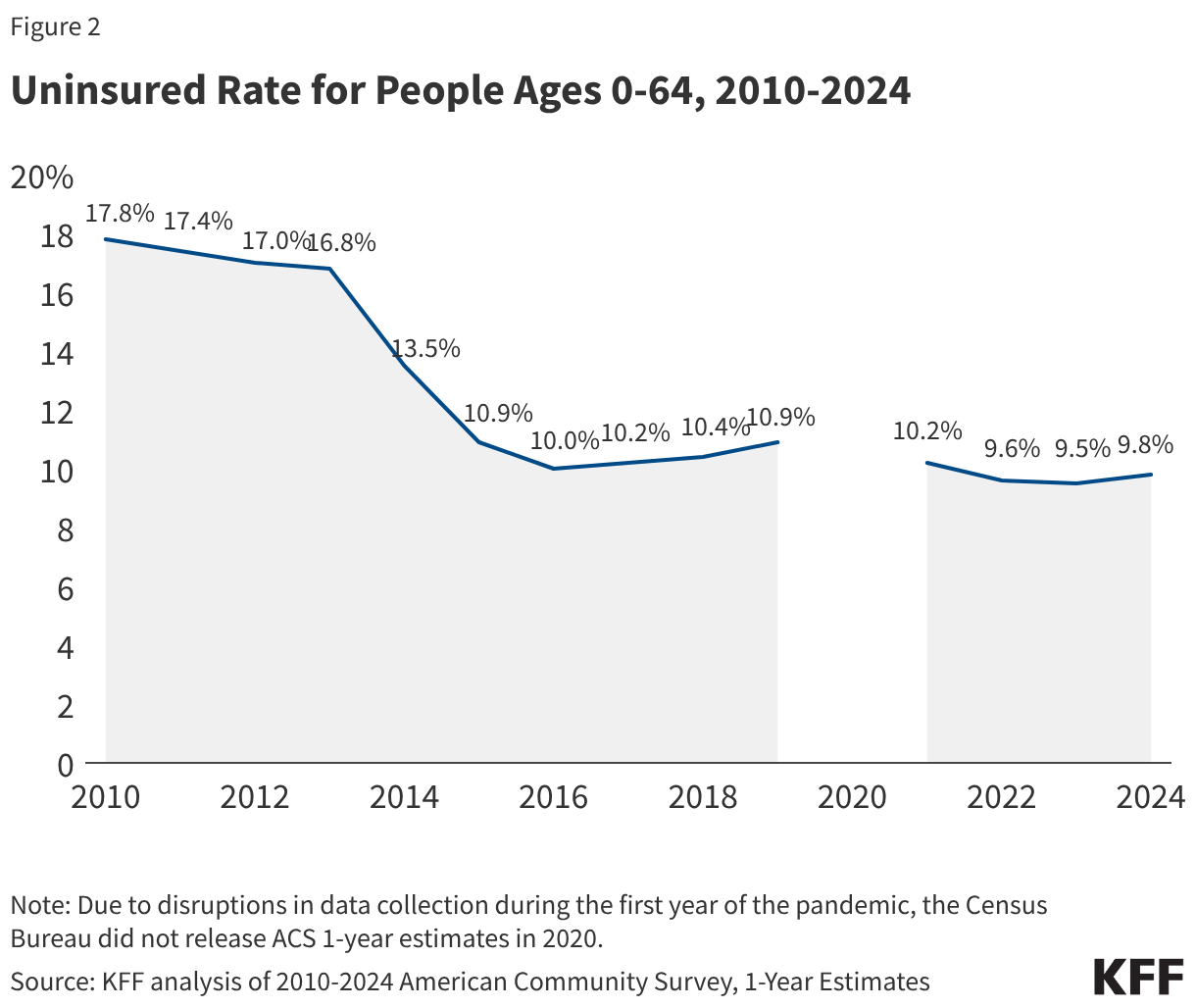

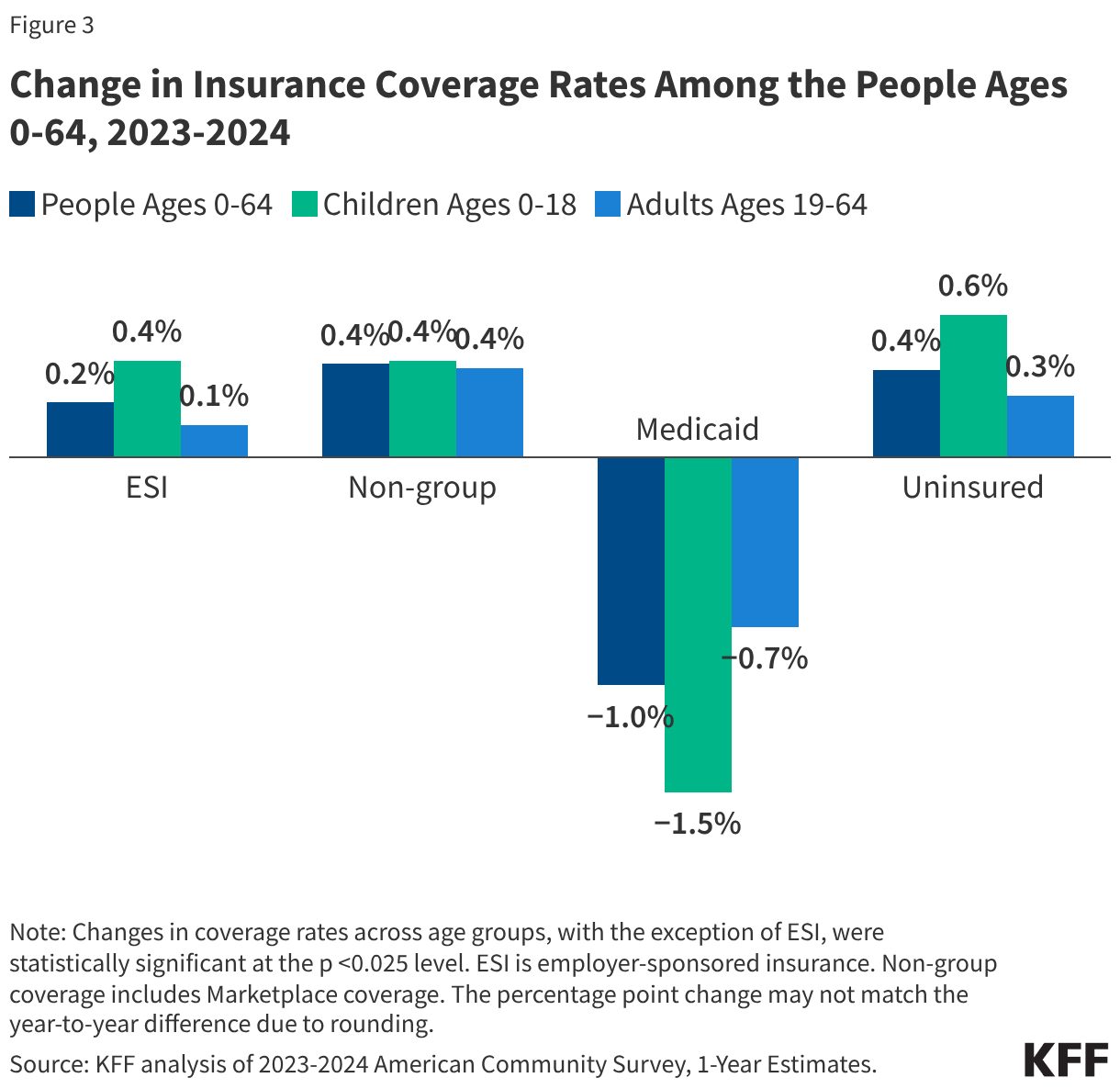

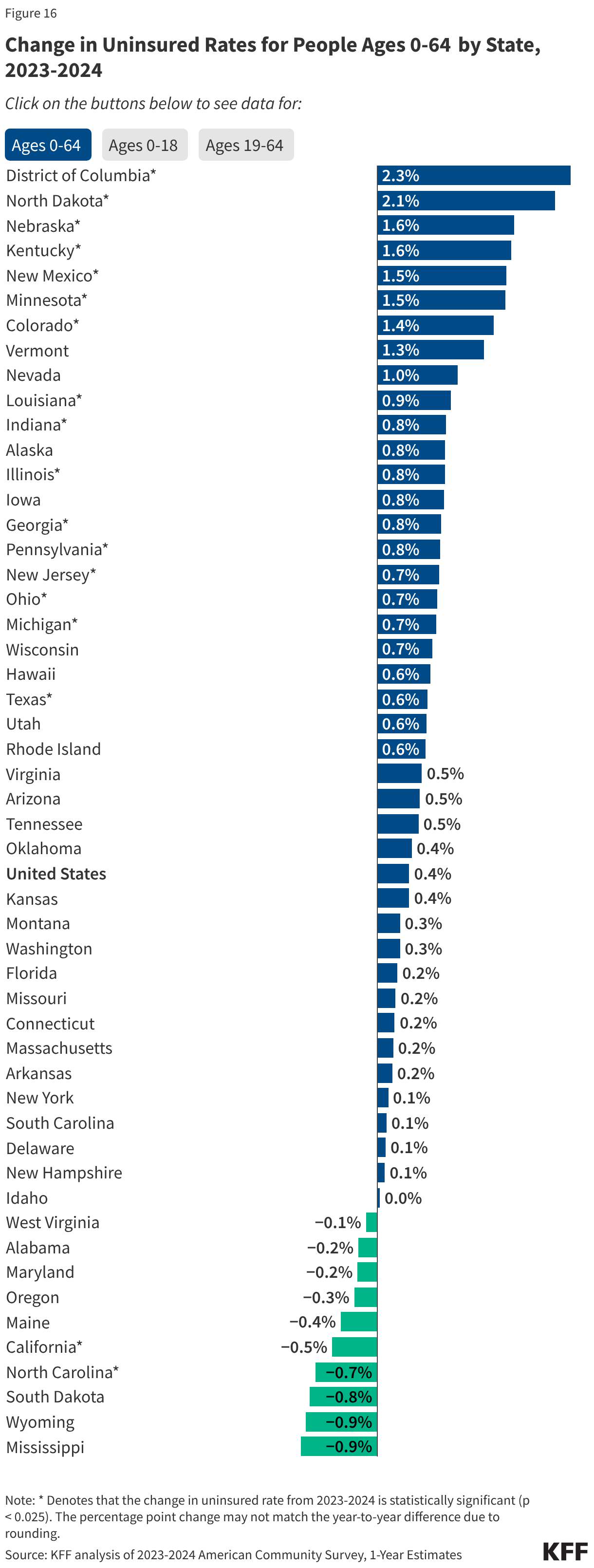

For the first time since 2019, the United States has witnessed a troubling reversal in healthcare access. After years of incremental gains in coverage, 2024 marked a pivotal shift as both the number of uninsured individuals and the national uninsured rate ticked upward. According to the latest data from the American Community Survey (ACS), the number of people under age 65 without health coverage swelled by over 1.3 million, reaching 26.7 million total. The uninsured rate for this demographic climbed from 9.5% in 2023 to 9.8% in 2024.

This increase, while statistically modest, signals a fundamental strain in the American healthcare system. Driven primarily by the conclusion of the Medicaid "unwinding" process and the expiration of pandemic-era policy protections, this trend suggests a return to a landscape defined by fragmentation, coverage gaps, and deepening financial instability for the nation’s most vulnerable populations.

Chronology: The End of Pandemic-Era Stability

To understand the current crisis, one must look back at the legislative and administrative maneuvers of the last five years. During the COVID-19 pandemic, the federal government implemented a "continuous enrollment" provision for Medicaid, which prohibited states from disenrolling members in exchange for increased federal funding. This stabilized coverage for millions who would otherwise have been pushed out of the system.

In March 2023, that provision expired. Over the subsequent 18 months, states launched a massive administrative operation known as the "Medicaid unwinding." Agencies were tasked with redetermining eligibility for every enrollee, a process that resulted in the removal of millions from the Medicaid rolls. While the Affordable Care Act (ACA) Marketplace provided a secondary landing spot for many, it failed to act as a complete safety net.

By the end of 2024, the administrative churn of the unwinding had collided with the harsh realities of a complex system. Many individuals simply fell through the cracks—either unaware of how to transition to new plans or finding that even subsidized private coverage remained unaffordable compared to their previous public benefits.

Supporting Data: Who Is Losing Coverage?

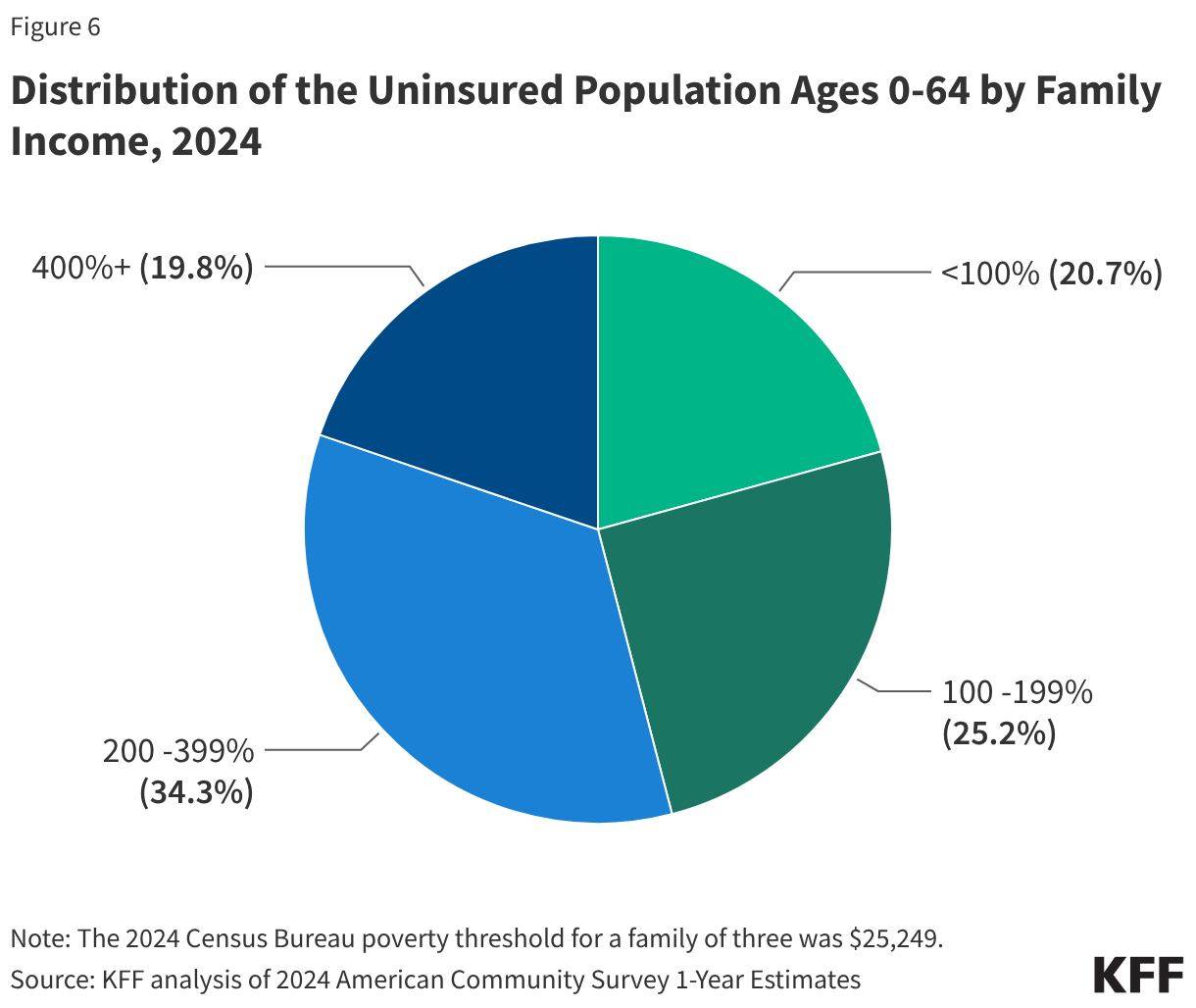

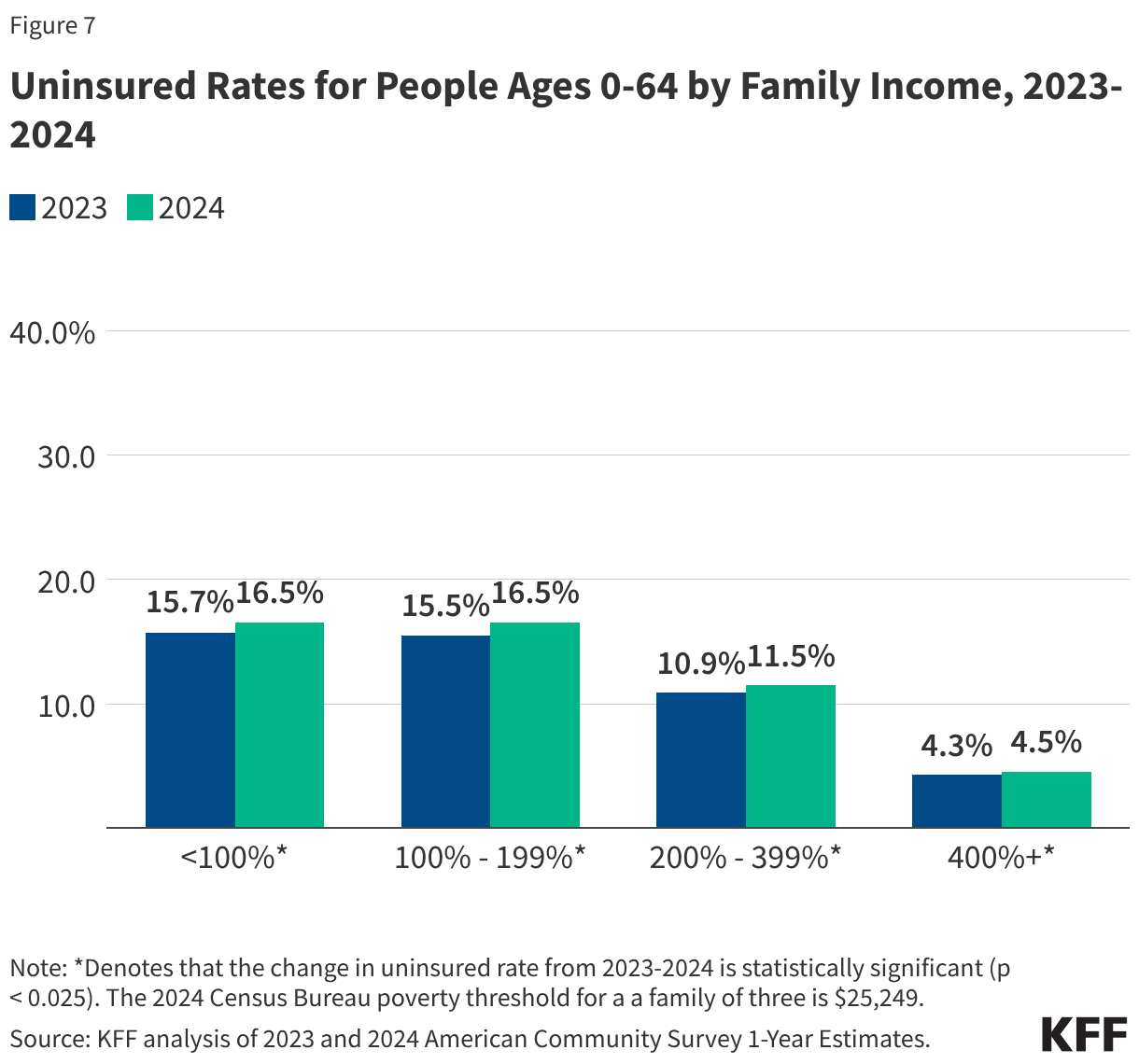

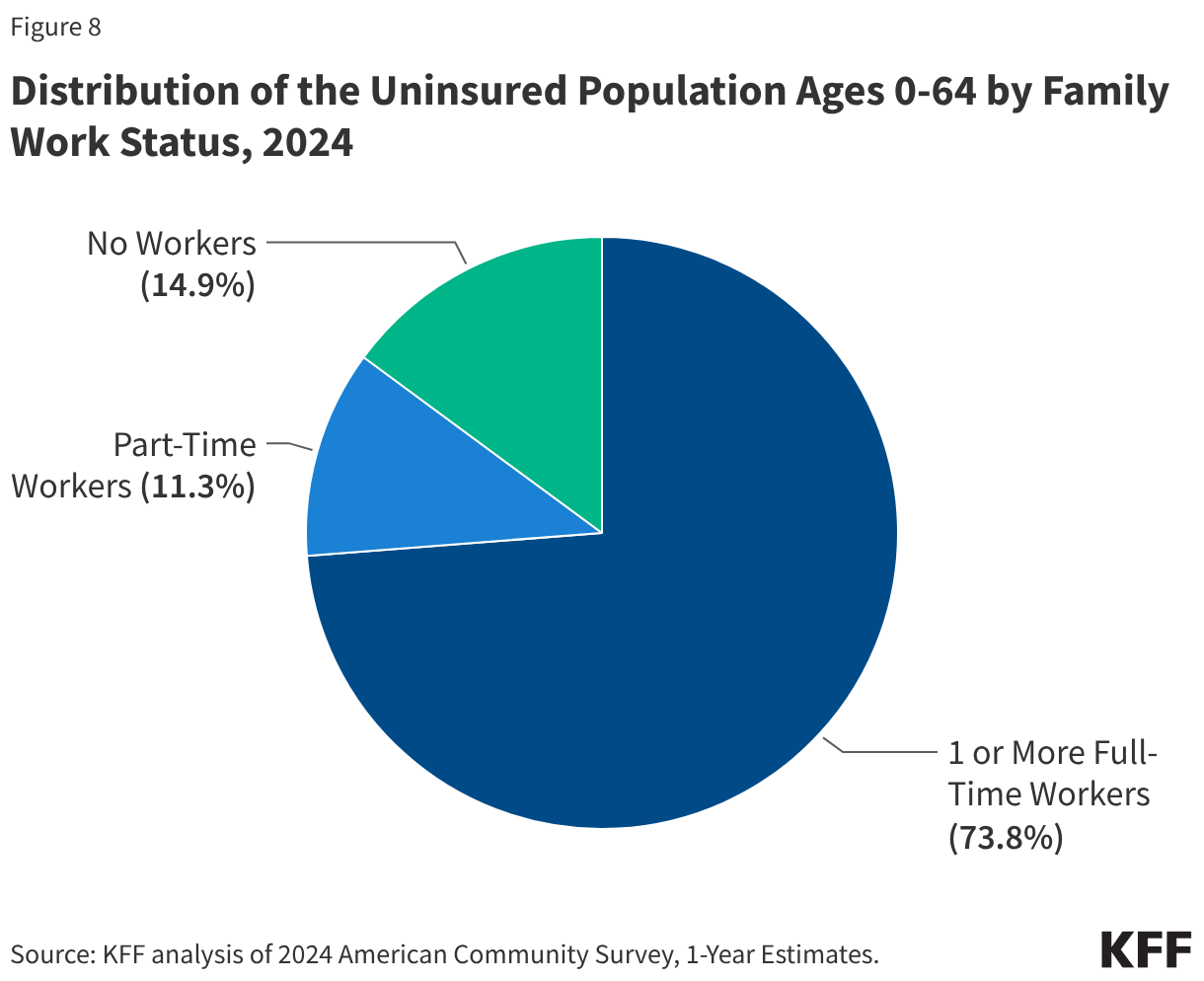

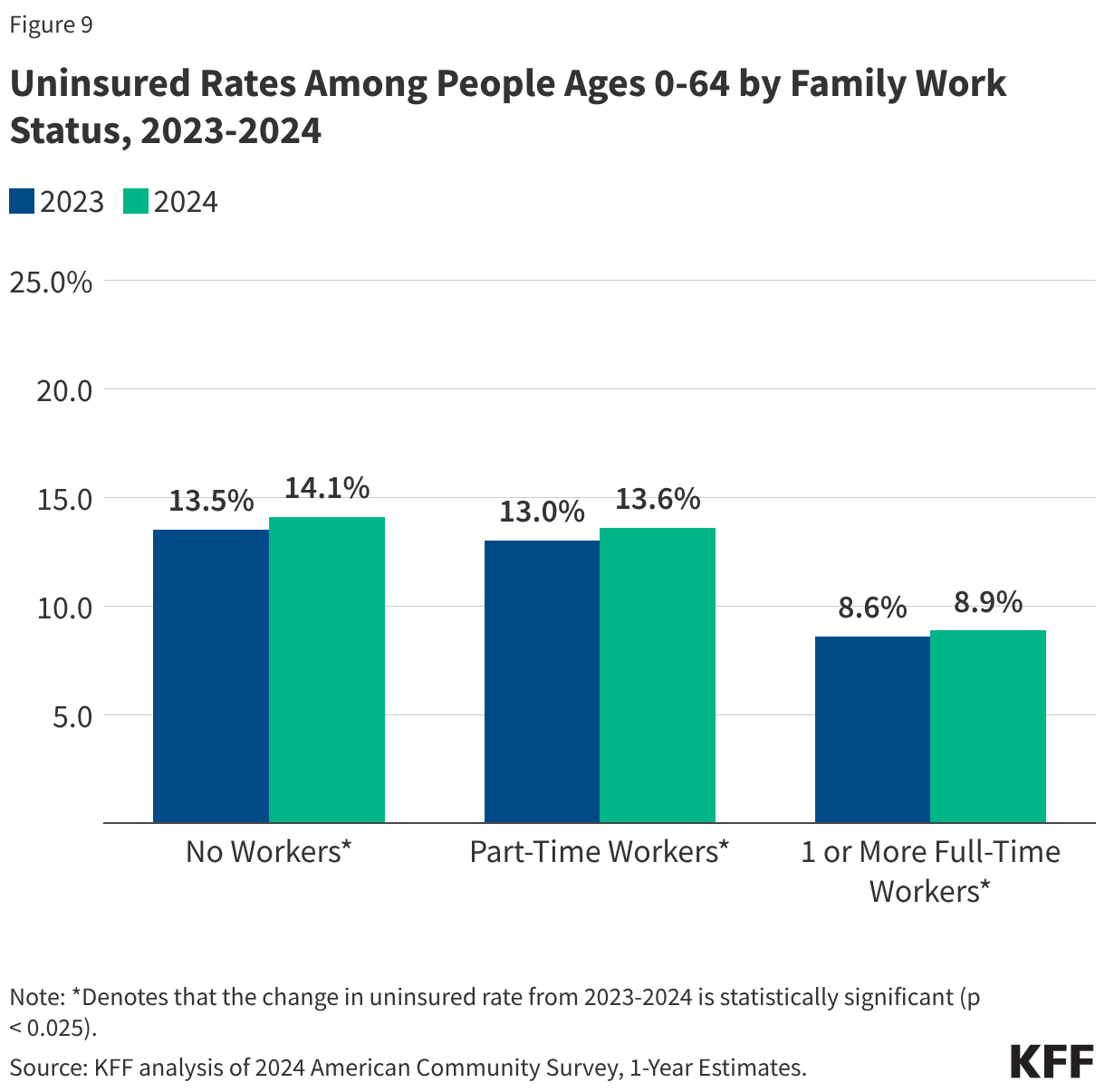

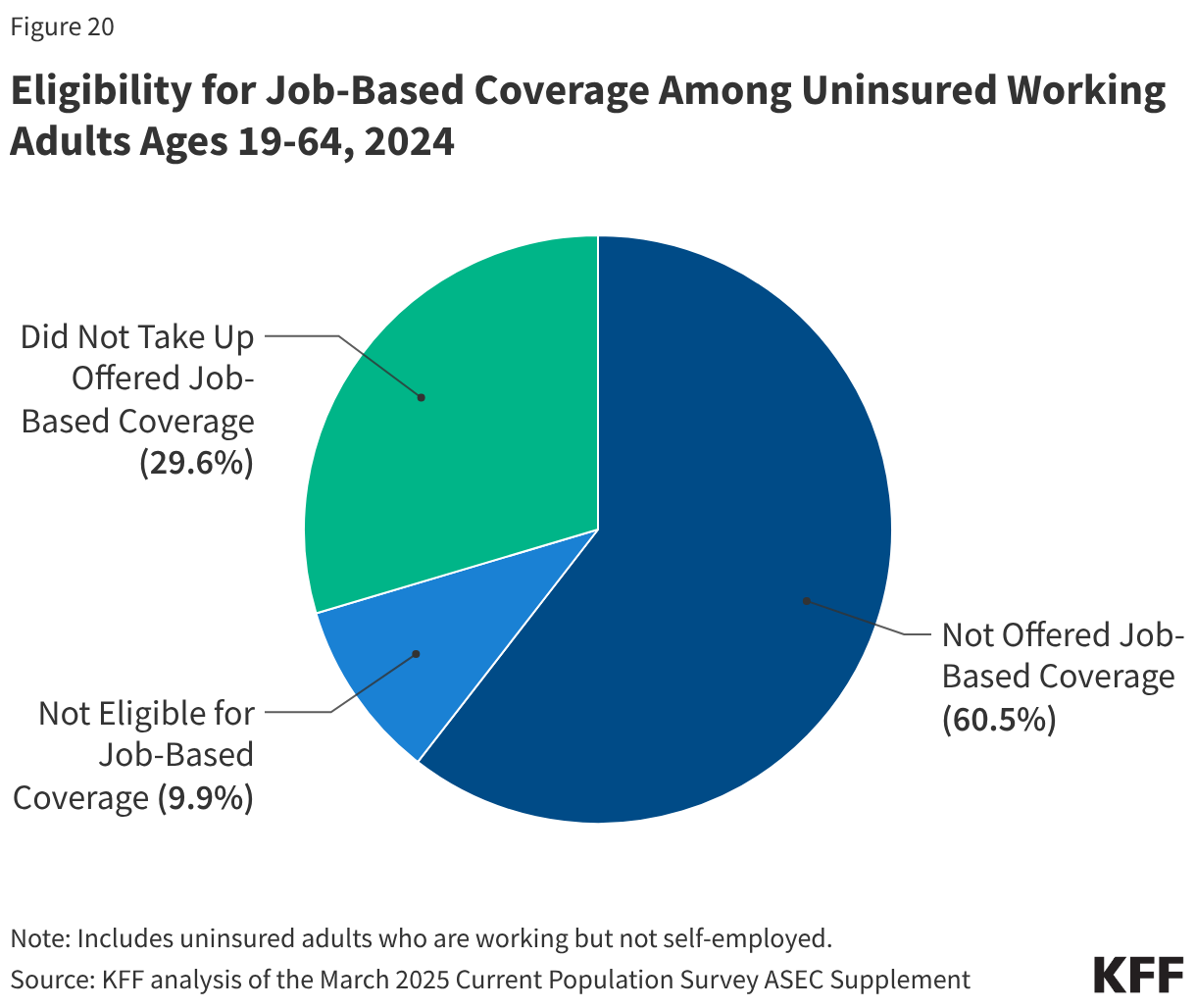

The demographic breakdown of the uninsured population in 2024 paints a picture of systemic inequality. Of the 26.7 million people without insurance, 80.1% belong to low-income families, and 85.1% reside in households with at least one worker. This underscores a persistent reality: employment does not guarantee access to affordable healthcare in the United States.

Disparities in Age and Geography

The impact of the coverage loss was not felt equally. Children, who historically have had higher rates of public coverage, saw a sharper increase in their uninsured rate—rising from 5.3% to 5.9%—compared to adults, whose rate moved from 11.1% to 11.3%.

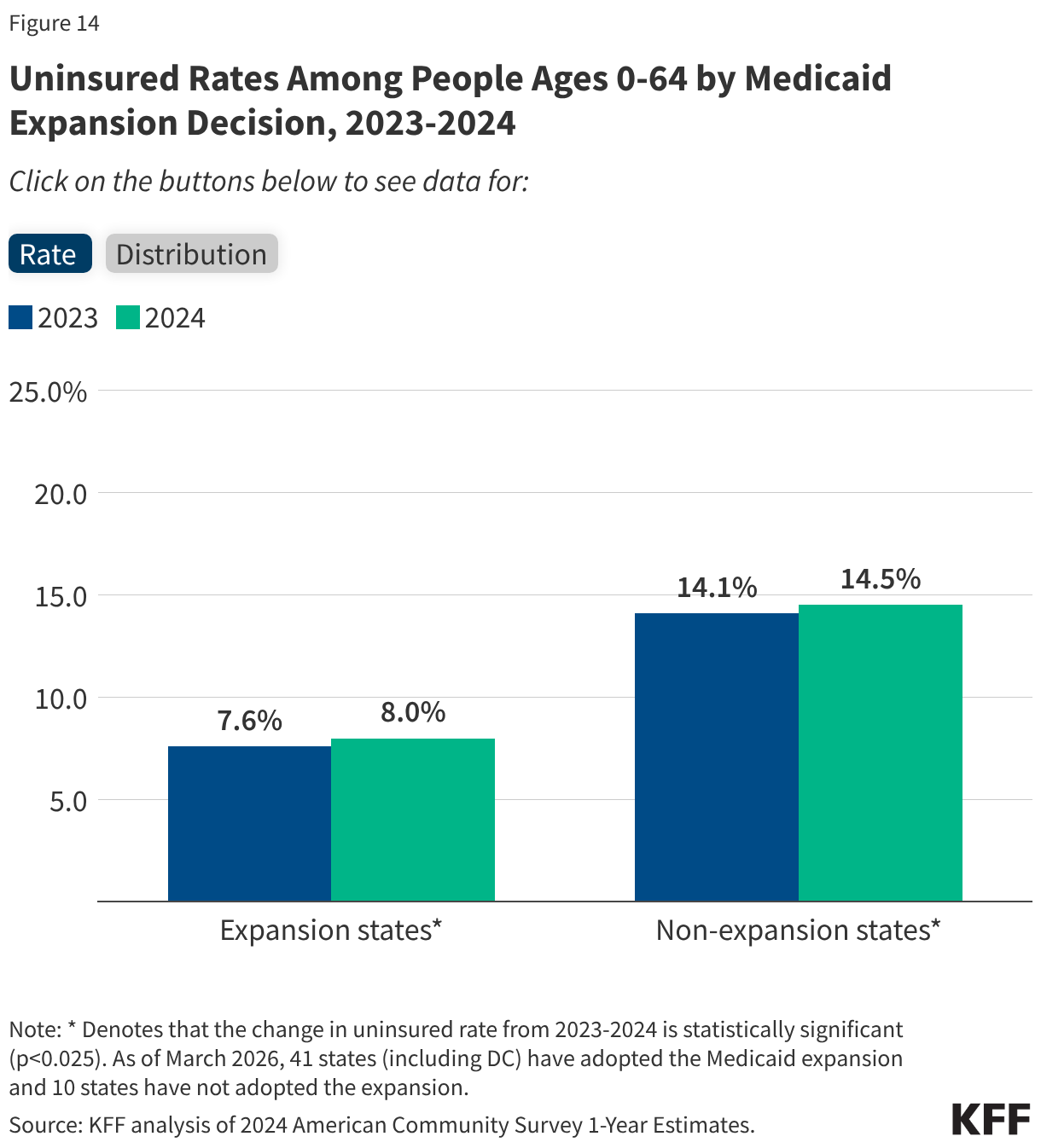

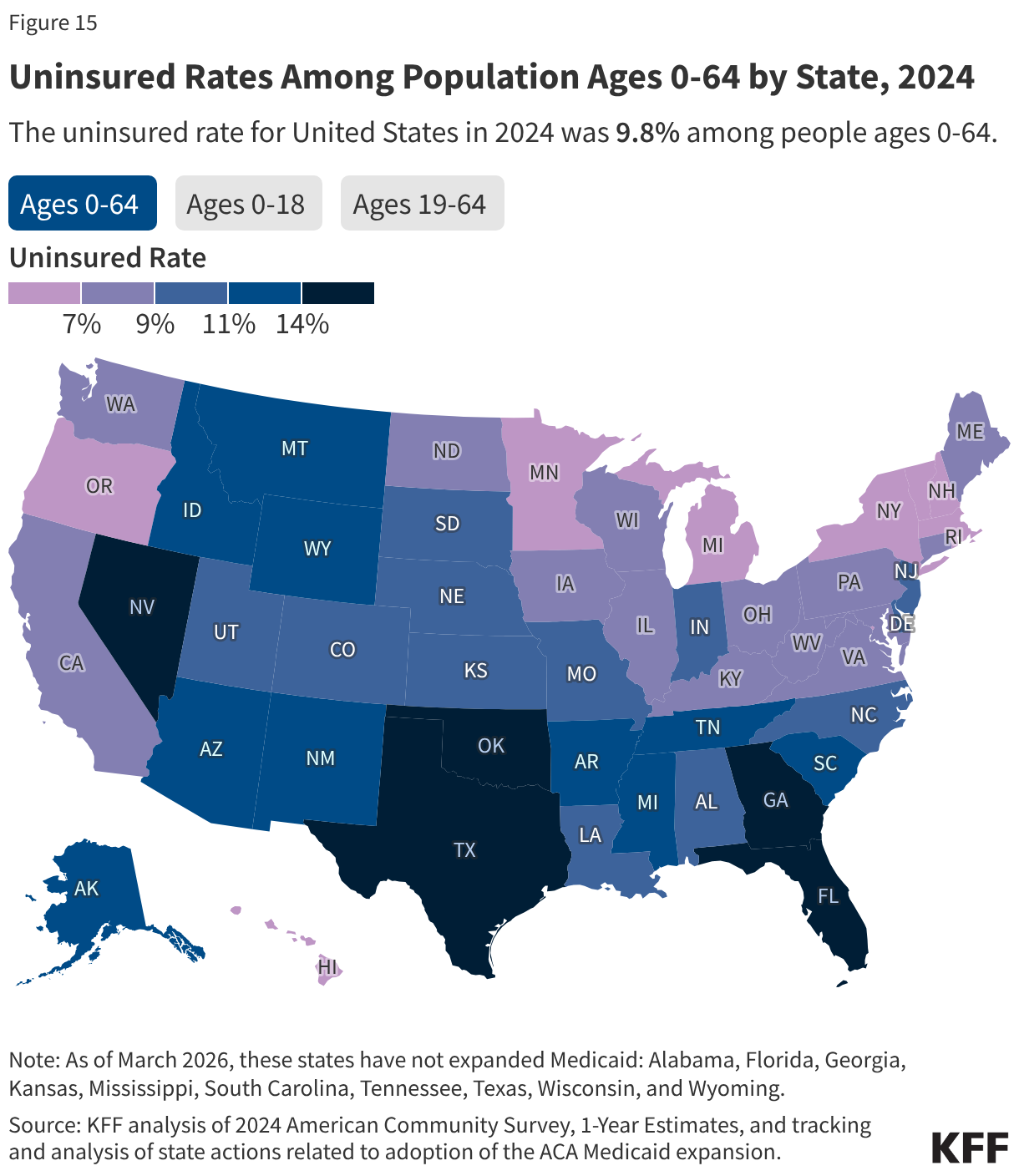

Geography remains the most significant predictor of insurance status. Nearly 42% of the uninsured population resides in the ten states that have refused to expand Medicaid under the ACA. In these states, the uninsured rate is 14.5%, nearly double the 8.0% rate found in states that chose to expand their programs. Texas, in particular, continues to lead the nation with an uninsured rate of 19.2%, reflecting the profound impact of state-level policy decisions on individual health outcomes.

The Role of Race and Citizenship

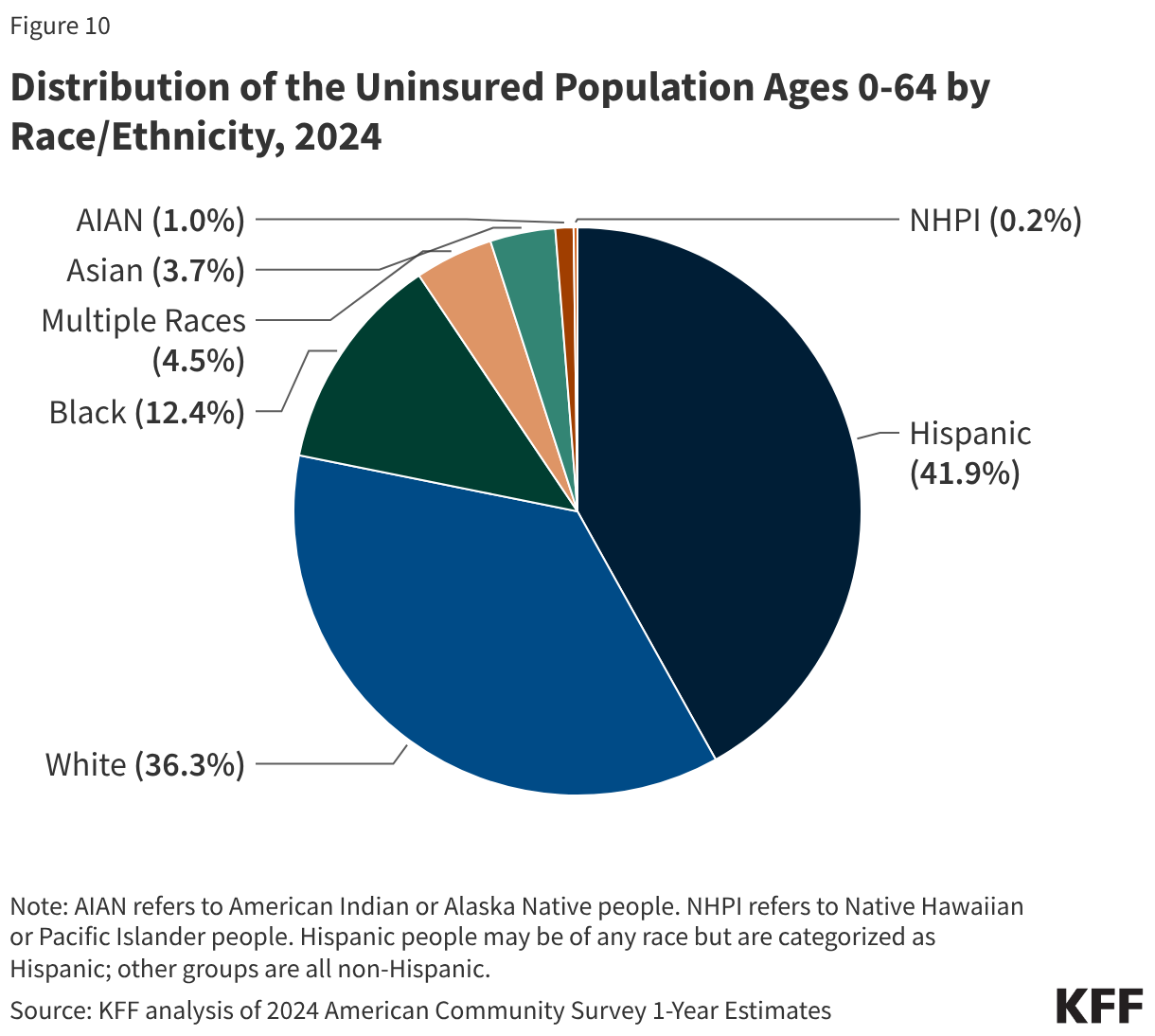

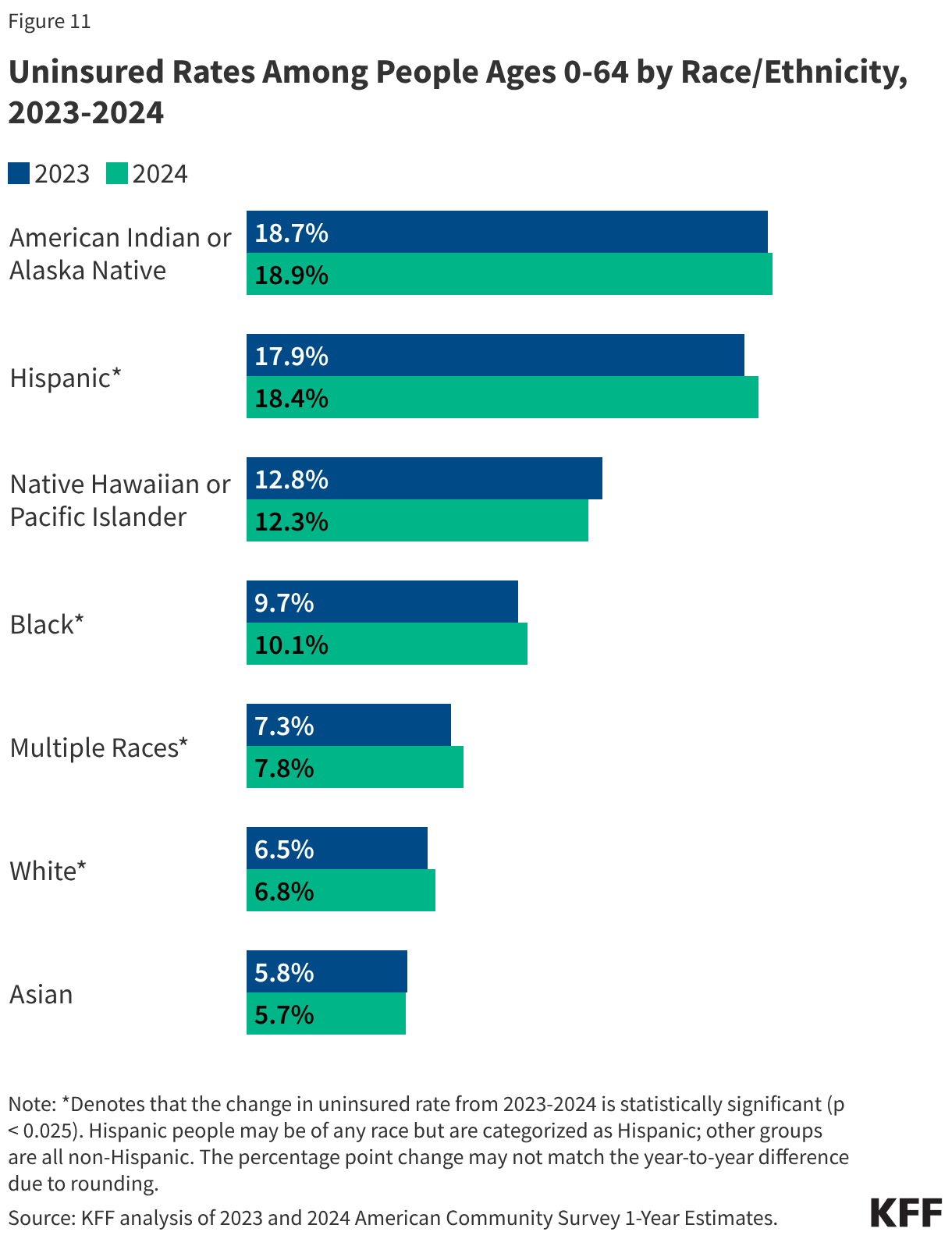

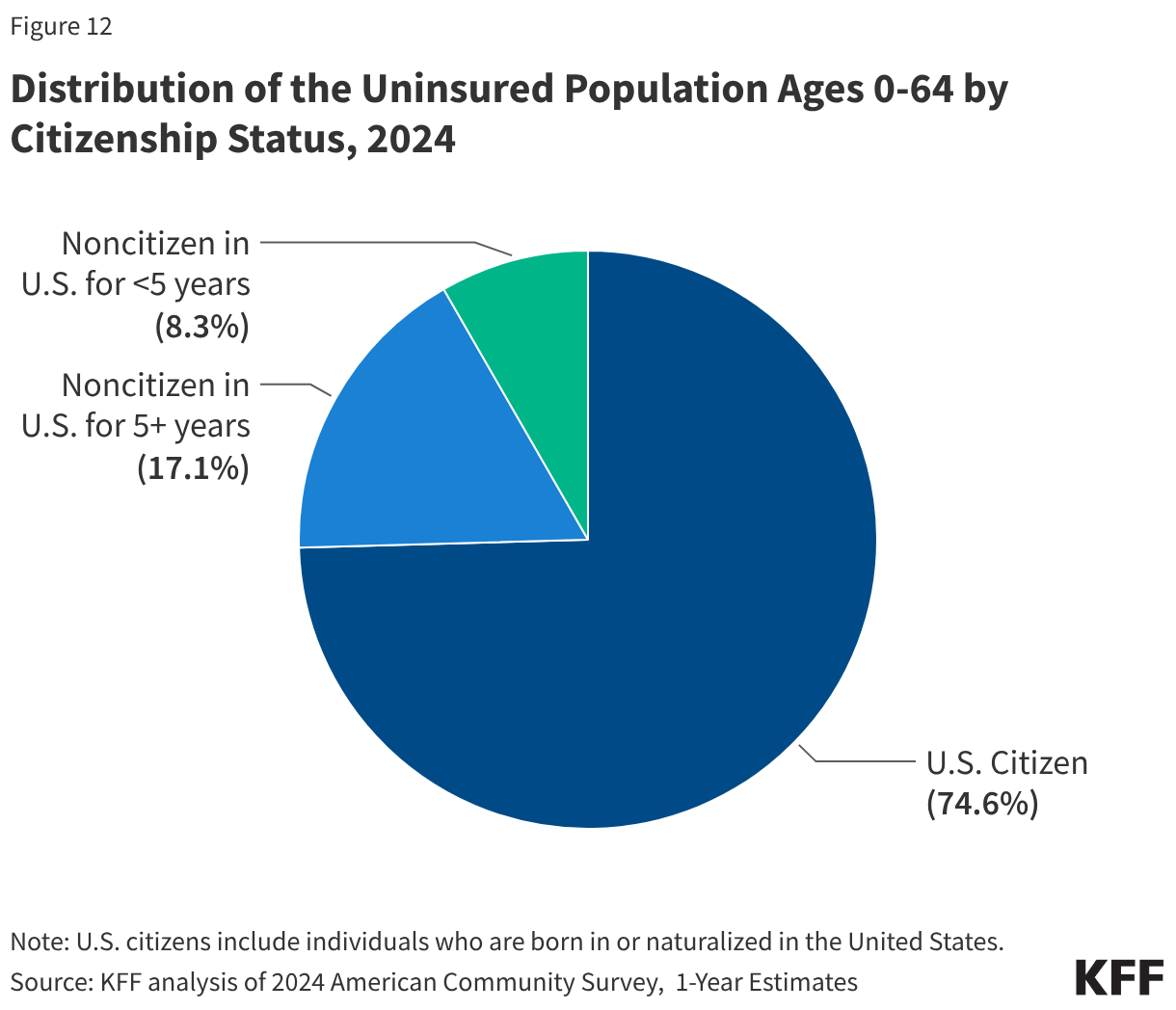

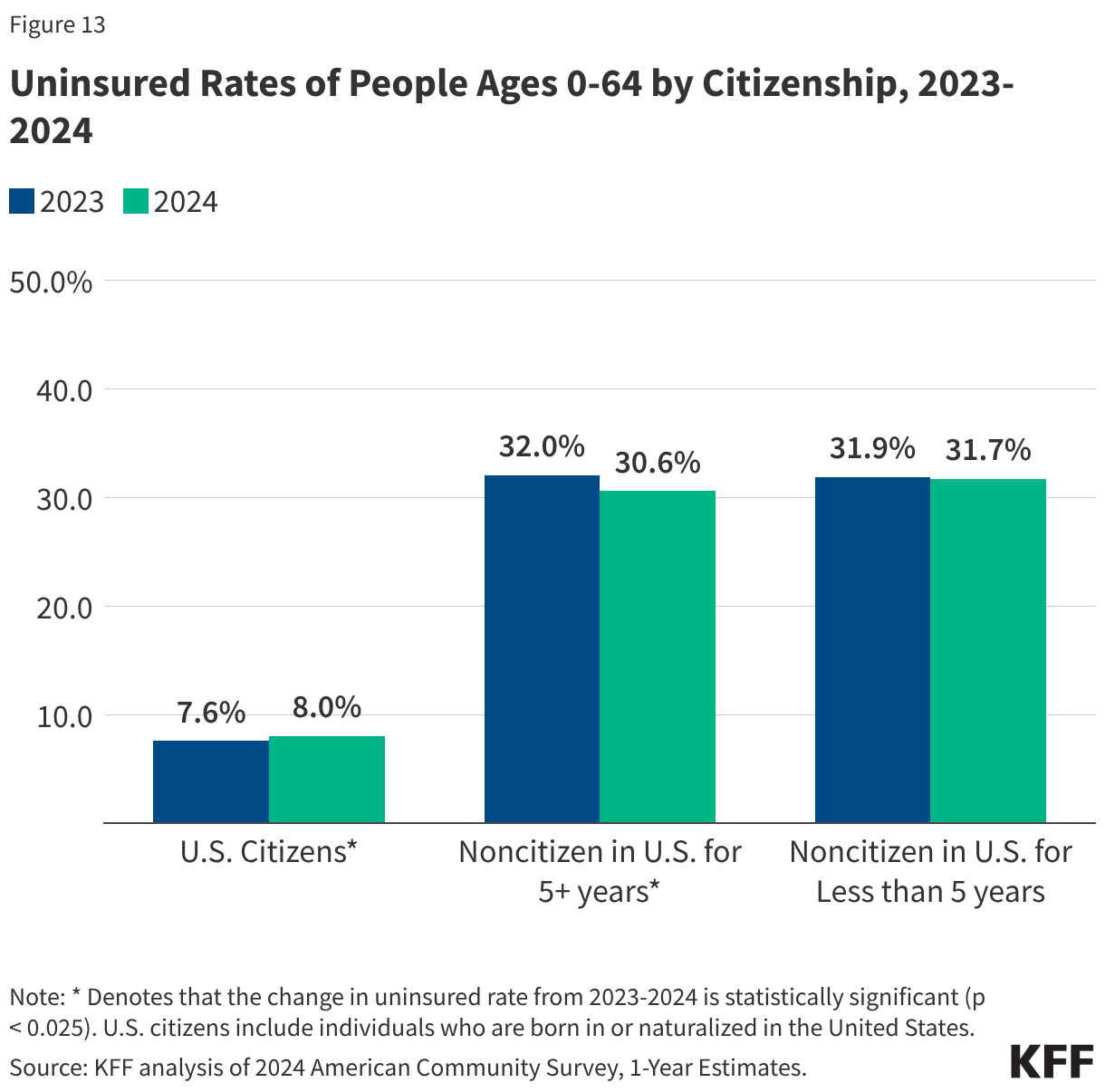

The burden of being uninsured falls disproportionately on people of color. Hispanic (18.4%) and American Indian/Alaska Native (18.9%) individuals are more than two and a half times more likely to be uninsured than White individuals (6.8%). Furthermore, while 74.6% of the uninsured are U.S. citizens, noncitizens face significantly higher barriers, with nearly one-third of noncitizen immigrants lacking coverage.

The Policy Outlook: A Tighter Squeeze Ahead

The Congressional Budget Office (CBO) has issued dire projections regarding the future of the uninsured rate. With the 2025 reconciliation law introducing stricter Medicaid eligibility requirements—including new work mandates and more frequent reporting—the administrative burden on states is expected to rise.

Furthermore, the expiration of enhanced Marketplace premium tax credits has rendered private plans significantly more expensive. The CBO estimates that by 2034, these combined factors could leave an additional 14 million people uninsured. Additionally, the current administration’s shift toward more aggressive immigration enforcement has created a "chilling effect." Even among immigrants who remain legally eligible for coverage, many are choosing to forgo enrollment out of fear that participation in public programs could impact their immigration status or lead to increased scrutiny.

Official Responses and Administrative Challenges

Policy analysts and public health advocates argue that the current trajectory is a result of a "fragmented and complex" system. While nearly 53% of the currently uninsured might be eligible for some form of subsidized coverage, the barriers to enrollment are significant.

"We are seeing a perfect storm," said one health policy researcher. "When you remove the guardrails of the pandemic era and simultaneously introduce stricter eligibility requirements, the inevitable result is a rise in the uninsured population."

The administration has defended its policies as necessary for fiscal responsibility and program integrity, emphasizing the need for regular eligibility audits. However, critics point out that these audits are often overly burdensome for low-income families, who may lose coverage due to minor clerical errors or the inability to navigate complex digital portals.

Implications: The High Cost of Being Uninsured

The human cost of this coverage loss is profound. Access to healthcare is not merely a matter of convenience; it is a determinant of life expectancy.

Barriers to Care

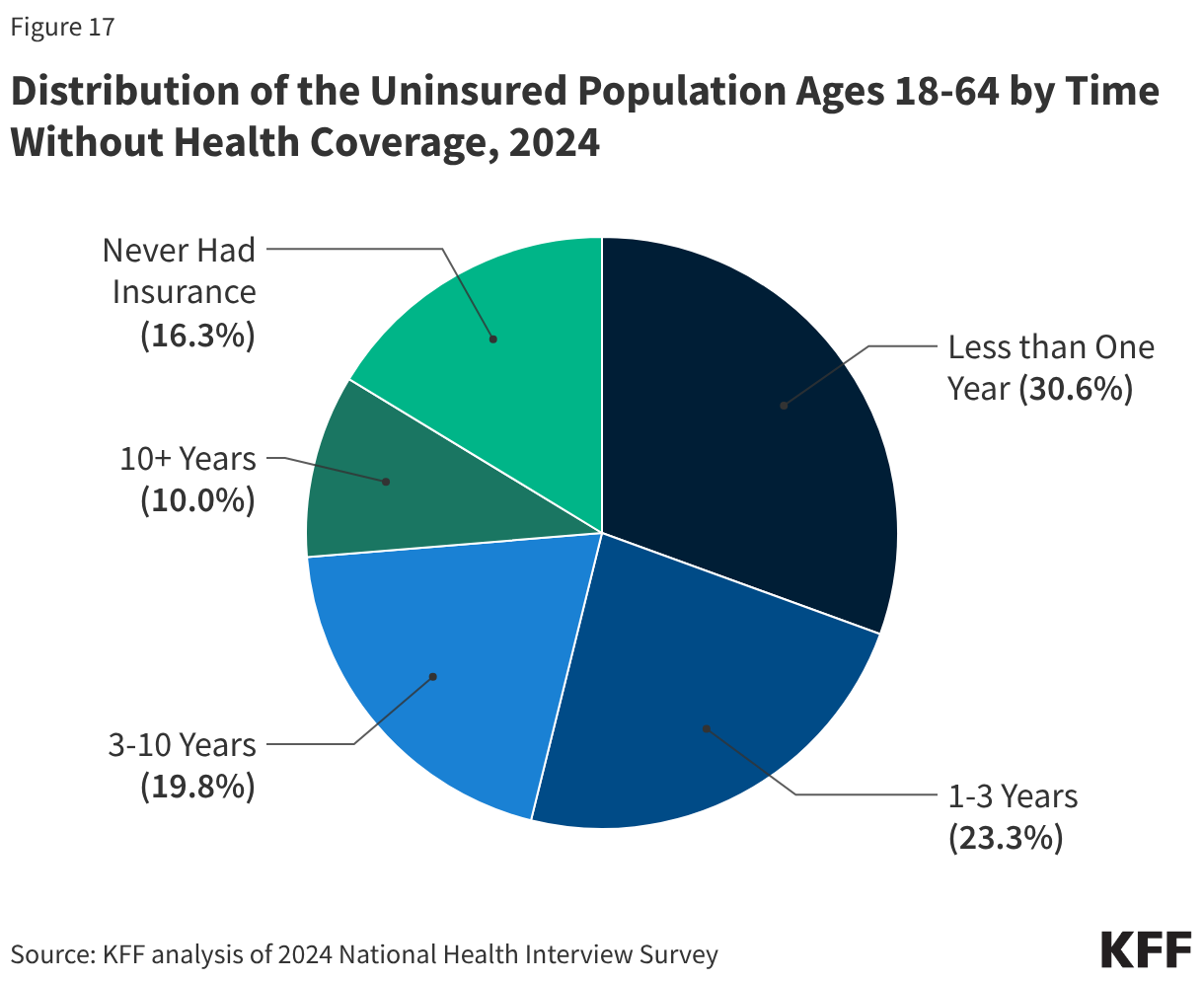

Uninsured adults are significantly less likely to have a "usual source of care." In 2024, 46.2% of uninsured adults reported having no regular doctor or clinic. When medical issues arise, the lack of insurance forces a "wait-and-see" approach that often leads to higher acuity when the patient finally seeks help. Among those with chronic conditions, such as diabetes or hypertension, uninsured individuals are three to four times more likely to forgo essential medications or diagnostic tests due to cost.

Financial Ruin

The financial implications are equally severe. Uninsured individuals are nearly twice as likely to struggle with medical debt as their insured counterparts. Nearly 60% of uninsured adults report that they or a household member have had trouble paying for healthcare, leading to a cascade of financial distress. From relying on payday loans to overdrawing checking accounts, the uninsured are often forced to choose between essential living expenses—like rent and food—and medical bills.

Medical debt is not just an inconvenience; it is a barrier to future financial stability. Over 60% of uninsured adults report holding medical debt, which often results in drained savings and damaged credit, creating a cycle of poverty that is increasingly difficult to escape.

The Impact on Providers

The safety net—comprising public hospitals and community health centers—is also feeling the strain. As the number of uninsured patients grows, the volume of uncompensated care rises, putting immense pressure on facilities already operating with limited margins. In states that have not expanded Medicaid, these institutions are particularly vulnerable. Research consistently shows that Medicaid expansion reduces uncompensated care costs, providing a more stable financial foundation for rural and urban hospitals alike.

Conclusion: A System at a Crossroads

The 2024 data serves as a stark reminder of the fragility of health security in the United States. While the Affordable Care Act provided a framework for coverage expansion, the reliance on state-level implementation and the volatility of federal policy means that access to care remains tenuous for millions.

As the nation looks toward 2026 and beyond, the trend of rising uninsured rates threatens to reverse decades of progress in reducing health disparities. Without meaningful intervention—whether through the universal adoption of Medicaid expansion, the stabilization of premium subsidies, or the simplification of enrollment processes—the chasm between the insured and the uninsured is poised to widen. For the 26.7 million currently without coverage, the cost of this policy environment is measured in missed diagnoses, delayed treatments, and the heavy, lingering burden of medical debt. The path forward remains uncertain, but the data is clear: the current trajectory is one that leaves too many Americans behind.