For millions of older Americans and individuals with disabilities, selecting health coverage is a foundational decision that dictates both their access to care and their financial security. The choice primarily pits traditional Medicare against private Medicare Advantage (MA) plans. While both offer essential coverage, they diverge sharply on a critical consumer protection: the out-of-pocket (OOP) limit.

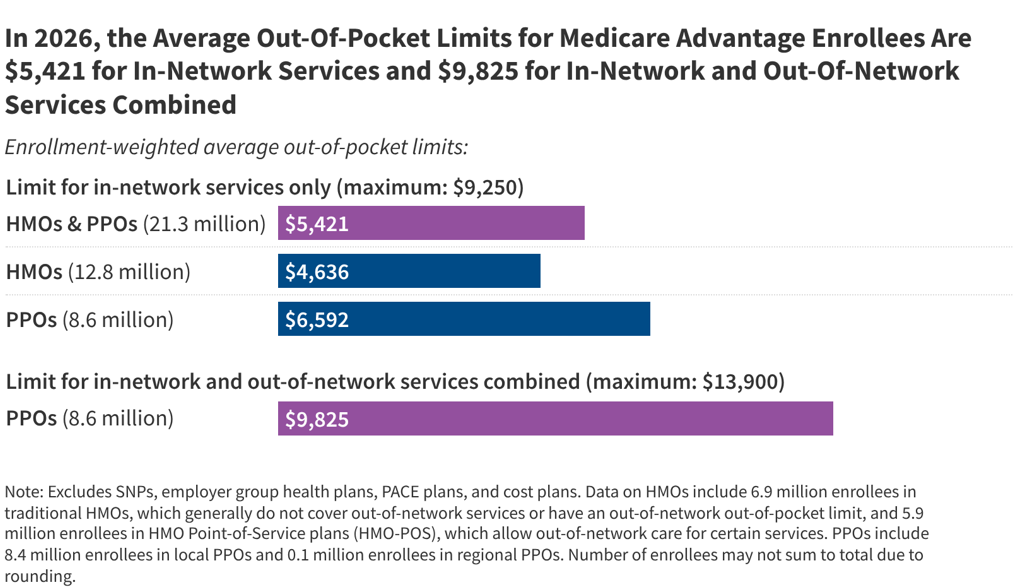

As we look toward 2026, the structure of Medicare Advantage plans reveals a complex landscape of risk and protection. With 21.3 million beneficiaries enrolled in individual Medicare Advantage plans, understanding these financial caps is more important than ever.

Main Facts: The Anatomy of 2026 Coverage

The most significant distinction between traditional Medicare and Medicare Advantage is the presence of an annual "catastrophic cap." In 2026, private Medicare Advantage plans are permitted to set an out-of-pocket maximum—a safety net that ensures beneficiaries are not held responsible for unlimited medical costs after a certain point.

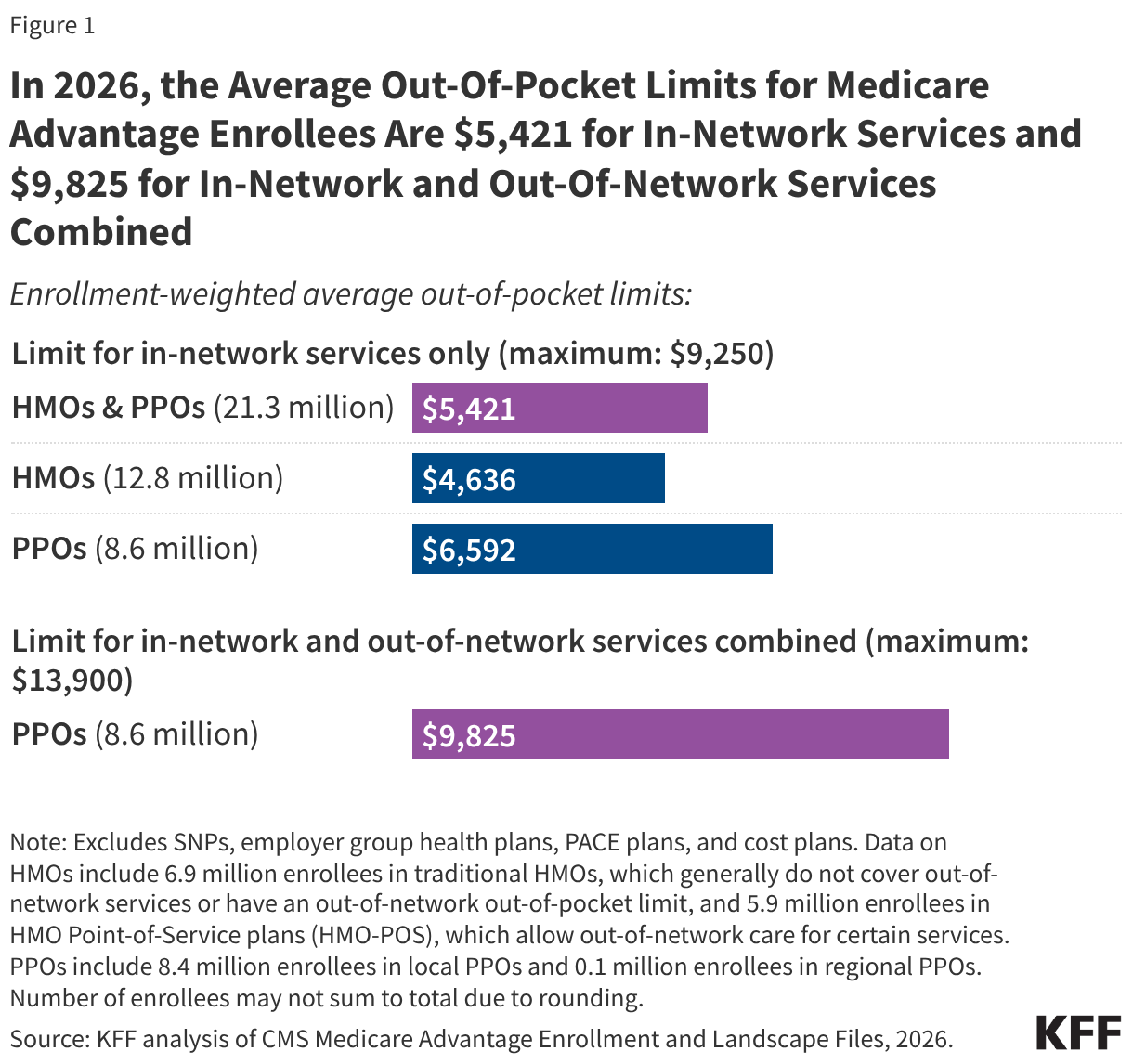

For the 2026 plan year, federal regulations dictate that Medicare Advantage plans cannot exceed an OOP limit of $9,250 for in-network services and $13,900 for a combination of in-network and out-of-network services. While these figures represent the absolute federal ceiling, many plans choose to set lower limits, effectively competing for enrollees by offering greater financial protection.

The reality, however, is not uniform. The average enrollment-weighted out-of-pocket limit for MA enrollees in 2026 stands at $5,421 for in-network services and $9,825 for combined services. These averages demonstrate that while the federal government sets the "worst-case scenario" cap, the market forces within the private insurance sector often push these limits lower.

Chronology: The Evolution of Financial Protections

The conversation surrounding OOP caps in Medicare is not new; it is a decades-long policy struggle.

1988: The Failed Attempt

In 1988, Congress enacted a Medicare Catastrophic Coverage Act, which sought to introduce an out-of-pocket cap for traditional Medicare. It was a landmark piece of legislation intended to protect seniors from bankruptcy due to health crises. However, the law was repealed only one year later. The primary driver of this repeal was not a lack of consensus on the need for protection, but rather a fierce debate over the financing mechanisms used to pay for the benefit.

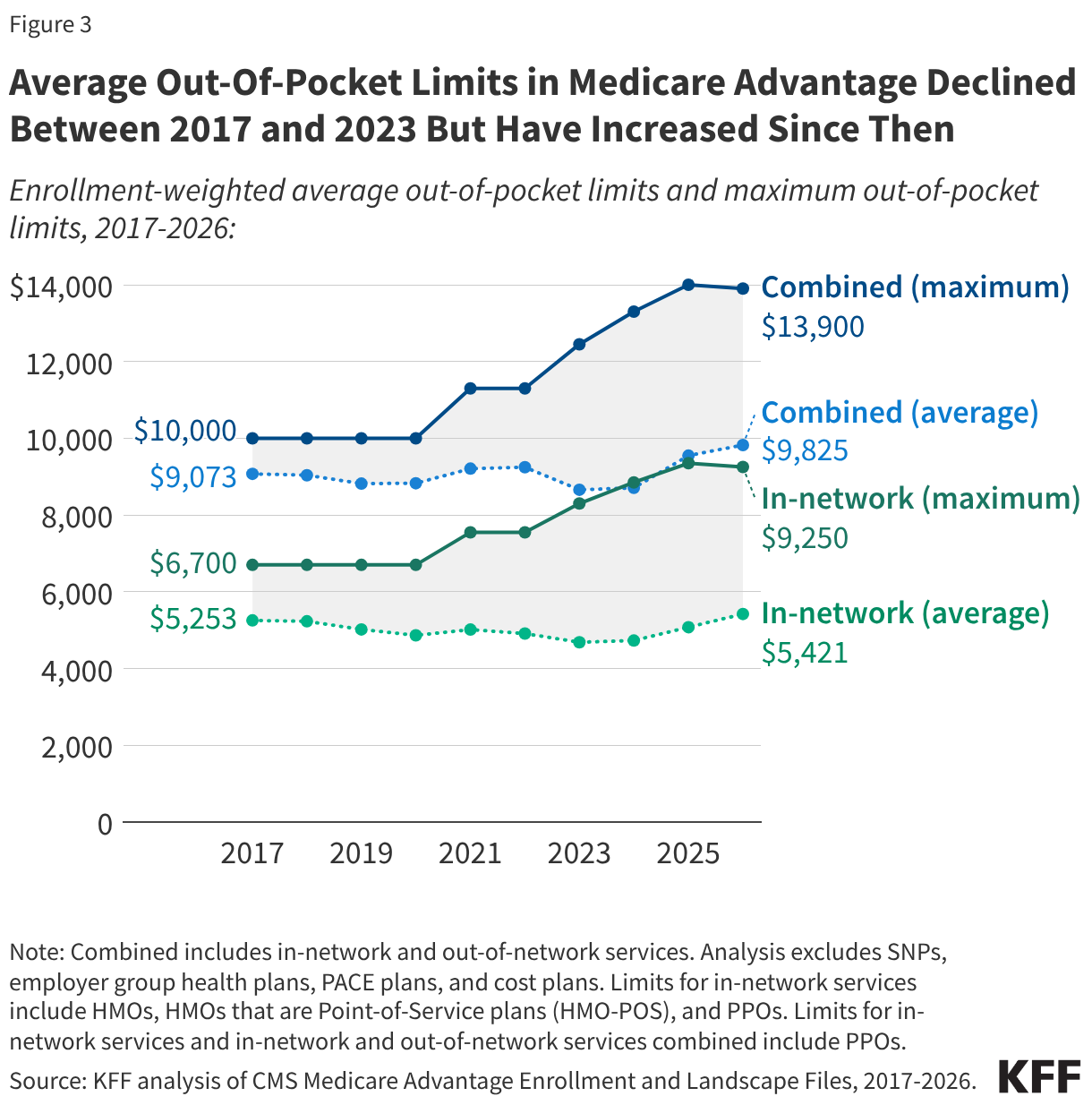

2017–2023: A Period of Declining Limits

For several years, the trend in Medicare Advantage was one of improved protection. From 2017 to 2023, the average in-network OOP limit dropped from $5,253 to $4,685. This downward trend suggested that as the MA market matured and competition intensified, insurers were using their federal "rebate" dollars—payments made by the government to the plans—to lower the financial burden on beneficiaries.

2024–2026: The Recent Inversion

The trend of declining limits hit a plateau and reversed starting in 2024. By 2026, the average in-network limit climbed back to $5,421. While the maximum allowable cap decreased slightly between 2025 and 2026, the average limit experienced by beneficiaries has risen, indicating that plans are reallocating their resources—perhaps shifting funds toward other supplemental benefits or simply adjusting to higher inflation in medical services.

Supporting Data: Understanding the Landscape

The data reveals a stark divide based on plan types and geographic location.

HMOs vs. PPOs

Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs) dominate the MA market. In 2026, the 12.8 million enrollees in HMOs benefit from an average in-network OOP limit of $4,636. Conversely, the 8.6 million PPO enrollees face an average in-network limit of $6,592.

The rationale behind this difference is functional: HMOs typically restrict enrollees to a closed network of providers, allowing the plan to manage costs more effectively and pass some of those savings back to the beneficiary in the form of lower caps. PPOs offer greater flexibility by covering out-of-network care, but that freedom comes with a higher "price" in the form of elevated OOP limits.

The "One-in-Five" Reality

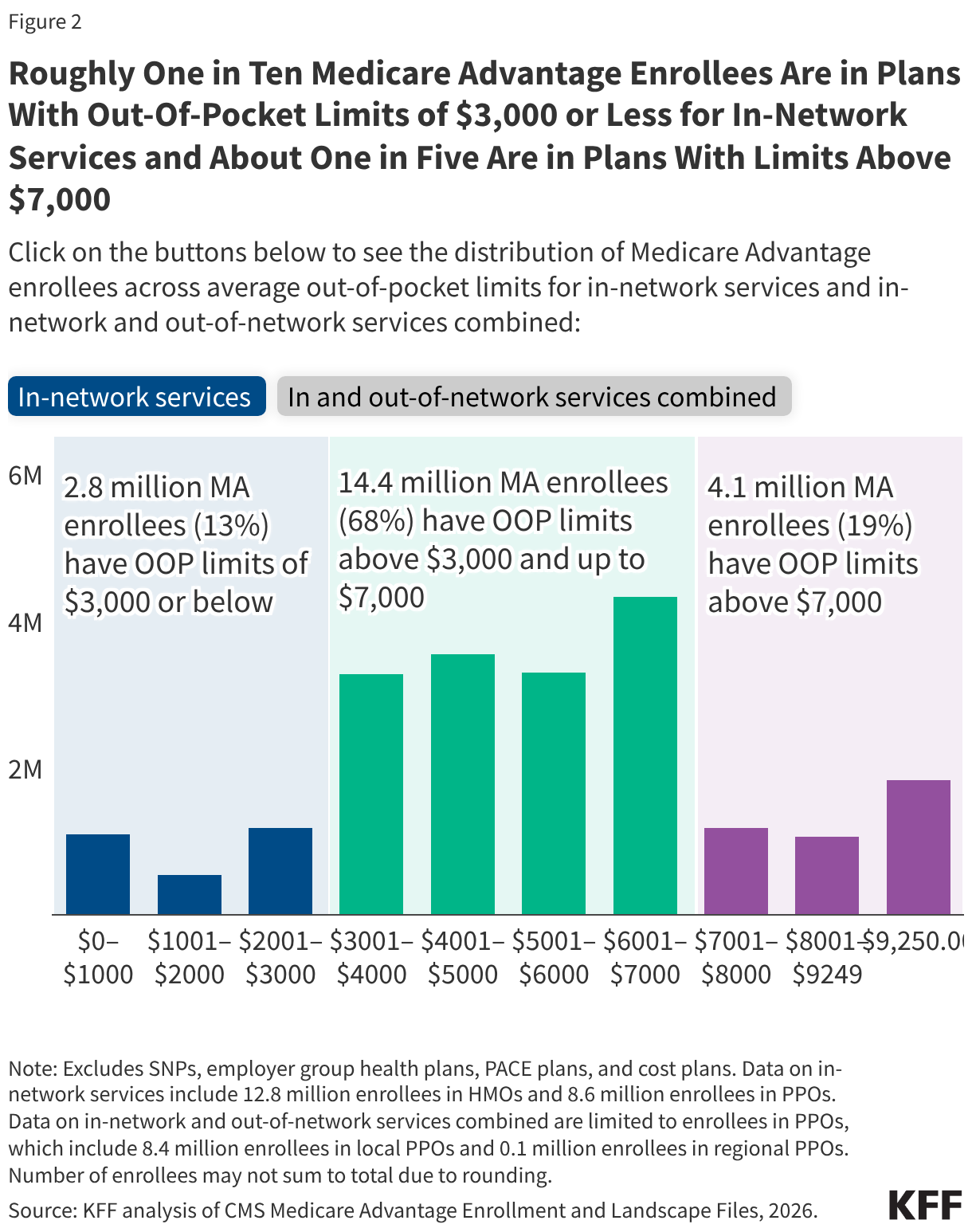

Approximately 19% of MA enrollees (4.1 million people) are currently in plans with in-network OOP limits exceeding $7,000. Among these, 1.8 million are in plans hitting the absolute maximum limit of $9,250. It is important to note that these figures represent the potential liability for a beneficiary. Because individual health spending data is not publicly available for these specific cohorts, we cannot determine exactly how many enrollees reach these caps annually. However, the presence of such high limits underscores the financial risk inherent in these plans.

The Rural-Urban Divide

Geography also plays a role. Medicare Advantage enrollees in rural areas face average out-of-pocket caps about $800 higher than their urban counterparts ($6,078 vs. $5,291). This disparity is largely driven by the higher concentration of PPO-style plans in rural areas, which are often the only private options available in sparsely populated regions.

Official Responses and Policy Perspectives

The Medicare Payment Advisory Commission (MedPAC) has been a vocal proponent for reform. MedPAC has consistently recommended that traditional Medicare be updated to include an out-of-pocket cap. Their vision is not merely to add a cap, but to engage in a broader redesign of the program, including the merging of Part A and Part B deductibles to simplify the labyrinthine cost-sharing structure that currently leaves traditional Medicare beneficiaries vulnerable to high costs.

Currently, traditional Medicare remains the only major form of health insurance in the United States without an out-of-pocket cap. While most traditional Medicare beneficiaries have supplemental coverage—such as Medicaid, retiree coverage, or private Medigap policies—these are not universal solutions. Medigap, for instance, requires additional monthly premiums, which can be prohibitive for low-income seniors.

Implications: What This Means for Beneficiaries

The 2026 data presents a dual-edged sword for the American public.

The Advantage of Predictability

For those in Medicare Advantage, the primary benefit remains the predictability of health costs. Knowing that there is a defined "finish line" for medical expenses provides a level of psychological and financial security that is absent in traditional Medicare. For a retiree on a fixed income, the difference between an uncapped financial liability and a $5,000 or $7,000 cap can be the difference between financial independence and medical debt.

The Trade-Offs

However, the data also highlights the "hidden" costs of these caps. When beneficiaries choose a plan with a lower OOP limit, they may be accepting smaller provider networks (HMOs) or higher premiums for other services. Furthermore, the reliance on "rebate dollars" to lower these caps means that the benefit is subject to the strategic priorities of the insurance company. If a plan decides that its competitive edge is better served by offering dental, vision, or hearing benefits, the OOP limit for medical services might be raised accordingly.

The Call for Systemic Reform

The ongoing analysis by groups like KFF and the recommendations from MedPAC signal a growing consensus among policy experts: the status quo for traditional Medicare is increasingly viewed as outdated. As medical costs continue to rise, the risk of a "catastrophic event" becomes more probable for the average senior.

The lack of an OOP cap in traditional Medicare forces many to choose between the flexibility of the traditional system and the financial protection of Medicare Advantage. For those who prioritize access to any doctor or specialist in the country, the lack of a cap is a high-stakes gamble. For those who prioritize financial certainty, Medicare Advantage offers a structured, albeit sometimes restrictive, alternative.

As the 2026 plan year begins, beneficiaries are encouraged to look beyond the marketing materials. An attractive "zero-premium" plan may come with high out-of-pocket limits that could prove devastating in the event of a chronic illness or a major surgery. Understanding the specific limit of one’s chosen plan is the single most important step a beneficiary can take to ensure their health coverage remains a shield rather than a source of financial stress.

In conclusion, while the Medicare Advantage market provides a vital safeguard against unlimited spending, the variations in these limits—by plan type, geography, and year-over-year adjustments—require a high degree of consumer vigilance. The debate over whether to bring similar protections to traditional Medicare remains one of the most critical, yet unresolved, issues in American healthcare policy. Until such a change occurs, the burden of managing financial risk will continue to rest heavily on the shoulders of the individual.