The biotechnology sector has entered the second half of 2026 riding a wave of unprecedented financial momentum. Despite a volatile regulatory environment and lingering anxieties regarding geopolitical tensions, venture capital funding for private drug startups has continued a robust, multi-year surge. New data from BioPharma Dive reveals that the first six months of 2026 have been a banner period for the industry, marked by aggressive dealmaking, massive capital infusions, and a resilient public market performance that has reignited investor appetite.

The State of the Sector: By the Numbers

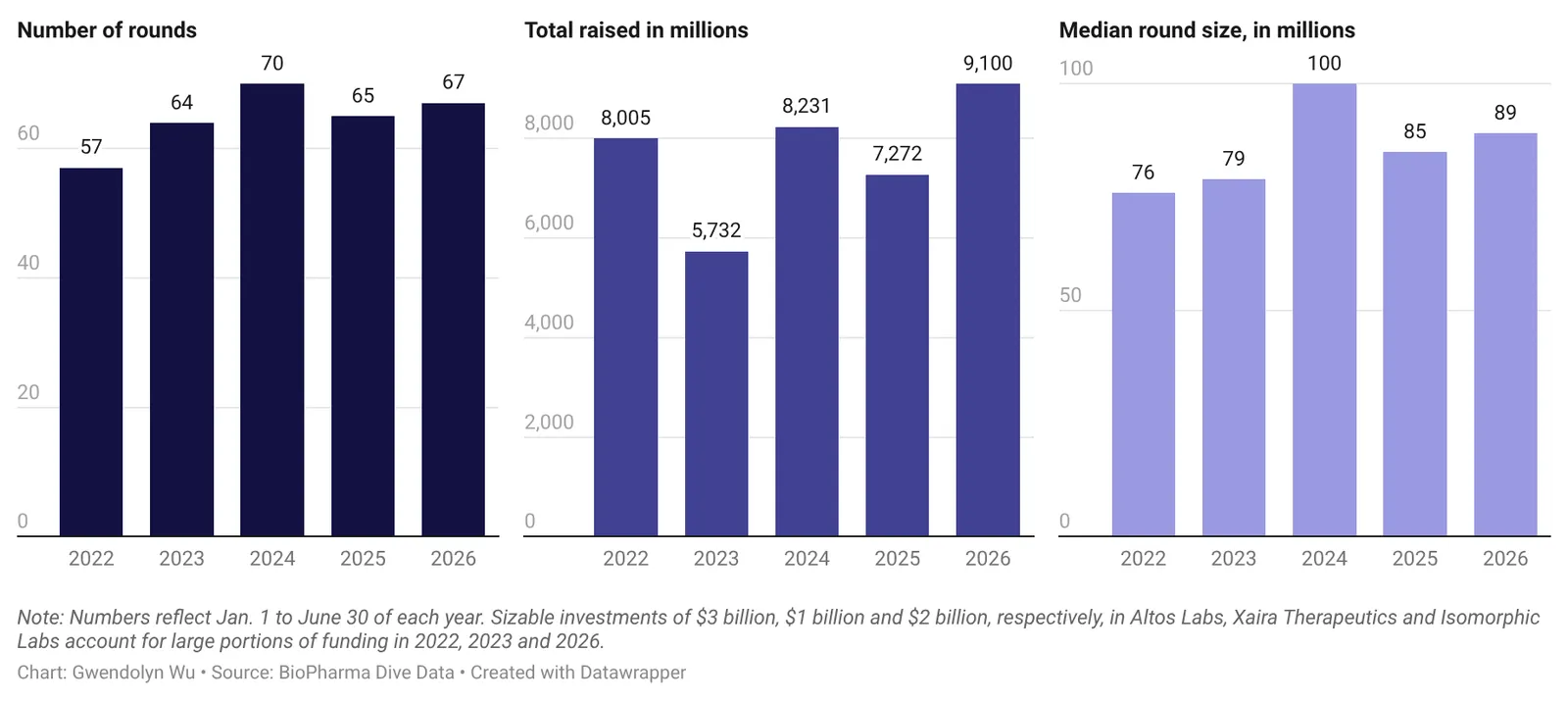

Between January and June 2026, at least 68 biotechnology companies successfully secured more than $9.1 billion in venture capital funding. This figure represents the highest first-half total since the industry’s pandemic-era peak in early 2022.

The composition of this funding is characterized by a distinct shift toward "megarounds"—capital infusions of $100 million or more. According to the tracking data, these large-scale financings accounted for approximately 76% of all funds raised during the first half of the year. This trend suggests that while liquidity is available, investors are increasingly concentrating their capital in companies with proven platforms or late-stage assets rather than spreading their risk across a wider net of early-stage startups.

A Chronology of Momentum: From IPOs to Acquisitions

The resurgence of venture funding did not occur in a vacuum; it was bolstered by a remarkably active IPO market and a record-breaking pace for mergers and acquisitions (M&A).

- Q1 2026 – The IPO Rebound: The year began with a significant thaw in the public markets. Thirteen firms launched initial public offerings, generating a combined $4.5 billion in proceeds. Notably, the median IPO haul reached nearly $302 million, a figure substantially higher than in previous years. High-profile debuts, such as those from Parabilis Medicines and Kailera Therapeutics, shattered sector records, signaling that public market investors are once again willing to place significant bets on the biotech narrative.

- Q2 2026 – The M&A Surge: As the IPO market stabilized, M&A activity accelerated. By mid-year, 38 acquisition deals had been finalized, positioning the sector on track for its most aggressive acquisition pace in at least seven years. The scale of these deals is particularly noteworthy: nearly two-thirds of the transactions were valued at $1 billion or more, with four deals exceeding the $10 billion threshold.

This M&A activity has served as a vital exit mechanism for venture firms, providing the liquidity necessary to recycle capital back into new, privately held drug startups.

Expert Perspectives: Voting Booths and Weighing Scales

The prevailing sentiment among industry leaders is one of cautious optimism. Simeon George, CEO and managing partner of the venture firm SR One, noted in a May interview that the recent months have been highly reaffirming for the M&A landscape. Addressing the nuance of the IPO market, George invoked Benjamin Graham’s famous investment adage: "In the short term, the markets are a voting booth, and in the long term, they’re weighing scales."

This perspective highlights the current market philosophy: while short-term volatility and regulatory noise might cause erratic pricing, the underlying value of innovative science remains the primary driver of long-term capital allocation.

The "Innovation Gap": Concerns for the Future

Despite the multi-billion-dollar inflows, the internal health of the biotech ecosystem is showing signs of structural strain. Ben Zercher, a senior analyst at Pitchbook, points out that the impressive top-line funding numbers are partially skewed by massive outliers. For instance, the $2.1 billion funding round for AI-driven drug discovery firm Isomorphic Labs accounts for a significant portion of the first-half total.

More concerning to industry observers is the growing scarcity of seed-stage funding. Ashwin Singhania, a principal at Ernst & Young’s life sciences practice, emphasizes that the era of easy money for first-time founders or high-risk "seed" ventures has largely passed.

"I think that a grave concern to the biotech community is where that next wave of early innovation is going to come from," Singhania stated. He highlighted the "backdrop" of recent funding cuts at the National Institutes of Health (NIH), which threaten to stifle basic research. If the academic pipeline for early-stage discovery is weakened, the industry may face a "talent and innovation drought" as far as a decade into the future.

Currently, capital is being diverted away from nascent ideas and toward "de-risked" assets. Data shows that two-thirds of all venture rounds in the first half of 2026 went to companies that already had a drug candidate in human clinical trials.

Regulatory Headwinds and Geopolitical Tensions

The industry’s current success is being tested by two primary external pressures: U.S.-China relations and instability within the Food and Drug Administration (FDA).

The China Factor

The threat of a U.S. government crackdown on investments in Chinese drug assets has created a complex environment for venture capitalists. Several newly formed companies, such as cAMPfield Therapeutics and Solstice Oncology, have based their platforms on ready-made drug candidates originating from Chinese research pipelines. While these deals have attracted significant capital, they have also invited scrutiny regarding national security and the long-term competitiveness of U.S. firms.

The FDA Instability

Regulatory uncertainty at the FDA has created what analysts describe as a "perfect storm." Frequent leadership turnover and changing guidelines have made investors hesitant to back companies in certain high-risk categories, particularly those focusing on complex modalities like cell and gene therapy.

According to Pitchbook’s Zercher, the lackluster market performance of therapies such as Casgevy, combined with documented side effects in clinical trials, has forced investors to adopt a "wait-and-see" approach. Consequently, funding for cell and gene therapy developers has stalled, remaining in a multi-year slump with only about $2 billion in total funding anticipated for the year.

Strategic Allocation: Where the Money Goes

In this environment of heightened scrutiny, investors are gravitating toward "safer" therapeutic areas. Immune and cancer-focused drugmakers commanded more than 40% of all funding rounds in the first half of 2026.

Furthermore, the preference for traditional modalities is clear: developers of biologics and small molecules each secured over $2 billion in funding, significantly outpacing the more experimental nucleic acid and gene-editing sectors.

Doreen Levine, a partner at Ernst & Young’s Americas life sciences sector accounting group, summarizes the current climate succinctly: "For the right management team, with the right platform or asset, there could be an appetite. The VCs have the liquidity and interest to do it, it’s just that they’re being very judicious."

Implications: A New Era of Professionalism

The current biotech boom of 2026 is fundamentally different from the speculative bubbles of the past. It is an era defined by professionalized, data-driven investing.

The implications of these trends are twofold:

- For Founders: The barrier to entry has risen significantly. Startups can no longer rely on early-stage "venture building" based on unproven concepts. They must now demonstrate clinical progress, strong intellectual property, and a clear path toward either a high-value IPO or an M&A exit with a major pharmaceutical partner.

- For the Industry: The focus on late-stage assets and proven platforms will likely lead to a higher success rate for new drug approvals. However, the long-term cost may be a narrowing of the scientific "aperture." By prioritizing companies with human clinical data, the sector risks overlooking the next generation of truly disruptive, breakthrough science that requires longer gestation periods.

As the industry moves into the second half of 2026, all eyes will be on whether the current pace of M&A remains sustainable and if the venture community will eventually find a way to re-risk the early-stage innovation pipeline. For now, the biotech sector remains a testament to the resilience of human ingenuity, albeit one that is currently playing a very calculated game of high-stakes chess.