The Affordable Care Act (ACA) introduced a foundational mechanism designed to hold health insurance companies accountable for their spending: the Medical Loss Ratio (MLR) provision. This regulation serves as a fiscal "check and balance," requiring insurers to devote the vast majority of their premium income to direct patient care and quality improvement rather than administrative bloat, marketing campaigns, or excessive profit margins.

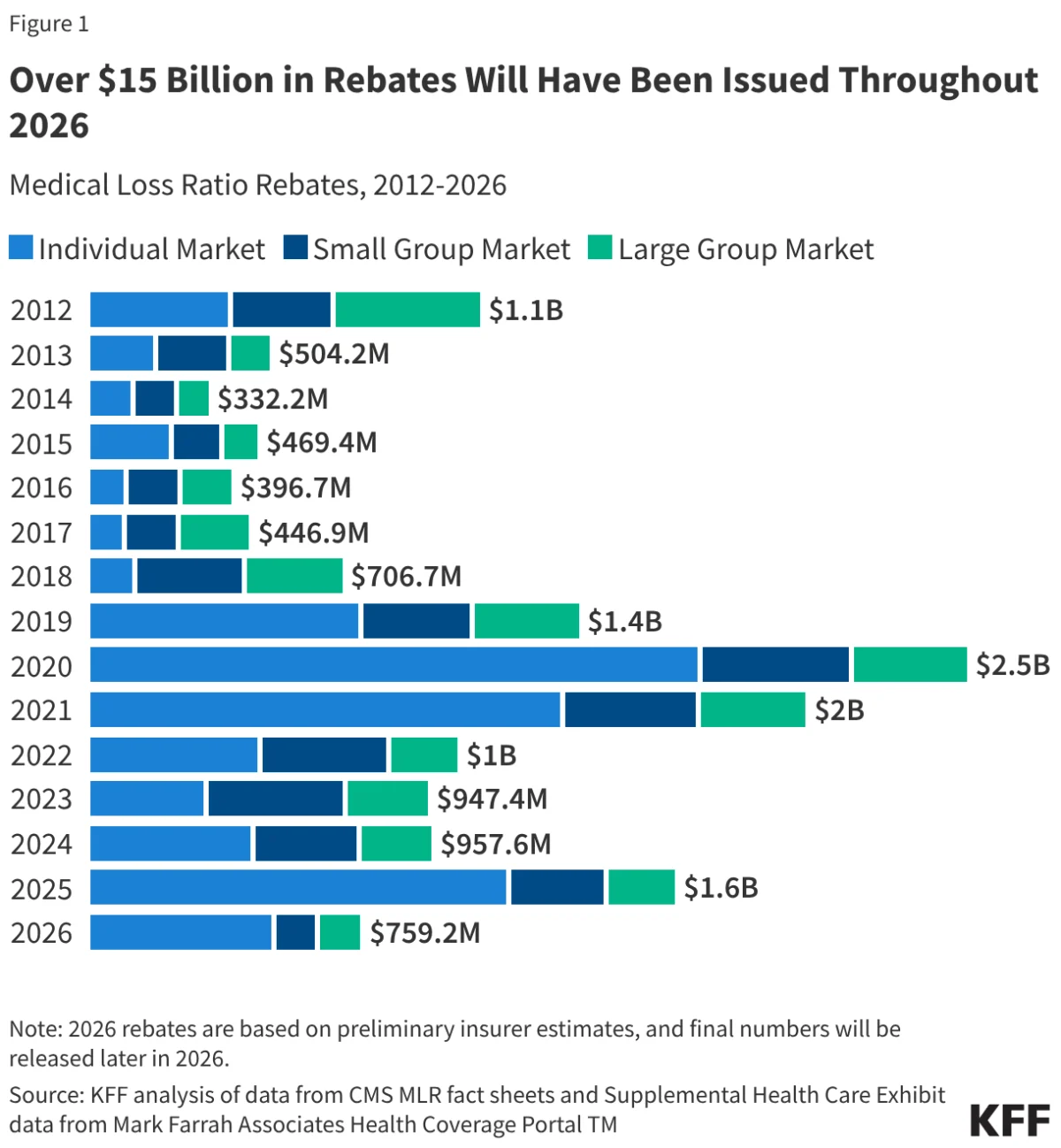

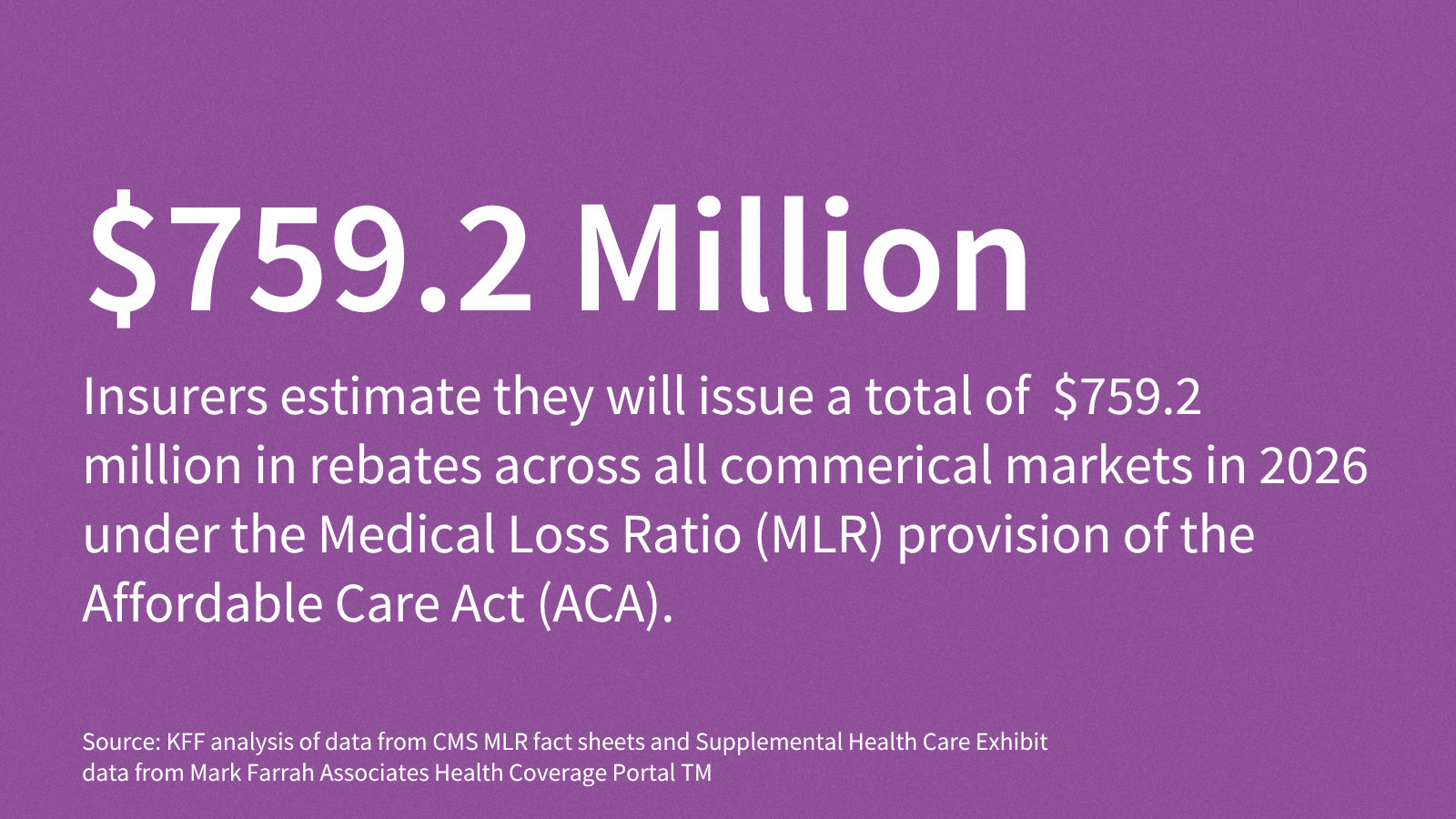

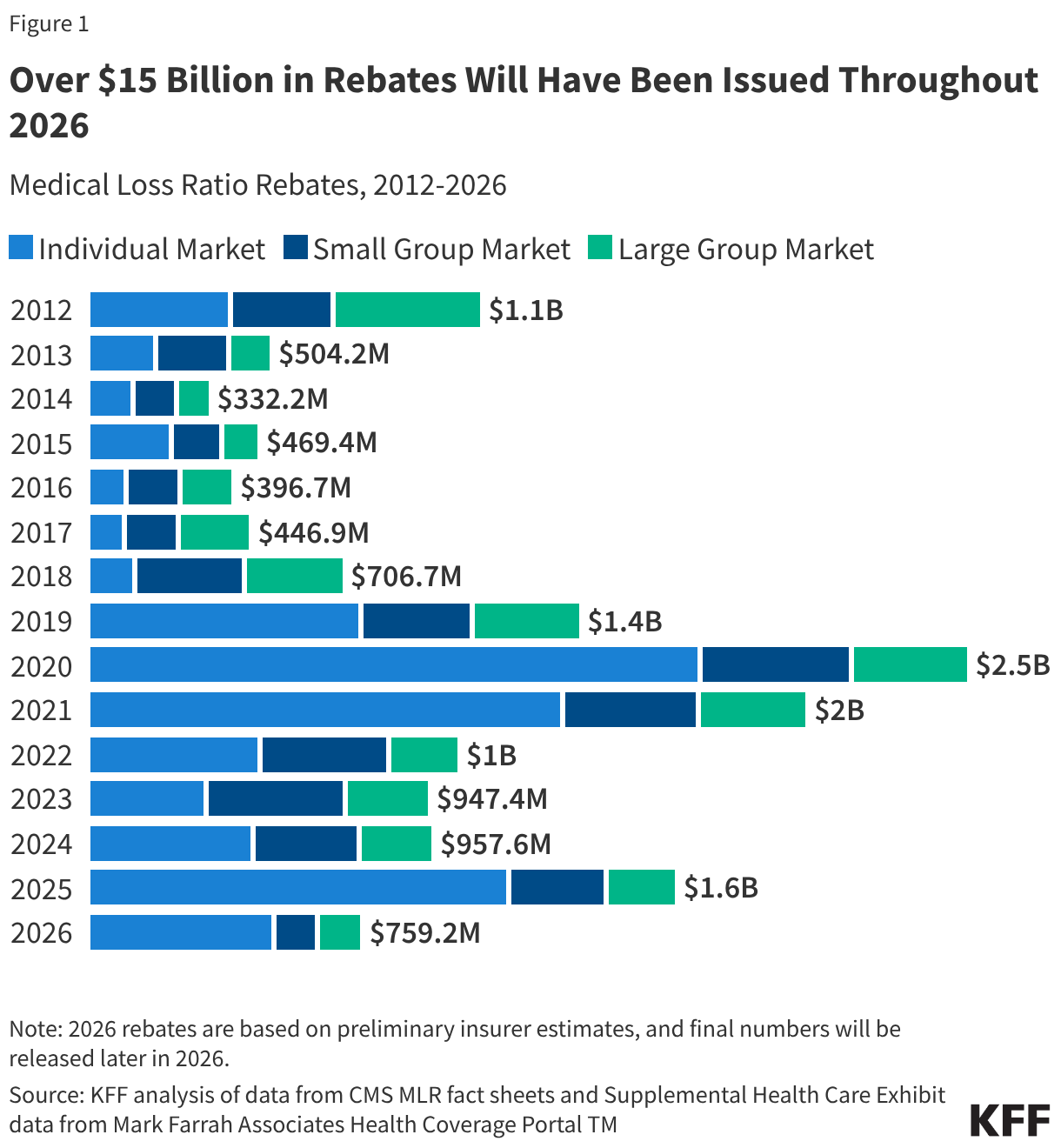

As insurers prepare for the 2026 cycle, preliminary data suggests that the total volume of rebates—the mandatory refunds issued when companies fail to meet these statutory benchmarks—will decline to approximately $759 million. While this figure represents a significant sum, it highlights a period of stabilization in the health insurance market following years of volatility.

Understanding the "80/20" Rule and the Rebate Mechanism

At the heart of the MLR provision is a simple but stringent requirement: insurers must spend a designated percentage of premium dollars on clinical services and quality improvement. For the individual and small group markets, this threshold is 80%. Large group insurers face a stricter requirement, necessitating an 85% expenditure on claims and health quality efforts.

Any revenue remaining—the "allowed" 20% or 15%—is the only portion available for administrative overhead and profit. If an insurer exceeds this cap, they are legally obligated to return the excess to policyholders in the form of a rebate.

These calculations are not based on a single year of financial performance but rather a three-year rolling average. This multi-year approach is designed to smooth out anomalies caused by unpredictable health events, such as a localized disease outbreak or a catastrophic year for medical claims. Consequently, the rebates scheduled for disbursement in 2026 are determined by the financial experience of the insurer across 2023, 2024, and 2025.

A Chronological Perspective: From Record Highs to Normalization

The trajectory of MLR rebates provides a fascinating window into the evolution of the ACA marketplace over the last decade and a half. Since the inception of the mandate in 2012, a staggering $14.4 billion has been returned to consumers and employers. When the 2026 distributions are finalized, this cumulative total is projected to reach approximately $15.1 billion.

The history of these rebates is marked by distinct eras:

- 2012–2017 (The Implementation Phase): During the early years of the ACA, the market underwent significant adjustments as insurers learned to price their products accurately in an environment that included the newly established exchanges.

- 2018–2021 (The Peak Rebate Years): This period saw record-breaking rebate totals, reaching $2.5 billion in 2020 and $2.1 billion in 2021. These spikes were largely driven by two factors: the elimination of cost-sharing reduction (CSR) payments, which led to a strategic "silver-loading" of premiums, and the subsequent, unforeseen decline in medical utilization during the onset of the COVID-19 pandemic. As hospitals canceled elective surgeries and patients delayed routine care, insurers found themselves with vastly higher margins than anticipated, triggering massive rebates.

- 2022–2026 (The Normalization Phase): As claims costs began to climb and align with premium levels, insurers adjusted their pricing models. The rebate totals began to recede from their historic highs, reflecting a market that is no longer characterized by the extreme margin inflation of the late 2010s.

Supporting Data: Analyzing the 2026 Forecast

The projected $759 million for 2026 represents a notable decline from the $958 million issued in 2024 and the $1.6 billion distributed in 2025. According to data compiled by Mark Farrah Associates, the "simple loss ratio"—a metric that tracks the percentage of premiums spent on claims without accounting for the nuanced adjustments required by the ACA—indicates that insurers in the individual market spent roughly 93% of their premium income on claims in 2025.

While a 93% simple loss ratio suggests a tighter profit margin for insurers in the most recent year, the three-year rolling average for 2023–2025 remains the deciding factor for 2026 rebates. If an insurer was exceptionally profitable in 2023 or 2024, they may still owe rebates in 2026, even if their 2025 performance was less lucrative.

The Role of Market Segmentation

The impact of these rebates is distributed unevenly across the insurance landscape:

- Individual Market: Enrollees here saw an average rebate of $233 per person in 2025.

- Small Group Market: Individuals saw an average of $190.

- Large Group Market: Individuals saw an average of $91.

It is critical to note that for employer-sponsored coverage, the rebate may not go directly to the employee. Instead, it is often shared between the employer and the employee based on the specific cost-sharing arrangement of their health plan. Furthermore, if a rebate amount is deemed administratively inefficient to process—less than $5 for individuals or $20 for group plans—insurers are exempt from the requirement to issue them.

Regulatory and Industry Implications

The current state of the insurance market is characterized by a significant shift in premium pricing. Going into 2026, ACA Marketplace premiums have seen their sharpest increase since 2018—rising by more than 20% in some sectors. This suggests that insurers are attempting to insulate themselves against rising medical inflation and potential volatility.

The implications for the consumer are twofold:

- Market Sensitivity: The fact that premiums have spiked suggests that insurers are responding to higher-than-expected utilization. If these higher premiums result in excess margins in 2026, consumers could see a return to higher rebate totals in the 2028–2029 cycle.

- The "Self-Funded" Gap: It is vital for employees to recognize that not all work-provided health plans are subject to these rules. Approximately two-thirds of Americans with employer-sponsored insurance are in "self-funded" plans, where the employer assumes the financial risk. Because these plans are governed by federal ERISA laws rather than the ACA’s MLR provisions, they are exempt from the rebate requirement.

Administrative Logistics: What Consumers Should Expect

For those eligible for a 2026 rebate, the process is largely automated. Insurers are required to mail out rebate checks or apply premium credits by the end of September. The Centers for Medicare & Medicaid Services (CMS) maintains the oversight role, ensuring that insurers report their data accurately and that the calculated rebates reach the appropriate parties.

For the average consumer, a rebate notice may arrive as an unexpected check in the mail or a notification that their next month’s premium payment will be reduced. These rebates serve as a tangible reminder of the ACA’s objective: to ensure that when health insurance becomes more expensive, the increase is driven by the cost of medical care, not by the bottom line of the insurance company.

Conclusion

The projected decline in MLR rebates to $759 million for 2026 is a signal of a maturing, albeit expensive, health insurance market. While the era of multibillion-dollar rebates appears to be in the rearview mirror, the mechanism remains a vital safeguard for consumers. As medical costs continue to rise and premiums follow suit, the MLR provision will remain the primary tool for federal regulators to ensure that the insurance industry remains focused on its primary objective: providing health coverage that serves the patient, not just the profit margins.

As we look toward the remainder of 2026, the focus will shift from these projections to the actual financial filings of insurers, which will determine if the current estimate of $759 million holds or if, as in previous years, the final reality differs from the preliminary data. Regardless of the exact amount, the continued existence of these rebates proves that the ACA’s regulatory framework is actively working to keep insurance providers disciplined in a high-cost medical environment.