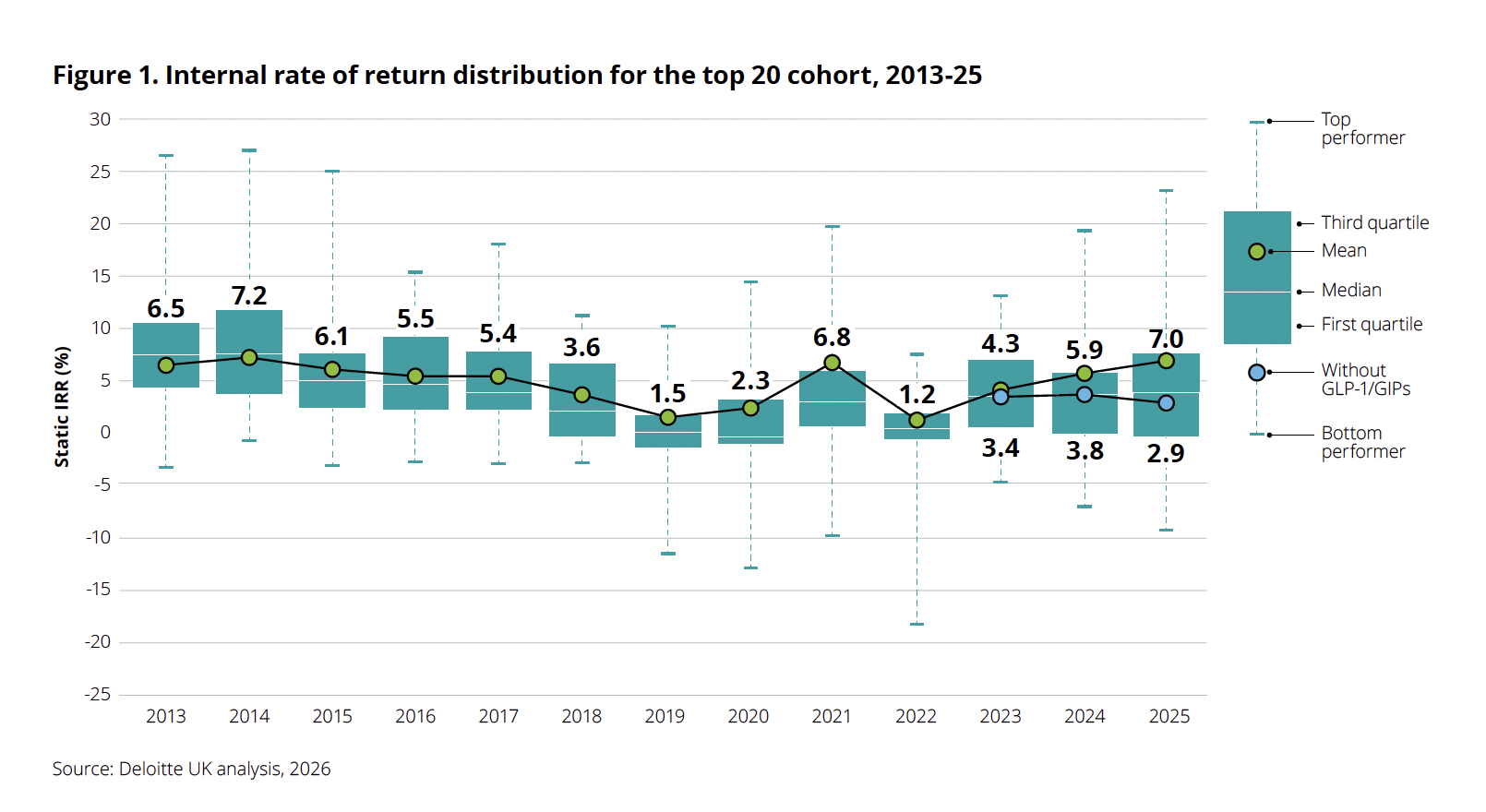

The global biopharmaceutical industry is experiencing a long-awaited thaw after a period of post-pandemic stagnation. According to the 16th edition of Deloitte’s landmark Measuring the Return from Pharmaceutical Innovation report—fittingly titled “Navigating the GLP-1 boom”—the projected internal rate of return (IRR) on late-stage pipeline assets has climbed for the third consecutive year, reaching 7.0% in 2025. This marks a notable recovery from the 5.9% recorded in 2024, signaling a transition from a challenging "industry winter" to a more fertile spring.

However, beneath this headline figure lies a narrative of extreme concentration. The industry’s newfound prosperity is not broad-based; it is fundamentally tethered to the explosive success of GLP-1/GIP receptor agonists. While these metabolic blockbusters have revitalized balance sheets, they have also obscured a more concerning trend: the underlying productivity of the traditional drug pipeline, when isolated from these obesity-focused therapies, is in decline.

The Main Facts: A Sector Defined by Metabolic Success

For over a decade, the pharmaceutical sector grappled with a steady erosion of R&D returns, a trend that seemed almost intractable. The 2025 surge to 7.0% represents an "analytically unprecedented" shift, according to Kevin Dondarski, principal for life sciences strategy at Deloitte Consulting. Yet, the source of this growth is stark.

GLP-1 and GIP therapies, which have revolutionized the treatment of obesity and related metabolic comorbidities, now account for an estimated 38% of all projected commercial inflows from the 2025 late-stage pipeline. The volatility of this reliance is revealed when these assets are stripped from the analysis: the headline IRR plummets from 7.0% to a meager 2.9%. By comparison, when the same adjustment was made in 2024, the IRR fell from 5.9% to 3.8%. This delta highlights a widening gap between the "GLP-1 era" and the rest of the industry’s output.

"There are two different messages here," Dondarski noted. "One, it’s certainly attractive, because the market is valuing the potential impact these therapies have on public health. But at the same time, it raises the question of sustainability. As these programs progress, can companies maintain this momentum through the next generation of assets? The industry bears a significant responsibility to replace these pillars with equally robust innovations."

Chronology: The Rise and Turbulence of the Metabolic Giants

The dominance of obesity drugs has created a unique, high-stakes environment for the industry’s two primary titans: Eli Lilly and Novo Nordisk.

2025: A Year of Structural Overhaul

The year 2025 served as a inflection point. Novo Nordisk, facing pressure from a crowded market and cooling momentum, initiated a massive leadership and organizational restructuring. Longtime CEO Lars Fruergaard Jorgensen was succeeded by Maziar Mike Doustdar. Simultaneously, the company saw seven board members depart during an extraordinary general meeting in November, accompanied by a strategic decision to cut 9,000 roles—a move that, by May 2026, appears to have expanded into a total workforce reduction of over 10,000 employees.

Early 2026: The "CagriSema" Setback and Market Realignment

Investor confidence was further rattled in February 2026, when Novo Nordisk’s clinical candidate CagriSema—a combination of the amylin analogue cagrilintide and semaglutide—failed to meet its primary endpoint of non-inferiority against Lilly’s Zepbound. The trial, dubbed REDEFINE 4, showed 23.0% weight loss for the Novo candidate compared to 25.5% for tirzepatide.

By April 2026, Eli Lilly launched its oral GLP-1, orforglipron (marketed as Foundayo), yet even with this innovation, the company’s stock faced a 10-13% decline year-to-date. This irony—that companies are hitting record revenue targets while facing share-price pressure—underscores the market’s deep skepticism regarding the long-term price ceilings and durability of the GLP-1 category.

Supporting Data: The Cost of Innovation

The Deloitte report paints a vivid, if challenging, picture of the cost of modern drug discovery. The average cost to develop a drug from the lab bench to market launch has escalated to $2.67 billion in 2025, up from $2.23 billion the previous year.

This is not a story of one or two failed projects; it is a systemic trend. Deloitte found that costs increased for 17 out of the 20 companies analyzed. Three primary drivers are responsible for this inflationary pressure:

- Persistent R&D Inflation: Costs are rising at a rate consistently higher than the general consumer price index.

- M&A-Driven Expansion: Frequent, large-scale acquisitions are inflating the R&D cost base, often without immediate, proportional gains in pipeline velocity.

- Clinical Attrition: A 4-5% reduction in the total number of late-stage programs has forced companies to spend more to protect fewer assets.

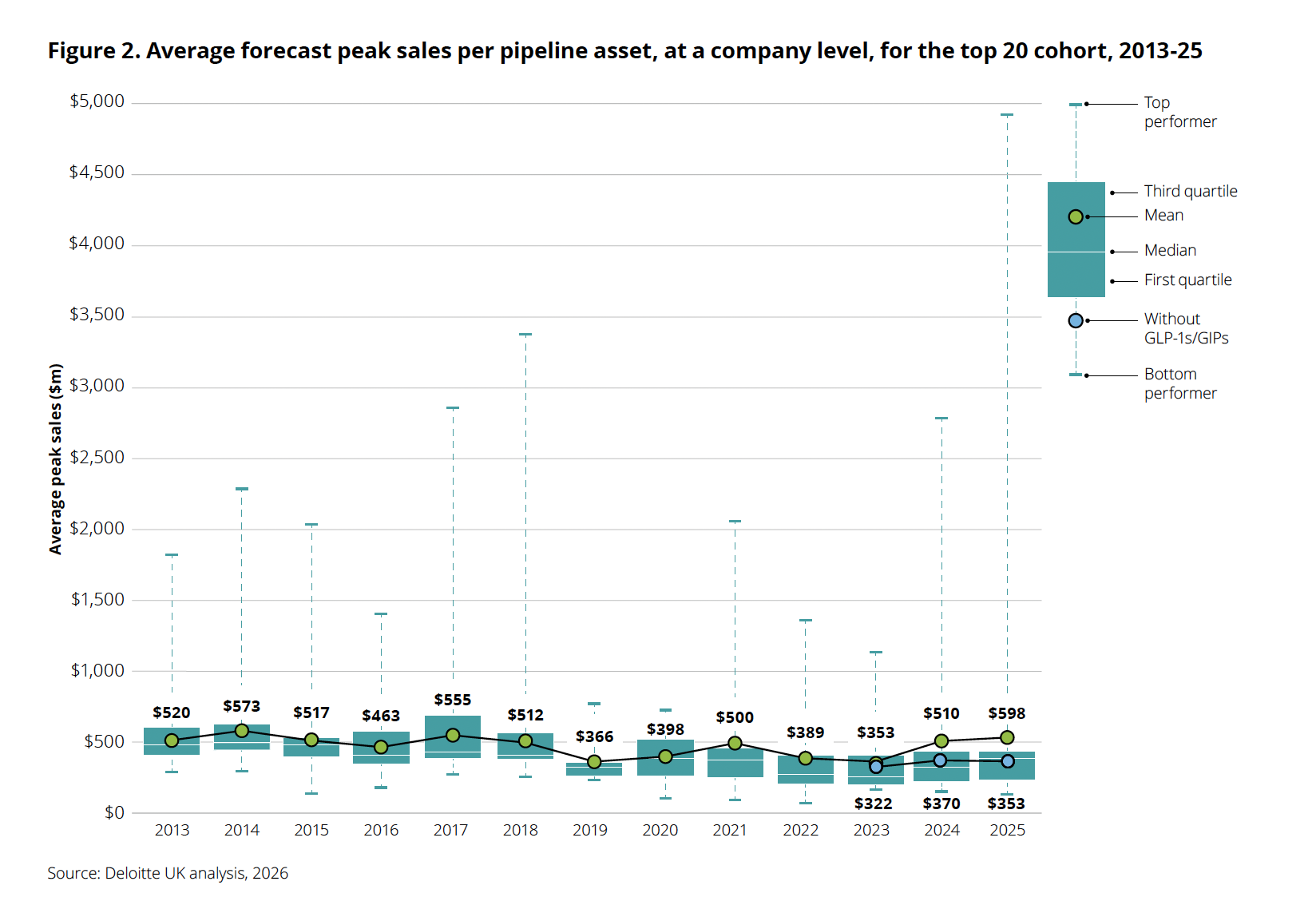

Perhaps most concerning is the "spread" in peak sales forecasts. While the average peak sales per asset jumped to $598 million, the top-performing assets are skewing this data significantly, nearing $5 billion in potential revenue. If the GLP-1 blockbusters are removed from the calculation, the average peak sales figure drops to just $353 million—a lower figure than the previous year. This confirms that for the majority of the pipeline, productivity is not just stagnant; it is actively retreating.

Official Responses and Strategic Implications

The industry is currently in a defensive posture, seeking to lower costs while managing the optics of public pricing. In late 2025, both Eli Lilly and Novo Nordisk reached agreements to lower U.S. prices for GLP-1 therapies via Medicare, Medicaid, and the private-sector "TrumpRx" initiative.

The resulting price structure—where a monthly supply of an oral Wegovy pill is listed at $149 and Zepbound at $299—reflects a new era of price sensitivity. This downward pressure on realized prices is already manifesting in quarterly earnings. Eli Lilly reported a 13% decline in realized prices in Q1 2026, despite a 65% surge in volume. Similarly, Novo Nordisk’s adjusted sales fell 4% at constant exchange rates once one-time accounting provisions were excluded.

The AI Gap: A Promised Revolution Delayed

Last year’s Deloitte report, “Be Brave, Be Bold,” centered on the transformative potential of artificial intelligence to rescue the industry from its productivity crisis. However, the 2025 data suggests that the "AI revolution" remains largely in the pilot stage.

"Everybody is actively focusing on AI, and everybody has had some degree of success," Dondarski noted. "But from our vantage point, there is a good amount of variability in the velocity at which organizations are scaling those efforts." The report concludes that AI’s promise to slash development times and costs has not yet been realized at scale, as most firms are stuck in a fragmented, function-by-function implementation model rather than a holistic, platform-based overhaul.

Implications: A Crossroads for Big Pharma

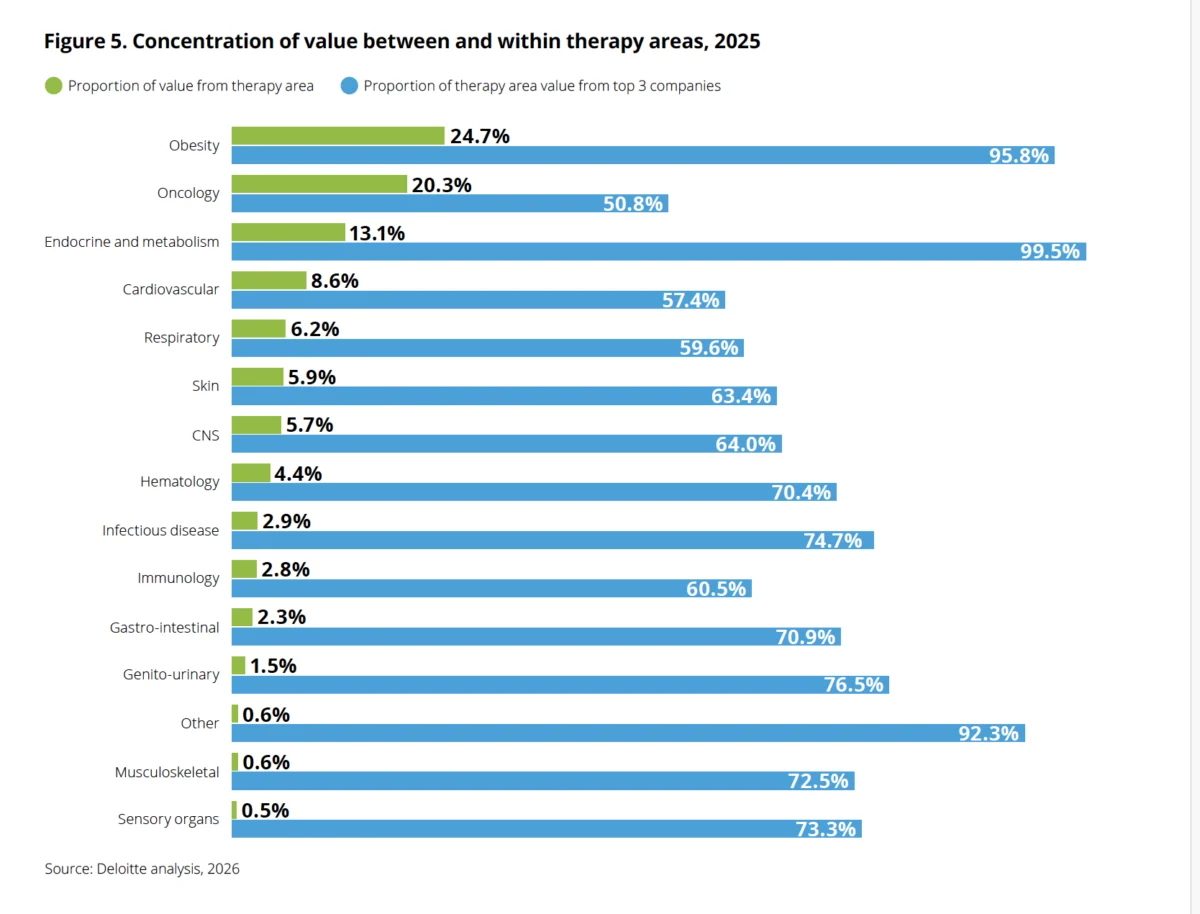

The implications for the biopharma sector are clear: the current reliance on the "golden goose" of GLP-1s is a temporary buffer, not a long-term strategy. The concentration of value is unprecedented, with nearly 96% of the obesity-related pipeline value controlled by only three companies.

As the industry moves toward 2027, the challenge will be two-fold. First, companies must navigate the "post-boom" environment, where high volume is increasingly offset by lower margins and tighter regulatory pricing controls. Second, they must address the R&D cost crisis. With the cost of bringing a drug to market approaching nearly $3 billion, the industry can no longer afford the inefficiencies of traditional, non-AI-integrated development cycles.

The shift from "winter to spring" identified by Deloitte is a welcome development, but it is a fragile one. Unless the industry can broaden its innovation base beyond metabolic diseases and successfully scale the productivity gains promised by digital and AI-driven platforms, the return to 7.0% may prove to be a short-lived anomaly rather than a return to long-term, sustainable growth. The coming years will require a pivot from the "GLP-1 boom" to a more diversified, cost-efficient, and technologically advanced model of drug discovery.