The landscape of American health insurance has undergone a tectonic shift in 2026. Following the expiration of the enhanced premium tax credits—a cornerstone of the 2021 American Rescue Plan and the 2022 Inflation Reduction Act—millions of Americans are navigating a new, more expensive reality. After years of record-breaking enrollment and historically low premiums, the Affordable Care Act (ACA) Marketplace is experiencing its most significant contraction since its inception.

This shift has created a dual crisis: a sharp decline in total coverage and a "coverage downgrade" for those who remain, as many families trade comprehensive silver-tier plans for high-deductible bronze options to keep monthly costs manageable. As federal data and private sector projections begin to crystallize, the true cost of the subsidy cliff is becoming clear.

Main Facts: A Market in Contraction

The primary driver of the current instability is the return of the "subsidy cliff." Under the enhanced provisions, federal tax credits were significantly expanded, effectively capping the cost of benchmark silver plans for most households and removing the income-based ceiling that previously disqualified many middle-income earners from assistance.

When these enhancements sunsetted at the end of 2025, the fiscal impact was immediate. By the close of the 2026 Open Enrollment Period, plan sign-ups had plummeted by over one million people, falling to 23.1 million. However, experts warn that "sign-ups" are a lagging indicator of actual coverage. Because sign-up data captures intent rather than financial commitment, the actual number of people who will pay their premiums and maintain "effectuated" coverage throughout the year is expected to be significantly lower.

Projections from the Wakely Consulting Group and the Congressional Budget Office (CBO) suggest that the individual market could see a total enrollment decline of 17% to 26% compared to 2025. This equates to an estimated loss of roughly 4.8 million people—a staggering reversal of the progress made over the previous five years.

Chronology of the Policy Shift

To understand the current volatility, one must look at the timeline of federal intervention and its subsequent retreat:

- 2021: The American Rescue Plan (ARP) is signed into law, introducing temporary, enhanced premium tax credits that lower premiums for current enrollees and expand eligibility to those earning more than 400% of the federal poverty level (FPL).

- 2022: The Inflation Reduction Act (IRA) extends these enhanced credits through the end of 2025, cementing a period of record-high enrollment and affordability.

- Late 2025: As the expiration date approaches, insurers and analysts begin warning of a "payment shock" for consumers. Despite efforts by some states to fill the void, the loss of federal dollars becomes inevitable.

- January 2026: The first month of the new, unsubsidized era. Early data shows a massive uptick in cancellations and non-payment terminations.

- Spring 2026: KFF surveys and state-level reports from California and Maryland confirm that the "subsidy cliff" is forcing a mass exodus, particularly among middle-income families and young, healthy adults.

Supporting Data: Who Is Leaving and Why?

The data reveals that the burden of the subsidy expiration is not distributed equally. The demographic impact is most concentrated among those who were newly empowered by the enhanced credits.

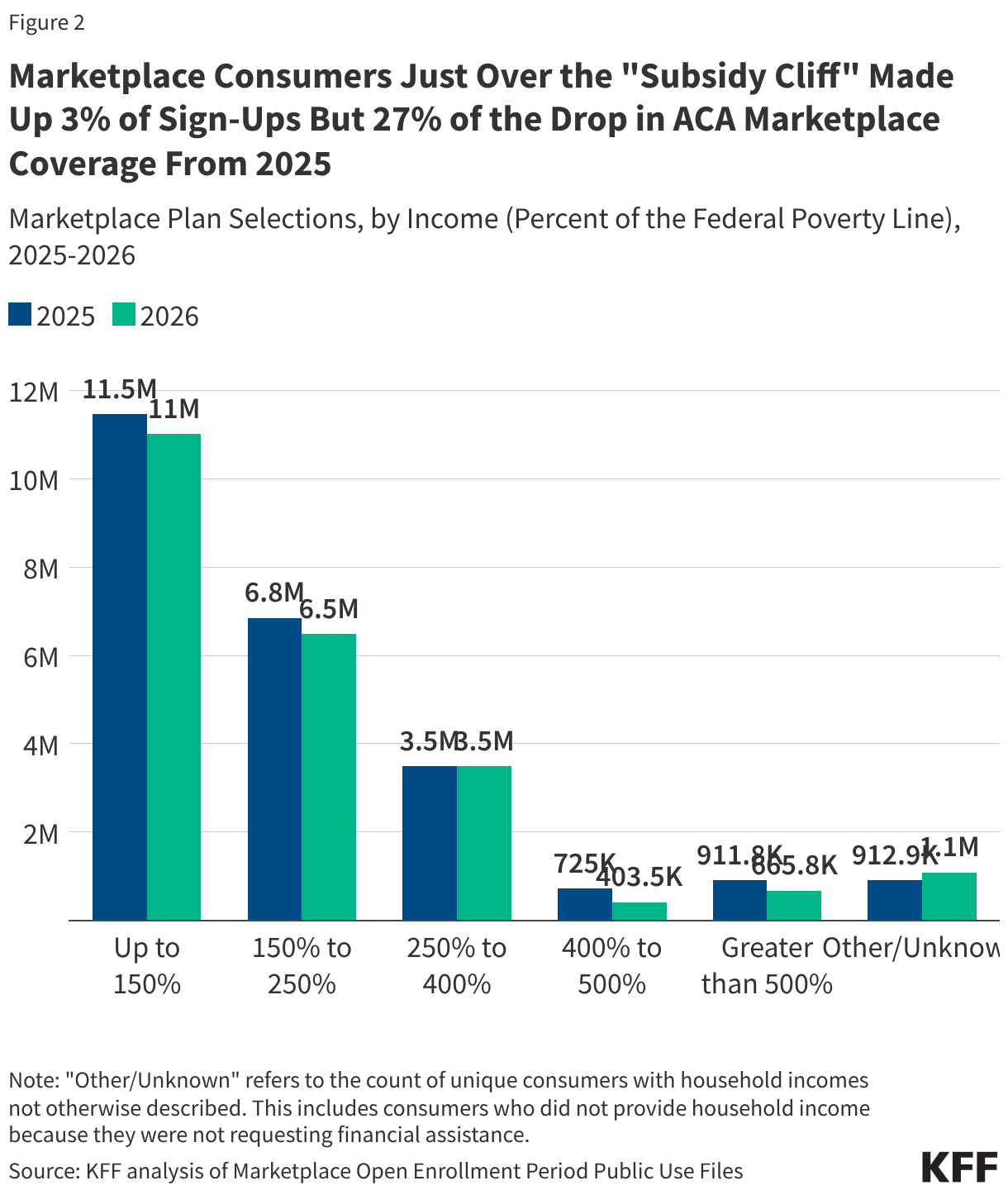

The Subsidy Cliff Impact

Consumers with incomes between 400% and 500% of the FPL represent a small slice of total enrollment (3%), yet they accounted for a disproportionate 27% of the total decline in sign-ups. For these households, the expiration of subsidies resulted in an immediate, significant jump in monthly premiums, pushing them out of the market entirely. Those earning above 500% FPL accounted for an additional 21% of the decline. In total, those "above the cliff" represented nearly half of the entire reduction in enrollment.

The Youth Exodus

Young adults (ages 18–34) have historically been the most price-sensitive segment of the insurance market. This demographic accounted for 46% of the total decline in ACA Marketplace sign-ups in 2026. As premiums rose, many in this age group—often feeling "invincible"—opted to forgo coverage, a trend that health economists fear will lead to a "sicker" risk pool and higher long-term costs for remaining enrollees.

The Shift to "Bronze" Plans

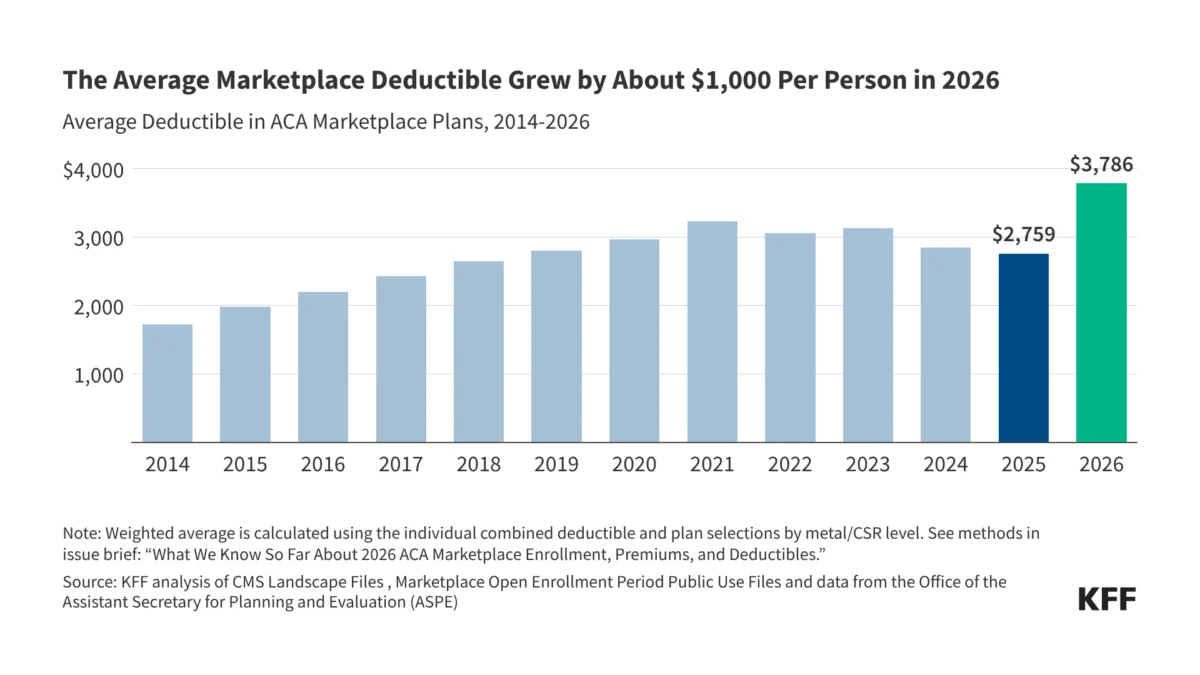

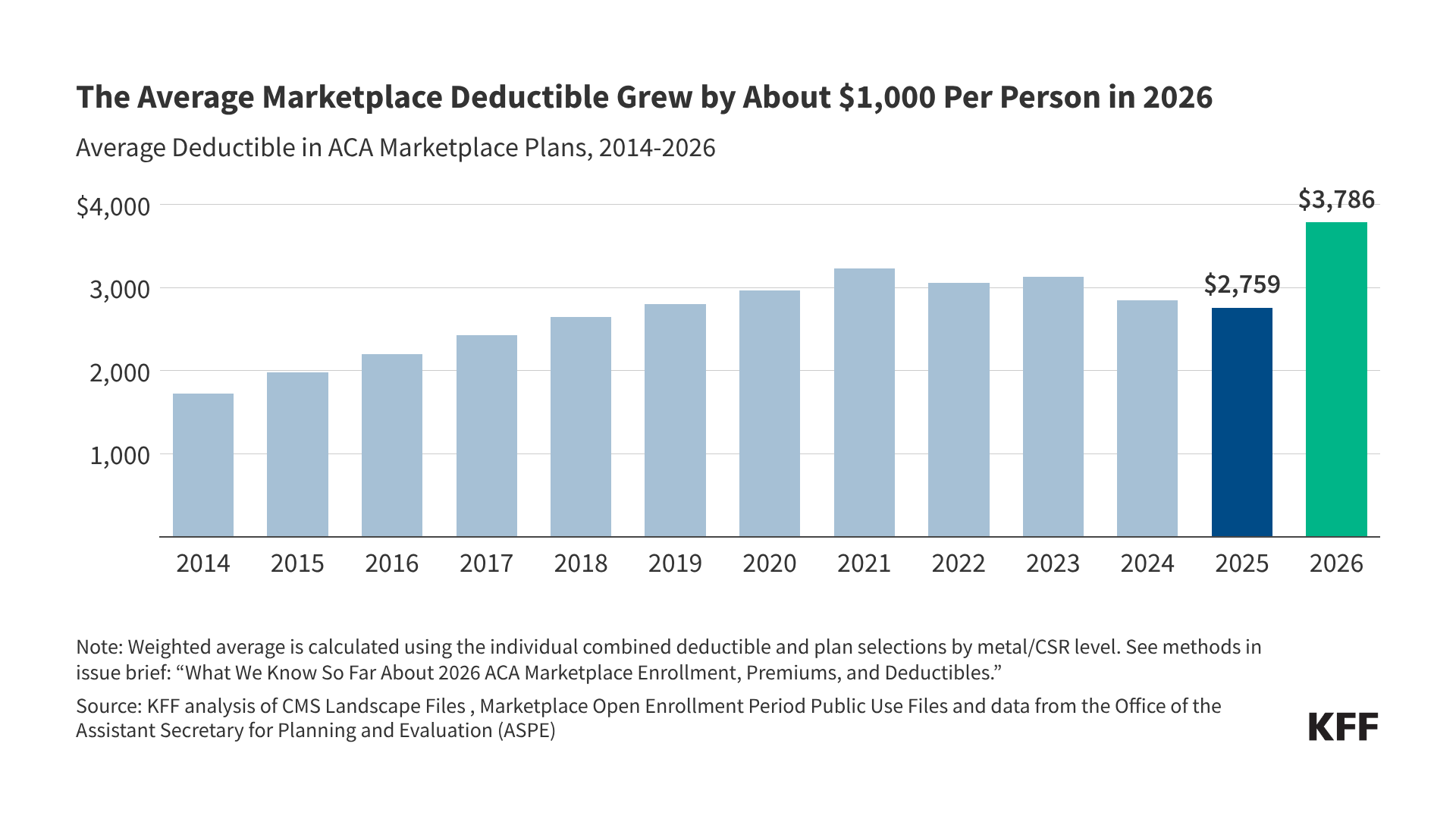

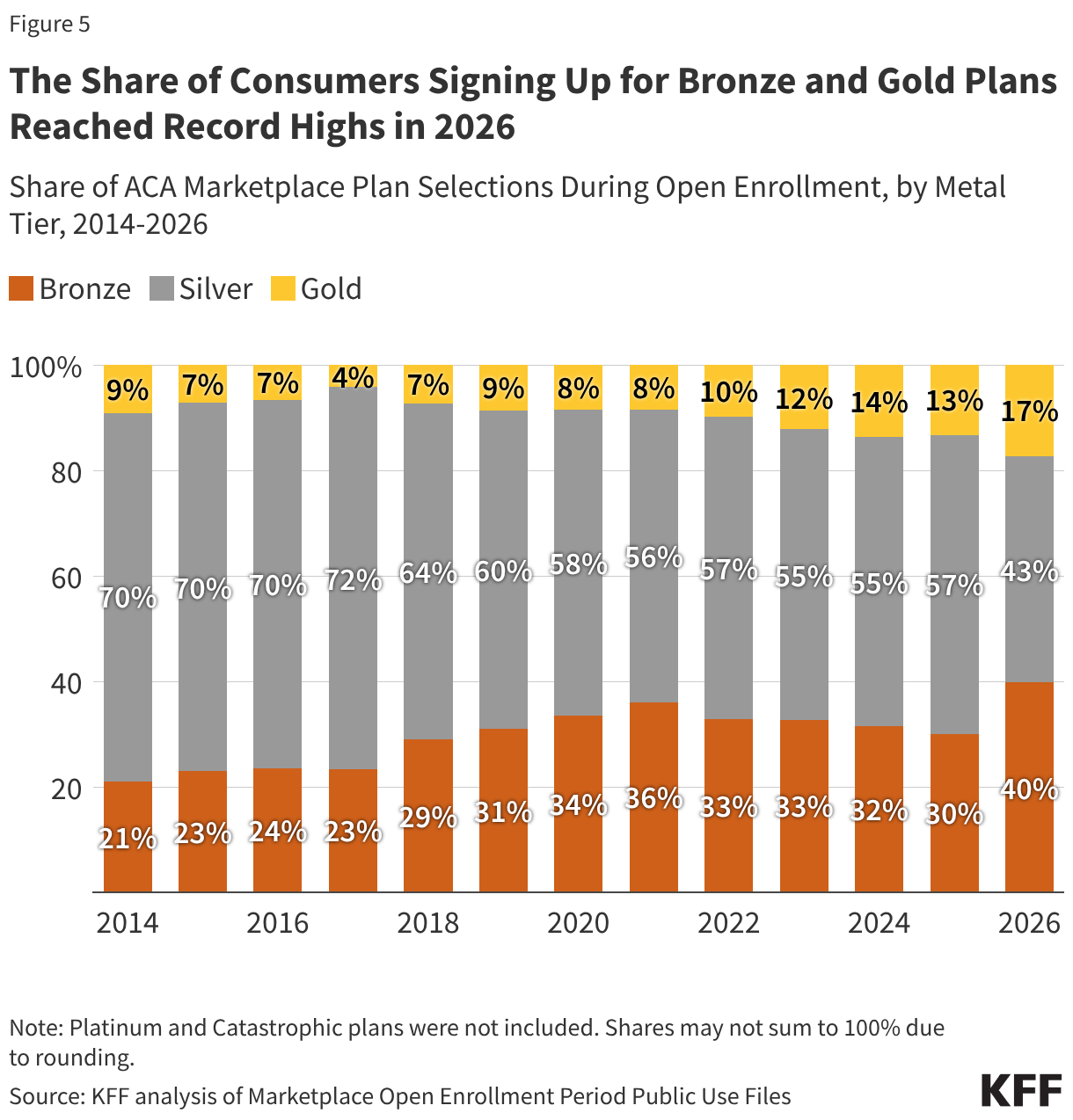

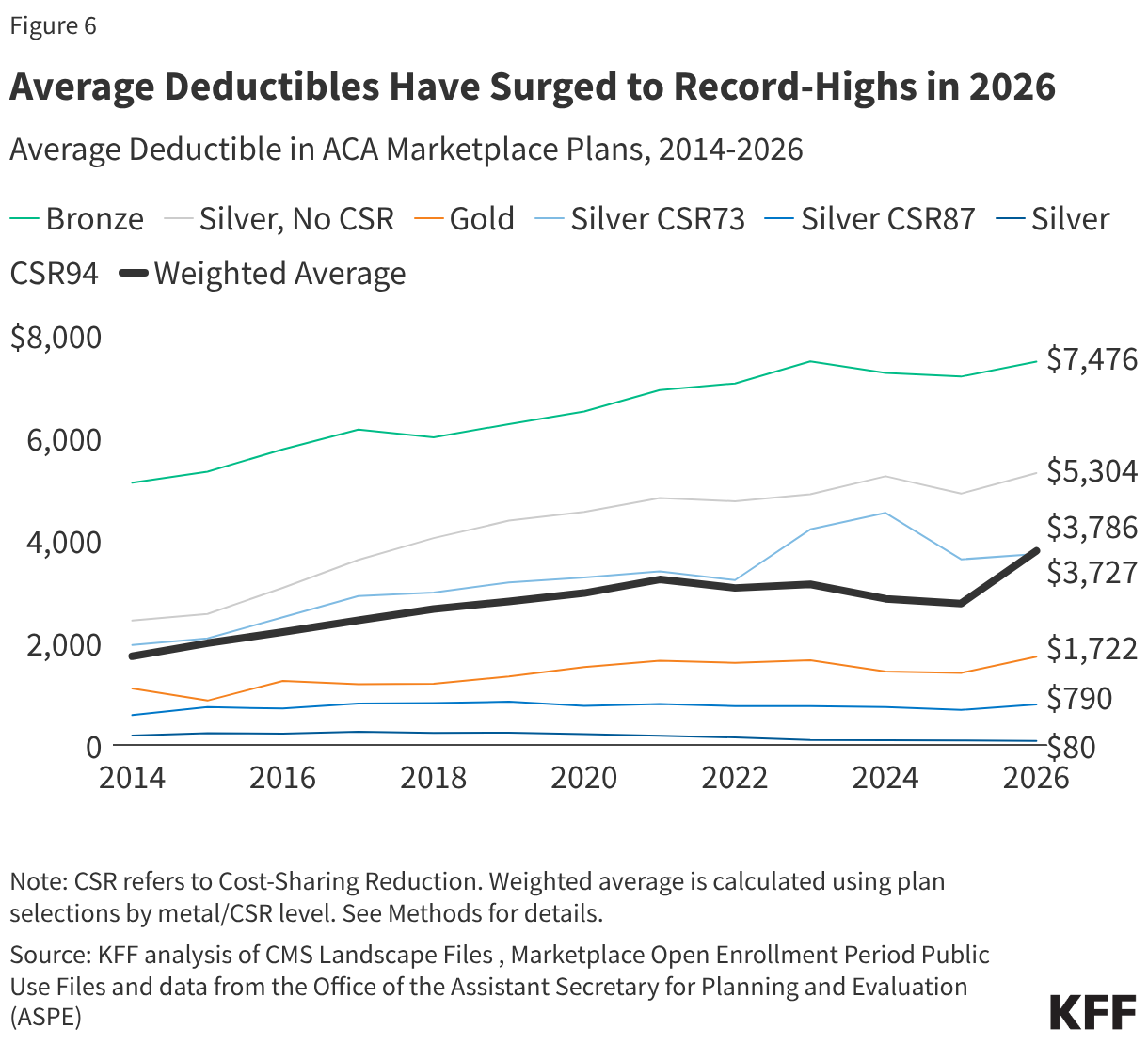

For those who stayed, the strategy has been to buy down. The share of consumers selecting silver plans—which offer better value through lower deductibles—fell below 50% for the first time in the program’s history. Simultaneously, enrollment in bronze plans surged to 40%. The result is a sharp increase in the average deductible, which has risen by 37% in a single year, climbing from $2,759 to $3,786. This creates a "hidden" cost: while some families managed to keep their insurance, their actual out-of-pocket exposure for medical care has skyrocketed.

Official Responses and State-Level Variability

The federal government, through the Centers for Medicare & Medicaid Services (CMS), continues to monitor the situation, but the ability to provide relief is currently limited by the existing legislative framework.

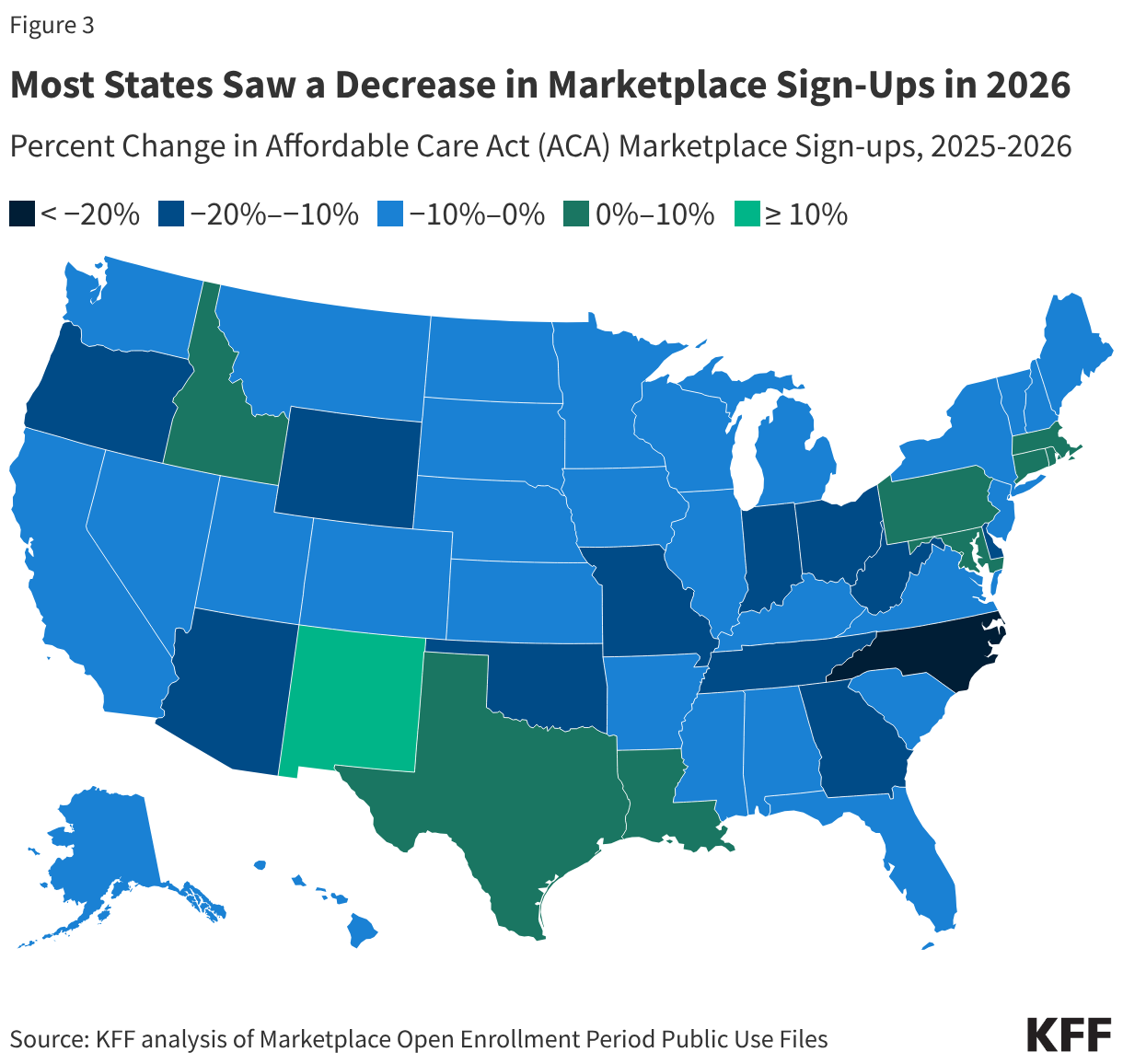

In the absence of federal action, states have become the primary battleground for health policy. State-based exchanges (SBMs) have largely outperformed the federal Marketplace. States like New Mexico have taken aggressive action, implementing supplemental financial assistance programs that backfill the lost federal credits. This has allowed those states to maintain, or in some cases grow, their enrollment figures. Conversely, states relying on the federal platform (Healthcare.gov) have seen the most drastic declines, as they lack the local funding mechanisms to soften the blow of the subsidy expiration.

Implications for the Future

The implications of the 2026 enrollment collapse are profound and multi-faceted:

1. The "Coverage Gap" Expands: The decline in enrollment is not merely a statistical anomaly; it represents millions of Americans moving toward the uninsured category. This creates a public health risk, as delayed care often results in more expensive emergency room interventions later.

2. Increased Administrative Strain: The high rate of "churn"—where people sign up, fail to pay, and are subsequently terminated—creates an administrative burden on insurers and marketplaces. This instability makes long-term premium forecasting nearly impossible, leading to potential price volatility in the 2027 plan year.

3. The CSR Dilemma: The sharp decline in the use of Cost-Sharing Reductions (CSRs) among eligible low-income enrollees is particularly concerning. Many families appear to be choosing lower-premium bronze plans without realizing that they are walking away from thousands of dollars in potential savings on deductibles and co-pays. This highlights a critical need for better consumer education and navigation support.

4. Long-Term Market Viability: If the current trajectory continues, the ACA Marketplace risks becoming a program primarily for the lowest-income tiers, losing the broad participation that keeps the market balanced. As younger and middle-income consumers flee, the "risk pool" could deteriorate, forcing premiums even higher for those who remain and cannot afford to leave.

As the 2026 calendar year progresses, the full picture of the post-subsidy landscape will continue to emerge. For now, the data serves as a stark reminder of the influence of federal policy on the lives of millions. The "Great Unwinding" is not just about numbers; it is a fundamental shift in the accessibility of the American healthcare system, one that will likely dominate the political and economic discourse for the remainder of the decade.