In the high-stakes world of global technology, financial earnings reports are rearview mirrors—accurate, but fundamentally historical. For corporate leaders and institutional investors, the real-time pulse of the industry is not found in balance sheets, but in the hiring pages of major semiconductor firms. As of April 2026, shifting patterns in global recruitment are signaling a subtle but significant recalibration of the industry’s strategic priorities.

Hiring data acts as an early warning system. By tracking the specific skills, regions, and themes that companies are investing in, executives can identify where competitors are pivoting—often months before those shifts manifest in quarterly revenue or market share adjustments. With a "positioning window" of roughly one to three months, the ability to interpret these signals is the difference between leading the market and reacting to it.

The State of Play: A Cooling Trend or a Strategic Pause?

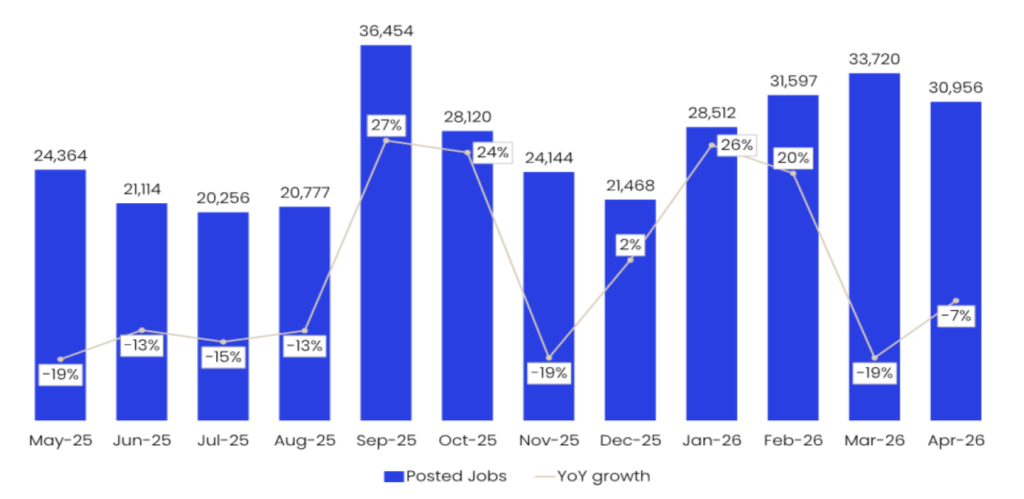

The global semiconductor sector experienced a notable contraction in April 2026, with job postings falling by 6.58% month-on-month to 30,956. This decline marks the second consecutive monthly drop, following a period of aggressive expansion between January and February.

Chronology of the 2026 Hiring Cycle

- Q3 2025: Volatile hiring patterns begin to emerge as global supply chain pressures ease.

- September 2025: A significant step-up in recruitment activity suggests a late-year push for R&D capacity.

- January–February 2026: A sharp acceleration in hiring across the sector as companies race to capitalize on the AI infrastructure boom.

- March–April 2026: A period of "retrenchment," where firms appear to be optimizing existing teams rather than expanding headcounts.

Despite the recent cooling, it is critical to note that the industry is not in a freefall. Current posting levels remain comfortably above the December 2025 baseline. This indicates that while the frantic pace of early-year recruitment has subsided, the sector is maintaining a "higher run-rate" than the troughs seen in mid-2025. This suggests that the current pullback is a tactical correction—a pause to digest the massive influx of talent hired earlier in the year—rather than a fundamental retreat from long-term growth objectives.

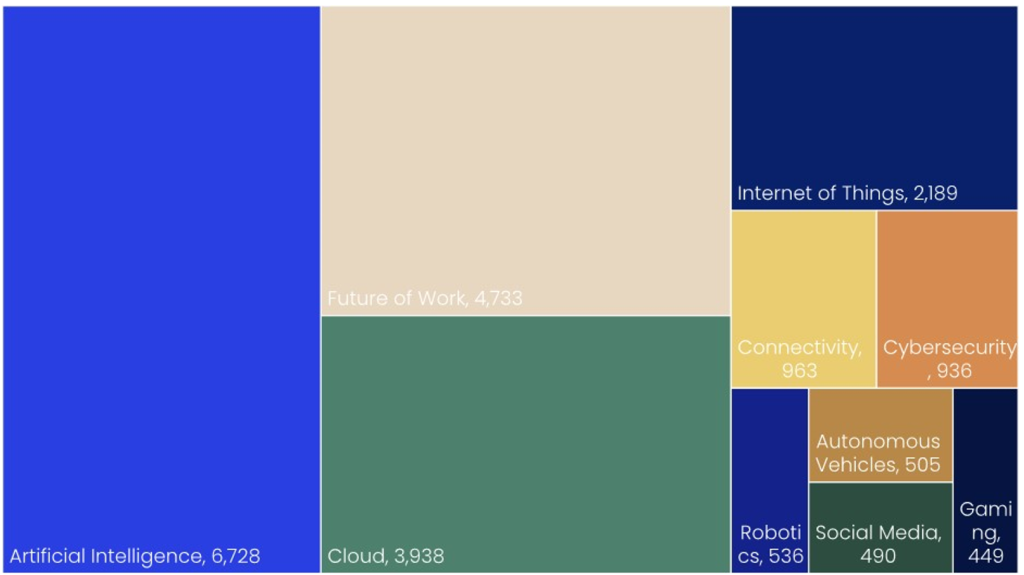

The Dominance of AI and the "Software-Adjacent" Pivot

The thematic breakdown of these job postings reveals where the "real bets" are being placed. The semiconductor industry is no longer just about hardware manufacturing; it is increasingly defined by its software-adjacent capabilities.

Leading Themes Driving Recruitment

- Artificial Intelligence (AI): With 6,728 postings, AI remains the undisputed heavyweight of the semiconductor hiring landscape. This reflects the industry’s massive investment in compute-heavy workloads required for training and deploying large language models.

- Future of Work (FOW): Capturing 4,733 postings, the FOW theme highlights a focus on internal digital transformation and the infrastructure required to support decentralized, high-efficiency engineering teams.

- Cloud Computing: Accounting for 3,938 postings, the reliance on cloud infrastructure remains a cornerstone of semiconductor development, emphasizing the transition from on-premise hardware testing to scalable, cloud-based simulation.

Secondary themes, including the Internet of Things (IoT) and connectivity, remain relevant but are significantly smaller in scale. The "long tail" of recruitment—covering robotics, autonomous vehicles, and gaming—suggests that while these sectors remain vital, they are currently secondary to the primary push toward foundational AI and cloud infrastructure.

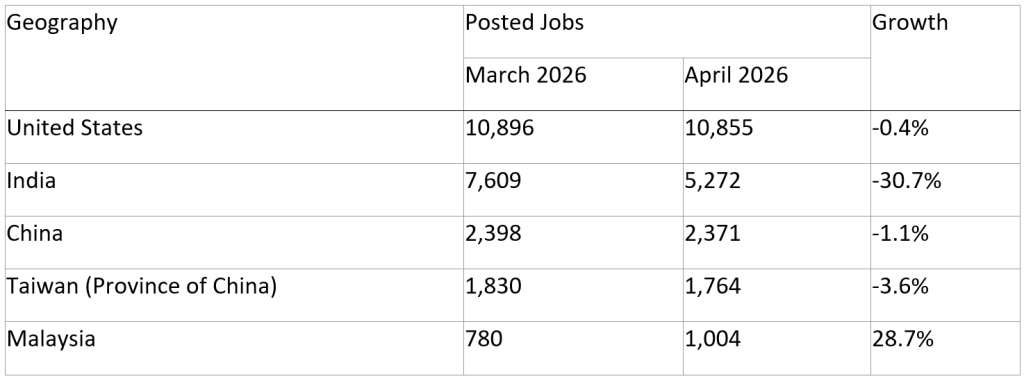

Geographic Shifts: The New Frontiers of Production

The geographic distribution of job postings in April 2026 paints a picture of a sector undergoing a subtle realignment. The United States remains the undisputed global hub for semiconductor talent, with postings remaining essentially flat (-0.4% month-on-month). This stability signals that despite broader economic fluctuations, the US continues to be the primary battleground for top-tier chip engineering talent.

However, the contrast between other major markets is stark:

- India: Recorded the most significant contraction, with a 30.7% drop in postings. This sudden shift indicates a possible consolidation of roles or a rebalancing of global teams.

- China and Taiwan: Both markets saw marginal declines (1.1% and 3.6% respectively), reflecting a measured, cautious approach to growth in these historically critical semiconductor centers.

- Malaysia: A standout performer, Malaysia saw a 28.7% growth in postings. This surge marks Malaysia as an increasingly vital node in the global semiconductor supply chain, likely benefiting from "China Plus One" strategies as firms diversify their geographic risk.

Employer Dynamics: The Shift Toward Efficiency

The hiring behavior of industry titans provides the most granular view of strategic intent. IBM, while maintaining the top spot for total job postings (4,248), has seen a marked decline from its February peak of 9,517. This volatility is not necessarily a sign of weakness, but rather a sign of a "burst" hiring strategy aimed at scaling up for specific project milestones.

Conversely, Hitachi has maintained impressive stability, keeping its hiring levels consistent at approximately 2,300 postings. Other firms, such as Qualcomm and Huawei, have shown moderate growth, suggesting a focus on specialized expansion. A notable newcomer to the top-employer list is Infineon, which pivoted from near-zero hiring in Q1 to a robust 751 postings in April. This sudden re-entry into the talent market is a classic indicator of a company shifting from a "defensive" posture to an "offensive" growth phase.

Technical Skills: The Building Blocks of the Future

If you want to know what a semiconductor company is building, look at the technical skills they are advertising. The current data points to a massive emphasis on infrastructure-level engineering:

- Application Platforms and Containers (4,960 postings): The primary demand for skills in Docker, Kubernetes, and similar containerization platforms highlights the industry’s shift toward modular, scalable software environments.

- Systems Design and Integration (3,637 postings): This confirms that the bottleneck in chip development is no longer just the silicon itself, but the complex integration of hardware with high-level software stacks.

- Operating Systems (3,408 postings): The high demand for OS-level expertise suggests a drive toward deeper customization of the kernel and firmware layers to maximize the performance of AI-specific hardware.

Implications for Strategic Leadership

For the modern executive, this data is not merely an HR metric; it is a vital component of competitive intelligence. When job postings lead earnings revisions by one to three months, waiting for the official quarterly report to arrive is, by definition, a lagging strategy.

Three Pillars for Strategy Decision-Making

- Monitor Competitor "Headcount Velocity": If a competitor suddenly spikes hiring in a specific region—like the recent growth in Malaysia—they are likely standing up new infrastructure or supply chain capabilities.

- Analyze Skill Shifts as Product Roadmaps: A shift toward containerization and platform engineering is a clear signal that the industry is moving away from bespoke, monolithic hardware design toward software-defined silicon.

- Use Hiring Data to Spot Overexposure: If a sector or region experiences a sharp, sustained contraction in hiring, it may indicate a strategic retreat. Leaders can use this information to identify where competitors are pulling back, potentially creating a gap in the market for aggressive expansion.

Conclusion: The Power of Proactive Intelligence

The semiconductor industry is currently navigating a period of transition. The rapid, feverish hiring of early 2026 has transitioned into a more calculated, efficiency-focused phase. For leaders, this is not a sign of stagnation but a unique opportunity to gain clarity on the industry’s direction.

As the lines between hardware and software continue to blur, the companies that successfully integrate their talent acquisition strategies with their long-term R&D roadmaps will be the ones that define the next decade of computing. In this environment, access to granular, point-in-time hiring data is not just an advantage—it is a requirement for survival. By translating these complex hiring patterns into actionable signals, organizations can move from the uncertainty of the "consensus" view to the precision of data-driven foresight.