For the first time since the introduction of enhanced premium tax credits in 2021, the robust expansion of the Affordable Care Act (ACA) Marketplaces has hit a structural speed bump. As the enhanced federal subsidies expired at the end of 2025, the insurance market has begun to recalibrate, leading to a measurable decline in insurer participation. This cooling period, marked by the high-profile departure of CVS Aetna from 17 states, signals a transition from a period of aggressive growth to one of strategic contraction. While the current number of insurers remains healthier than pre-2021 levels, the data for 2026 suggests that the "gold rush" era of Marketplace expansion may be giving way to a more cautious, bottom-line-driven environment.

Main Facts: A Market in Transition

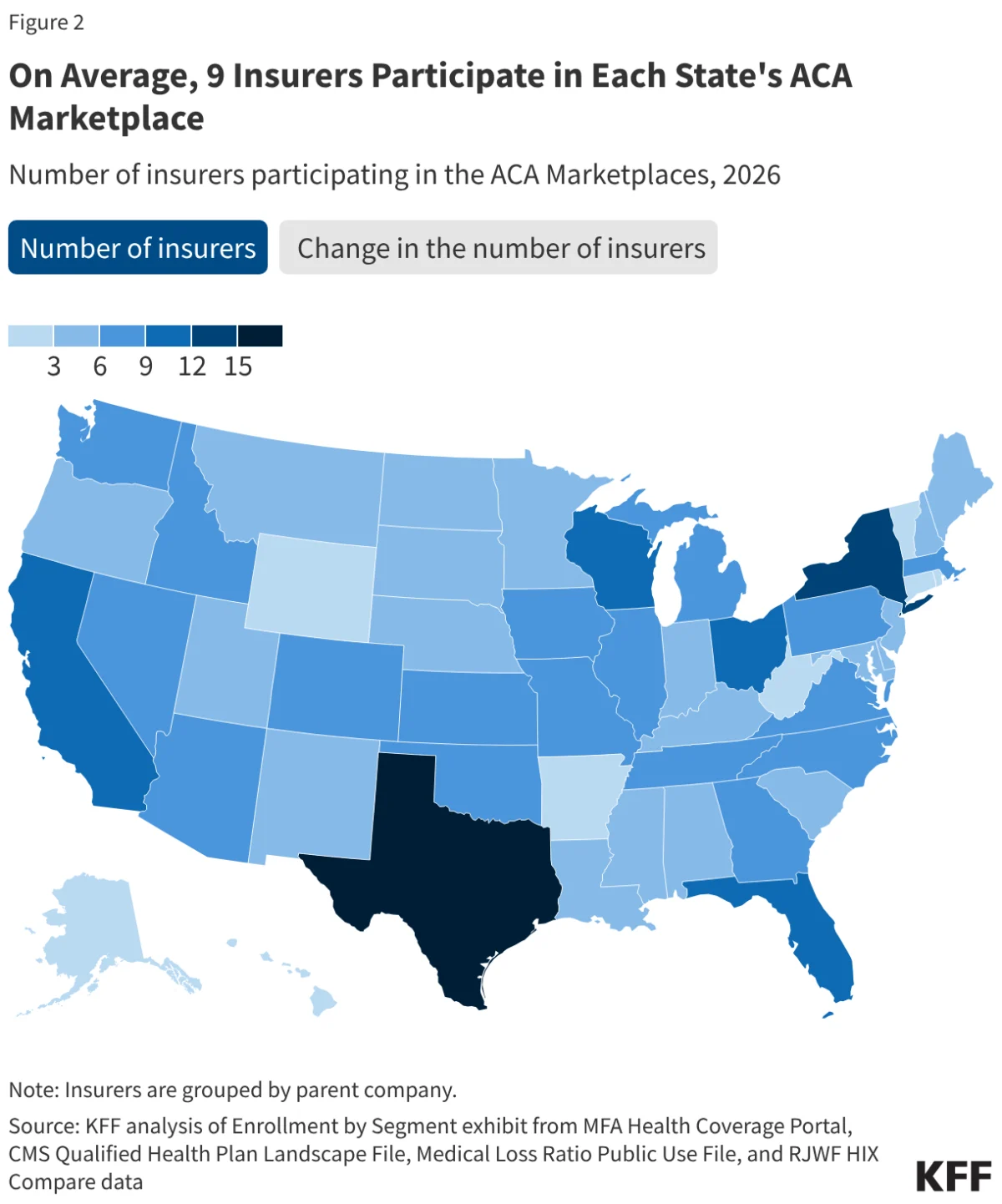

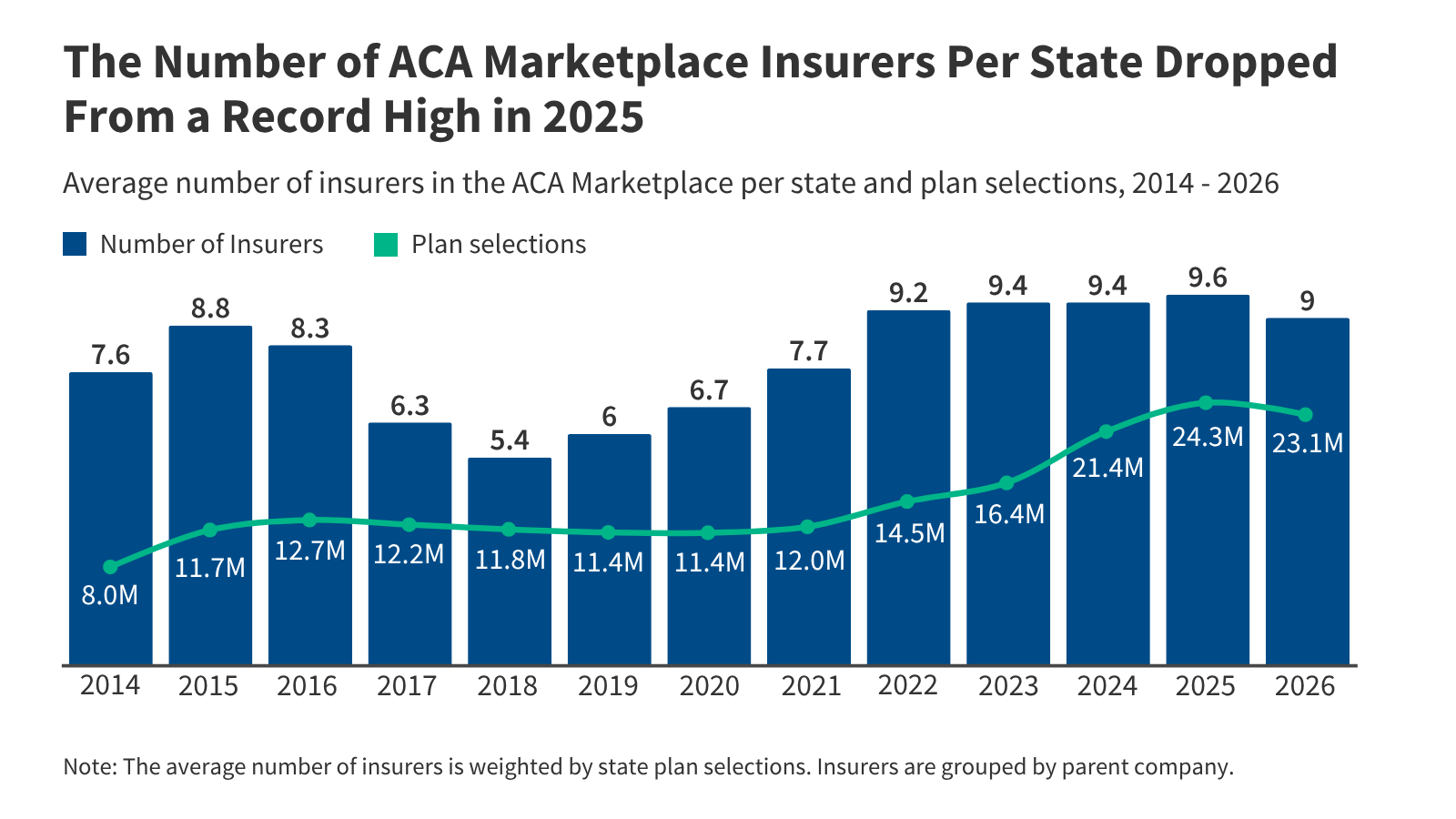

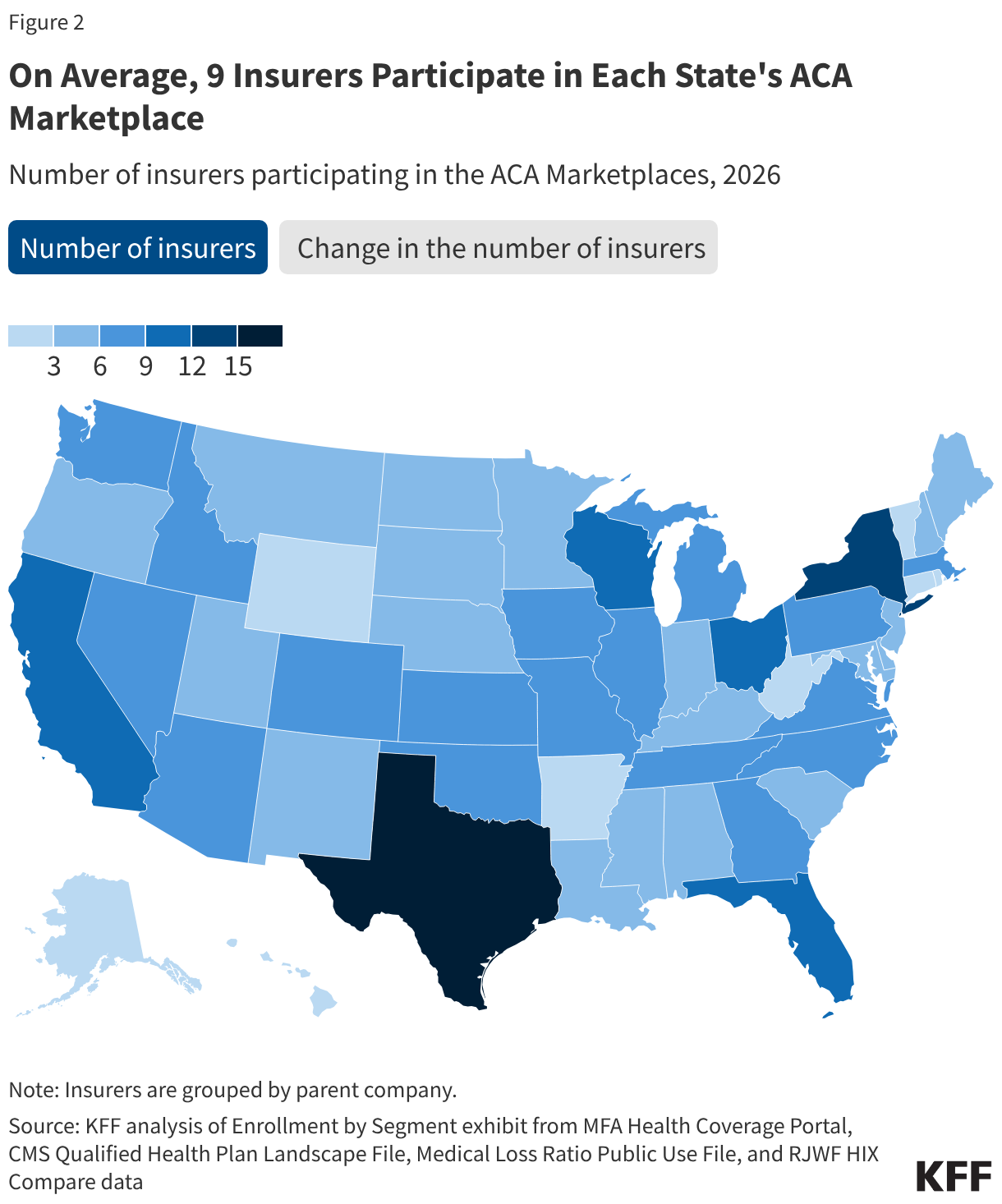

The national average for insurer participation in the ACA Marketplaces has dipped from a record high of 9.6 insurers per state in 2025 to 9.0 in 2026. This downward movement is not merely a statistical anomaly but a reflection of shifting market dynamics. The primary catalyst for this shift is the expiration of the enhanced premium tax credits, which had previously artificially inflated demand by making coverage exceptionally affordable for millions of Americans.

As these subsidies waned, the resulting decline in enrollment—estimated by KFF to reach approximately five million fewer people effectuating their coverage in 2026 compared to 2025—has forced insurance carriers to reassess the long-term viability of their participation. When the pool of potential enrollees shrinks, insurers often retreat to markets where they can achieve higher density and profitability. The departure of CVS Aetna stands as the most significant individual exit, but it is accompanied by a broader trend of carriers trimming their footprints in specific counties to shore up their risk pools.

Chronology: From Expansion to Retrenchment

To understand the current climate, one must view the ACA Marketplace through the lens of its turbulent history.

- 2017–2018 (The Volatility Era): The early years of the Trump administration saw significant instability. The 2017 exit of UnitedHealthcare from most states, followed by legislative attempts to repeal the ACA and the erosion of the individual mandate, caused a mass exodus of insurers. By 2018, the Marketplace had reached a low point in terms of competition, as carriers struggled to price plans against a backdrop of legislative uncertainty.

- 2019–2021 (The Stabilization Phase): During this period, the market found its footing. Insurers began to see the potential for consistent profitability, and many returned to the Exchanges.

- 2021–2025 (The Enhanced Subsidy Boom): The introduction of the American Rescue Plan’s enhanced premium tax credits served as a massive stimulus. Enrollment reached record highs, and insurers expanded their geographic footprints to capture this new, heavily subsidized customer base.

- 2026 (The Correction): With the expiration of those enhanced credits, the market is experiencing its first meaningful contraction since 2018. Insurers are now pruning their portfolios, as evidenced by the 18 states that saw a net decrease in the number of carriers offering plans this year.

Supporting Data: Regional and County-Level Analysis

The decline in participation is not uniform across the United States. While some states have maintained their competitive landscape, others have seen a stark reduction in consumer choice.

State-Level Divergence

Texas remains the most competitive state with 15 participating insurers, followed by New York, California, Florida, and Wisconsin, each boasting 11. Conversely, Illinois and Michigan have faced the steepest declines, each losing three carriers. Despite these exits, some states have seen minor growth; Alabama, Iowa, Louisiana, and Washington each saw a net increase of one insurer, proving that while the national trend is downward, niche opportunities for growth still exist for carriers like Oscar Health and Elevance Health (Wellpoint).

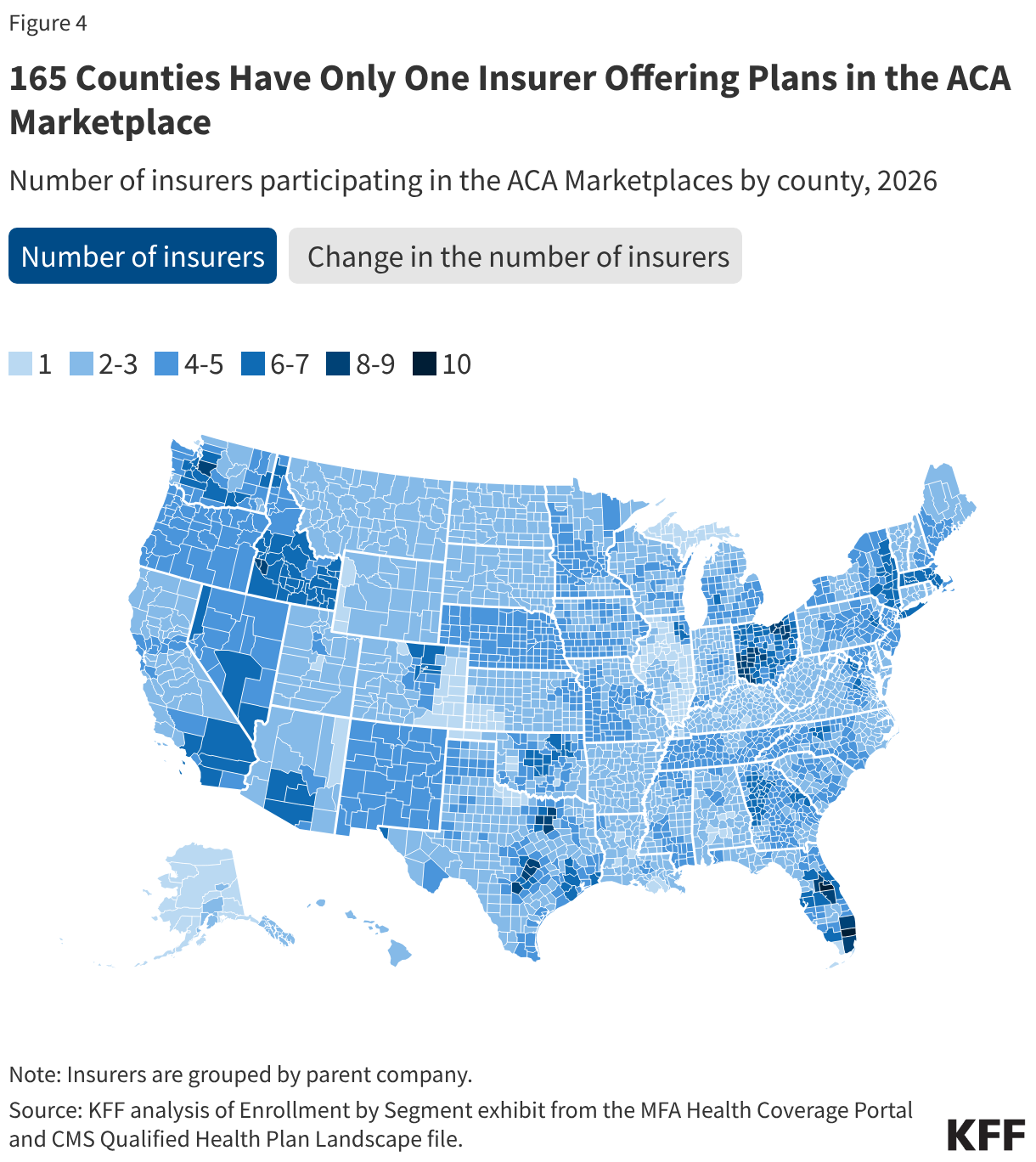

The County-Level "Desert"

The real impact of these changes is best observed at the county level. A carrier might remain in a state but pull out of specific rural or less profitable counties. For instance, UnitedHealth significantly scaled back its footprint in Kansas and South Carolina while simultaneously expanding in Oklahoma.

Perhaps most concerning for consumer advocates is the rise of the "single-insurer" county. In 2026, 165 counties are served by only one insurance provider. In 90 of these, the lack of competition is a direct result of insurers exiting the market for the new plan year. Furthermore, the lack of "bronze" plan availability in 490 counties—often where insurers have opted to provide only higher-premium silver or gold options—limits the ability of cost-conscious consumers to find affordable coverage, further complicating the accessibility of the ACA.

Official Responses and Strategic Implications

The implications for the healthcare industry are profound. Insurers are no longer operating in an environment where they can rely on government-fueled enrollment growth. Instead, they are reverting to traditional actuarial strategies: monitoring the risk pool, assessing the health of the population in specific regions, and exiting markets where the cost of care exceeds the premiums they can charge.

Major players like Centene and UnitedHealth continue to dominate the market, holding significant portions of the individual market share. However, the data suggests that these giants are becoming increasingly selective. When healthier-than-average enrollees drop coverage, the risk pool worsens, forcing insurers to raise premiums to cover the costs of the remaining, sicker population. This creates a "death spiral" dynamic that regulators are now watching closely to prevent.

The KFF Insurer Participation Tracker, which monitors early announcements for the 2027 plan year, suggests that the contraction may not be a one-time event. Several insurers have already signaled their intent to depart from additional markets, indicating that the industry is bracing for a period of sustained volatility.

Implications for Consumers and Policymakers

The primary casualty of this contraction is consumer choice. In a market where competition is essential to keeping premiums low and benefit packages robust, the loss of three carriers in a single state can lead to significant premium hikes and reduced network access for residents.

For policymakers, the challenge is clear: the ACA Marketplace was designed to be self-sustaining, but it has become increasingly dependent on the artificial demand generated by subsidies. The 2026 data serves as a warning that without long-term, stable federal support, the Marketplace is susceptible to the same boom-and-bust cycles that plagued the individual health insurance market prior to 2010.

As we move toward the 2027 enrollment cycle, all eyes will be on whether the remaining carriers can stabilize the market or if further exits will continue to erode the progress made over the last five years. The goal for state insurance commissioners and federal regulators will be to incentivize competition in the 165 counties currently served by only one provider, ensuring that the promise of the ACA—affordable, accessible coverage—does not vanish along with the enhanced subsidies.

The era of unchecked expansion is over; the era of market discipline has arrived. Whether this transition leads to a more efficient system or a fractured one remains the defining question for the future of American health insurance.