For millions of older Americans and people with disabilities, the promise of Medicare is anchored in the ability to access affordable prescription drugs. For those enrolled in "Traditional Medicare"—nearly half of all beneficiaries—that access is primarily provided through stand-alone Prescription Drug Plans (PDPs). However, a seismic shift is underway in the Medicare marketplace. As Medicare Advantage Prescription Drug plans (MA-PDs) gain an increasingly dominant competitive edge, the stand-alone market is contracting, leaving traditional Medicare enrollees facing higher premiums, fewer choices, and growing uncertainty.

The Core Conflict: An Uneven Playing Field

At the heart of this instability lies a structural imbalance in how the federal government pays for drug coverage. The Medicare Advantage (MA) payment system is designed with a unique mechanism: when an insurer’s cost of providing medical services (Part A and Part B) is lower than the benchmark payment set by the federal government, the insurer retains a portion of the difference as a "rebate."

These rebates are not merely corporate profits; they are effectively public subsidies that insurers must use to reduce premiums or offer supplemental benefits. Increasingly, MA-PD sponsors are funneling these billions of dollars into their drug benefit programs. By "buying down" Part D premiums, they can offer plans that appear to be premium-free or significantly cheaper to the average beneficiary.

Conversely, sponsors of stand-alone PDPs receive no such rebates. Without the ability to cross-subsidize their drug plans with medical-side surplus payments, PDP sponsors are forced to compete on a purely cost-recovery basis. This dynamic has been exacerbated by the 2024–2025 redesign of the Part D benefit under the Inflation Reduction Act (IRA), which shifted more financial risk onto plan sponsors, further squeezing their margins and forcing premium hikes.

A Chronology of Market Contraction

The erosion of the PDP market has been a gradual, yet accelerating, phenomenon over the last half-decade.

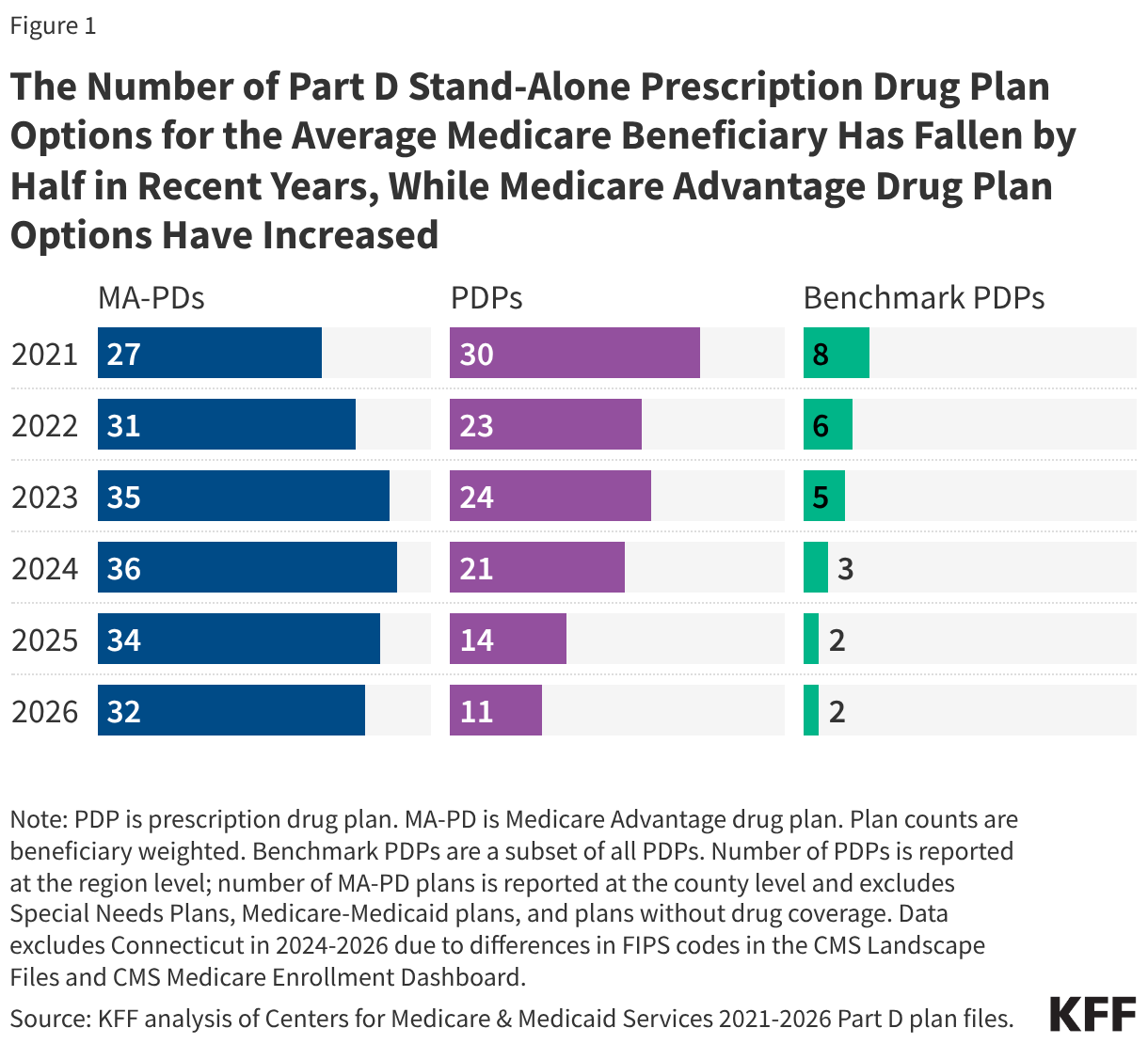

- 2021: A Competitive Landscape: Five years ago, the average Medicare beneficiary had access to 30 different stand-alone PDPs. For those qualifying for the Low-Income Subsidy (LIS), there were an average of eight "benchmark" plans—options that required no monthly premium.

- 2024: The Turning Point: The implementation of the Inflation Reduction Act’s Part D benefit redesign—including a new out-of-pocket spending cap—created significant cost pressures for all plans. To prevent a catastrophic spike in premiums, the federal government launched the voluntary "Premium Stabilization Demonstration."

- 2025: Heightened Volatility: As the full weight of the IRA changes took hold, the Centers for Medicare & Medicaid Services (CMS) reported significant variation in plan bids. The government increased its intervention, providing $6.2 billion in subsidies to PDPs to keep the market afloat.

- 2026: The Current Crisis: The number of available PDPs for the average beneficiary has plummeted to just 11. Meanwhile, the number of benchmark plans for low-income beneficiaries has dwindled to only two. In contrast, the MA-PD market has remained robust, with the average beneficiary now having 32 different plan options.

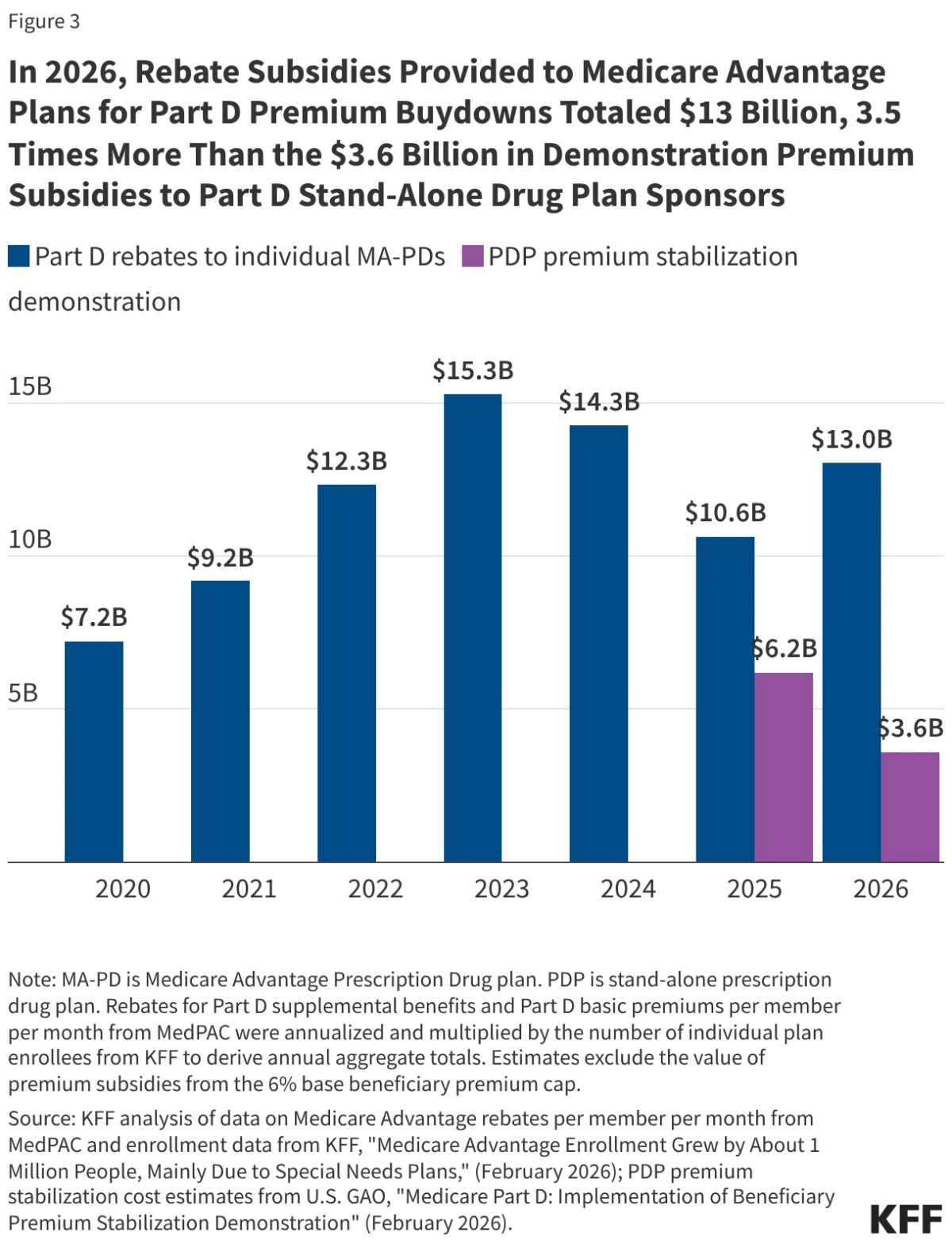

Supporting Data: The Cost of Disparity

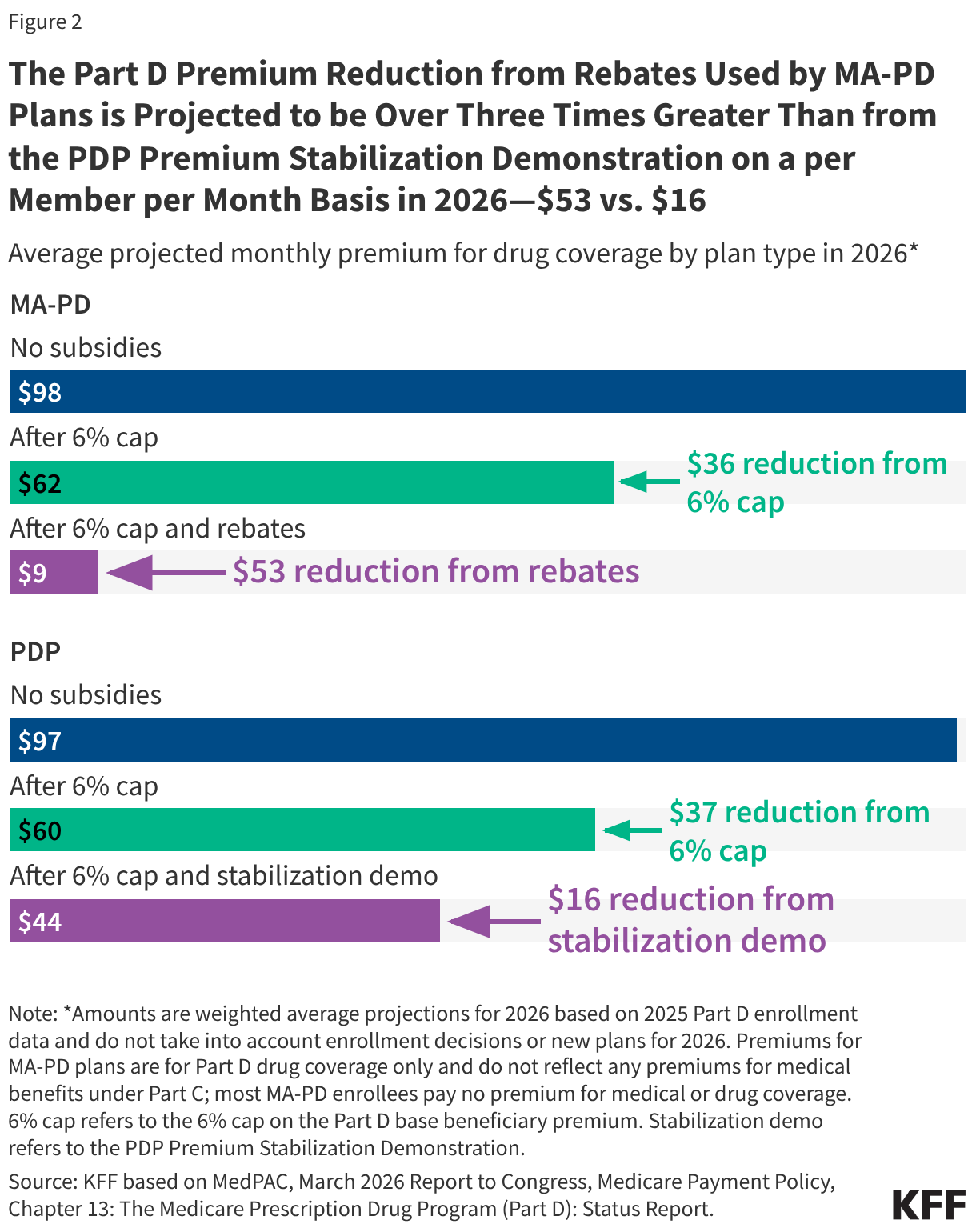

The financial chasm between the two markets is best illustrated by the data regarding federal support. In 2026, the federal government is projected to provide $13 billion in rebate-funded subsidies to MA-PDs, equating to roughly $53 per member per month (PMPM).

By comparison, the government’s efforts to stabilize the PDP market through the temporary demonstration project provide only $3.6 billion in total subsidies, or roughly $16 PMPM.

Key Comparative Metrics (2026 Projections)

- Average Monthly Premium (MA-PD): $9 (after accounting for all subsidies).

- Average Monthly Premium (PDP): $44 (after accounting for all subsidies).

- Percentage of Non-LIS Enrollees with $0 Premiums: 79% for MA-PDs vs. 28% for PDPs.

- Total Federal Subsidy Impact: MA-PD rebate buydowns are over three times more impactful on a per-member basis than the PDP stabilization demonstration.

Without these government interventions—specifically the 6% base beneficiary premium cap and the targeted stabilization funds—the average monthly premiums for both plan types would likely be on par. The subsidies essentially act as a thumb on the scale, heavily favoring the Medicare Advantage model.

Official Responses and Regulatory Maneuvers

The federal government has acknowledged the fragility of the stand-alone market, yet its response has been bifurcated. Through the CMS Innovation Center, the government has used Section 402 demonstration authority to prop up the PDP market. However, these are temporary measures.

The decision by the current administration to reduce the level of premium subsidies in the second year of the demonstration (2026) reflects an ongoing tension between controlling federal spending and maintaining market stability. While proponents of the Medicare Advantage model argue that the rebate system promotes efficiency and integrated care, critics—including representatives from the traditional Medicare advocacy community—contend that the current system effectively penalizes beneficiaries who prefer the provider freedom of traditional Medicare.

The Medicare Payment Advisory Commission (MedPAC) has consistently highlighted this disparity in its reports to Congress, noting that the "premium advantage" for MA-PDs is a direct result of the payment formula rather than inherent operational efficiencies in drug management.

Implications: The Future of Traditional Medicare

The long-term implications of this market shift are profound. As PDP options vanish, beneficiaries in traditional Medicare are increasingly forced into a corner. They must choose between paying significantly higher out-of-pocket premiums for the privilege of keeping their traditional coverage or switching to a Medicare Advantage plan.

1. The Rural Access Crisis

Rural residents are the most vulnerable to these trends. They are statistically more likely to rely on traditional Medicare and, by extension, rely heavily on stand-alone drug plans. As PDP sponsors withdraw from rural markets due to low profitability, these beneficiaries are left with the fewest choices, potentially leading to "coverage deserts" where only one or two expensive plans remain.

2. The Trade-offs of "Free" Coverage

While the zero-premium MA-PD plans are attractive, they come with strings attached that are not present in traditional Medicare. MA plans frequently utilize restrictive provider networks and aggressive prior authorization requirements. For patients with complex, chronic conditions, the "cheaper" premium may ultimately lead to higher hurdles in accessing specialized care or specific medications.

3. The Erosion of Choice

The shrinking number of PDPs limits the ability of consumers to "shop" for the best coverage for their specific medication regimen. When only a handful of plans are available, the probability that a beneficiary can find a plan that covers all their medications at a reasonable cost decreases significantly.

Conclusion: A System at a Crossroads

The Medicare Part D program was founded on the principle of choice and market competition. However, the current trajectory suggests that competition is being replaced by consolidation. By allowing the payment system to favor one model of coverage so heavily, the federal government is effectively nudging millions of Americans toward Medicare Advantage—not necessarily because it is the superior choice for every individual, but because the alternative is being rendered financially unsustainable.

Moving forward, policymakers face a difficult dilemma: continue to provide increasingly expensive, temporary "band-aid" subsidies to keep the stand-alone market alive, or reform the Medicare Advantage payment system to create a truly level playing field. Without such structural intervention, the decline of the stand-alone PDP market may well signal the beginning of the end for the independence of the traditional Medicare program. As it stands, the "premium advantage" enjoyed by MA-PDs is not just a market quirk; it is a policy-driven outcome that is fundamentally reshaping the landscape of American healthcare for the elderly.