The Medicare Part D program, a cornerstone of the American healthcare safety net, continues to evolve as it enters 2026. Serving 56 million older adults and individuals with long-term disabilities, the program is currently navigating a complex period of structural redesign, shifting enrollment patterns, and rising out-of-pocket cost pressures. As the program adapts to the mandates of the Inflation Reduction Act (IRA), recent data from the Centers for Medicare & Medicaid Services (CMS) reveals a landscape where the divide between stand-alone prescription drug plans (PDPs) and Medicare Advantage (MA-PDs) is widening, particularly regarding affordability and access.

The State of Enrollment: A Tale of Two Plans

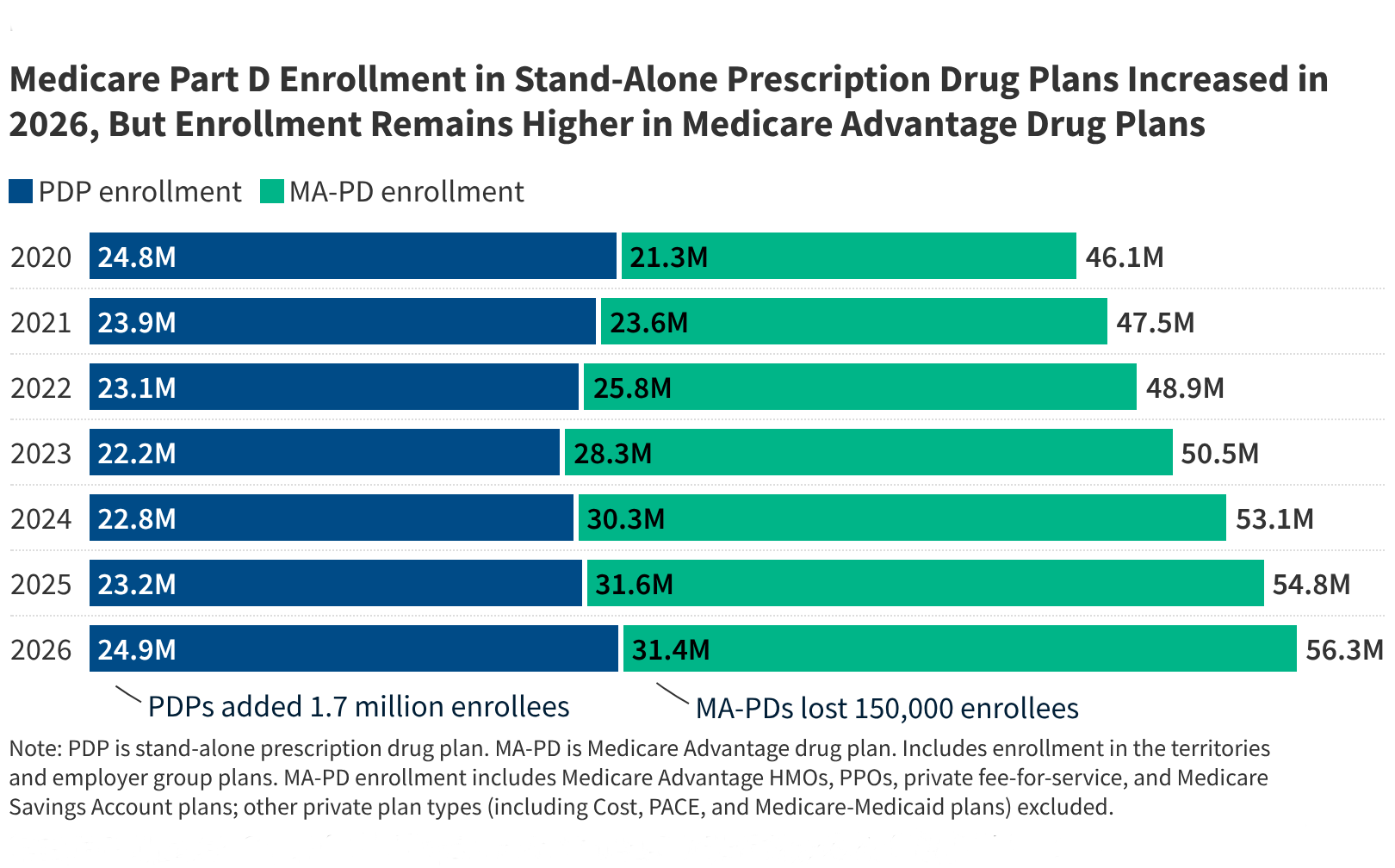

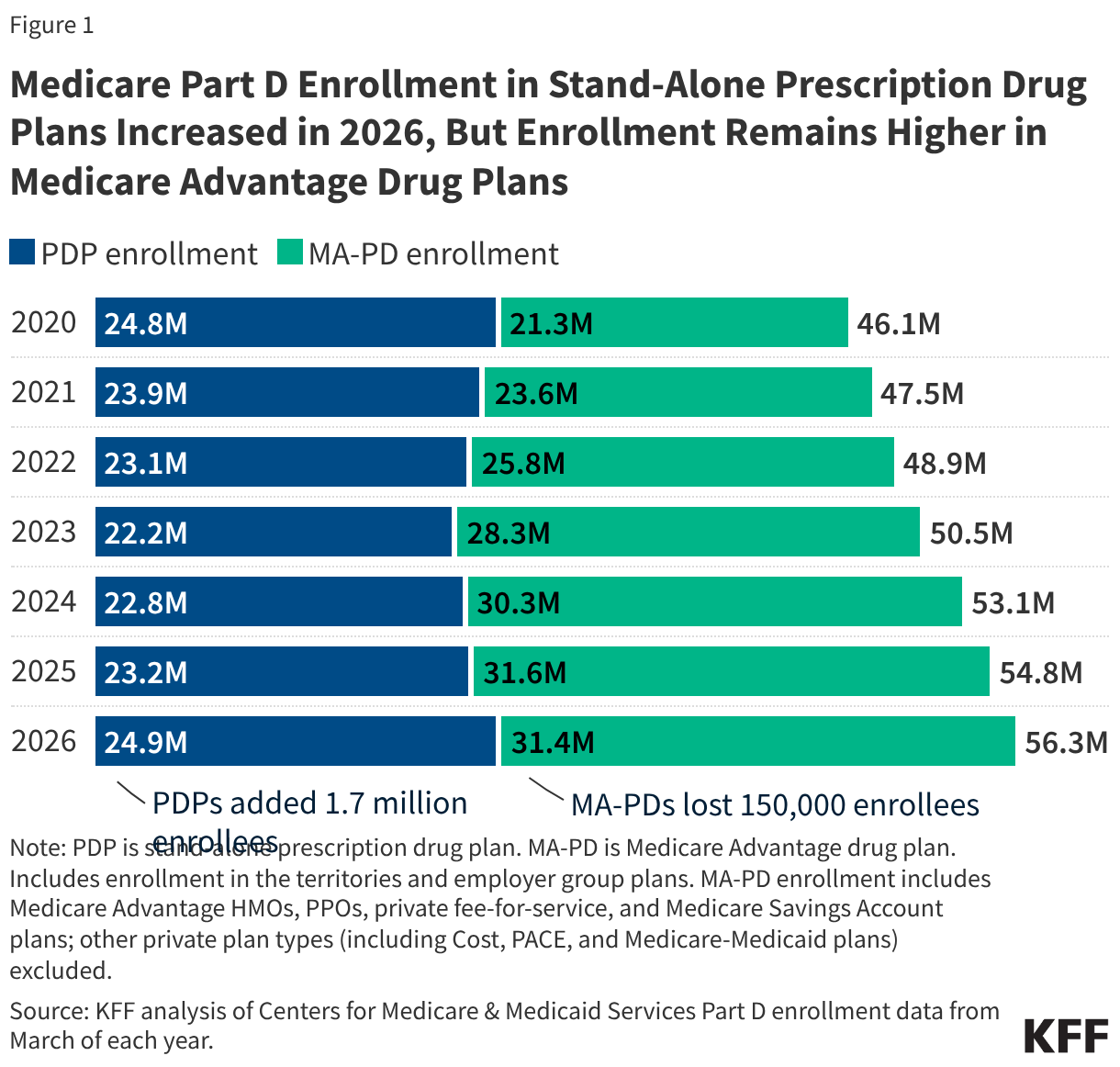

As of 2026, the Medicare Part D ecosystem remains heavily tilted toward integrated coverage. More than half (56%) of all Part D enrollees are now housed within Medicare Advantage plans. This reflects a multi-year trend where beneficiaries increasingly prefer the "all-in-one" model of Medicare Advantage, which combines medical benefits with drug coverage.

However, the stand-alone Prescription Drug Plan (PDP) market has shown unexpected resilience. For the third consecutive year, the number of PDP enrollees has grown, climbing by 1.7 million since 2025. Much of this growth is attributed to employer-group PDPs, as corporations adjust their benefit structures to better manage rising costs.

A notable shift occurred in the total enrollment for Medicare Advantage Prescription Drug plans (MA-PDs), which saw a modest contraction, dropping from 31.6 million to 31.4 million. Industry analysts suggest this is not a decline in interest in Medicare Advantage itself, but rather a tactical shift. Many employer groups are moving enrollees from integrated MA-PD plans toward MA-only plans paired with separate, stand-alone drug coverage, likely to optimize administrative costs and plan performance metrics.

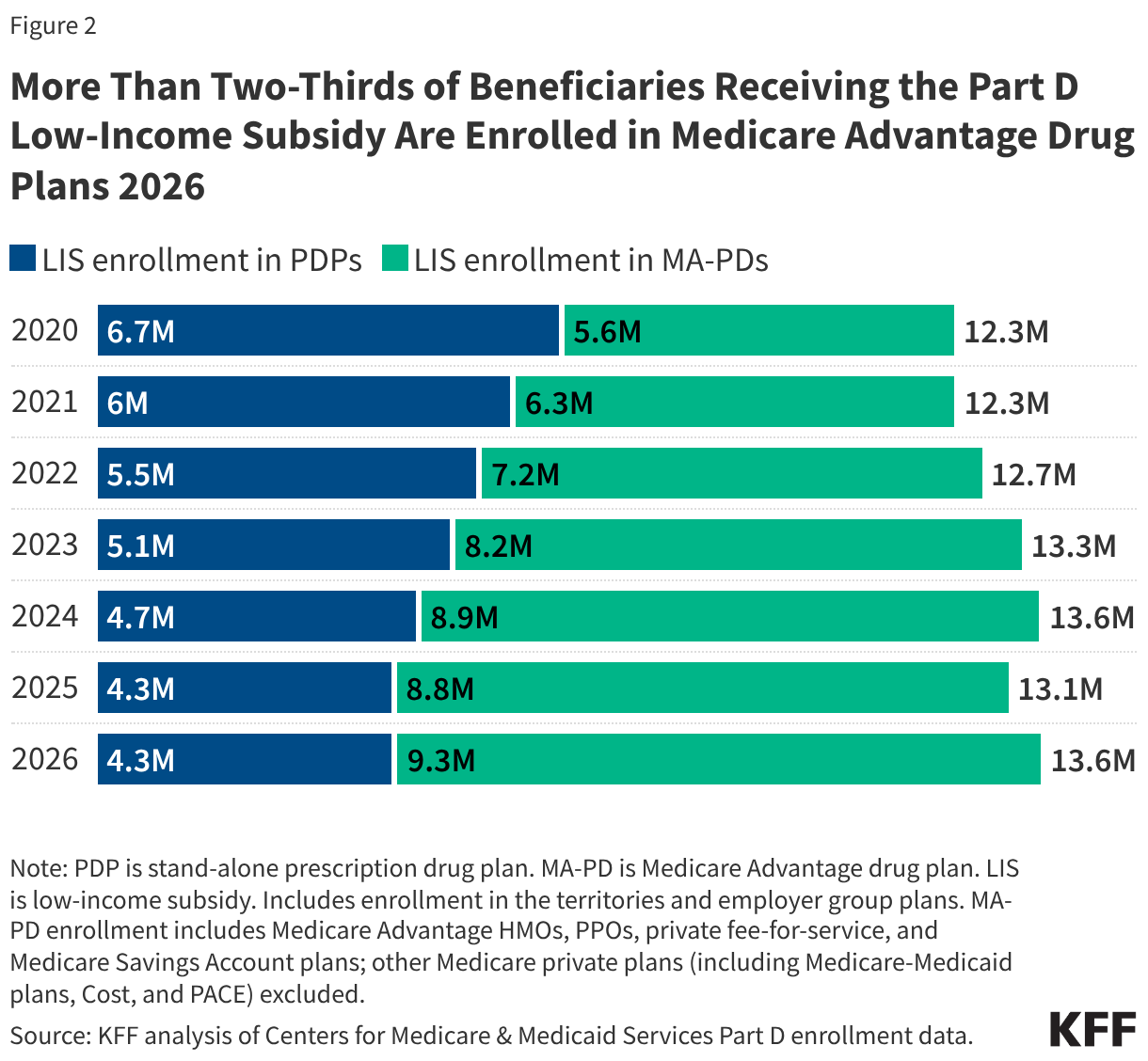

The Vulnerability of Low-Income Subsidy (LIS) Beneficiaries

The Low-Income Subsidy (LIS) program, which provides essential financial aid for premiums and cost-sharing, covers 13.6 million beneficiaries. In 2026, enrollment in this program grew by 500,000, partially rebounding from a dip in 2025. The previous year’s decline was largely tied to the "unwinding" of Medicaid continuous enrollment provisions, which followed the end of the COVID-19 public health emergency. Because dual-eligible individuals automatically qualify for LIS, the loss of Medicaid coverage often triggered an unintended loss of Part D subsidies. While the program is stabilizing, the reliance of these vulnerable populations on Medicare Advantage Special Needs Plans (SNPs) remains absolute, with nearly half of all LIS enrollees (6.7 million) residing in these specialized, coordinated-care plans.

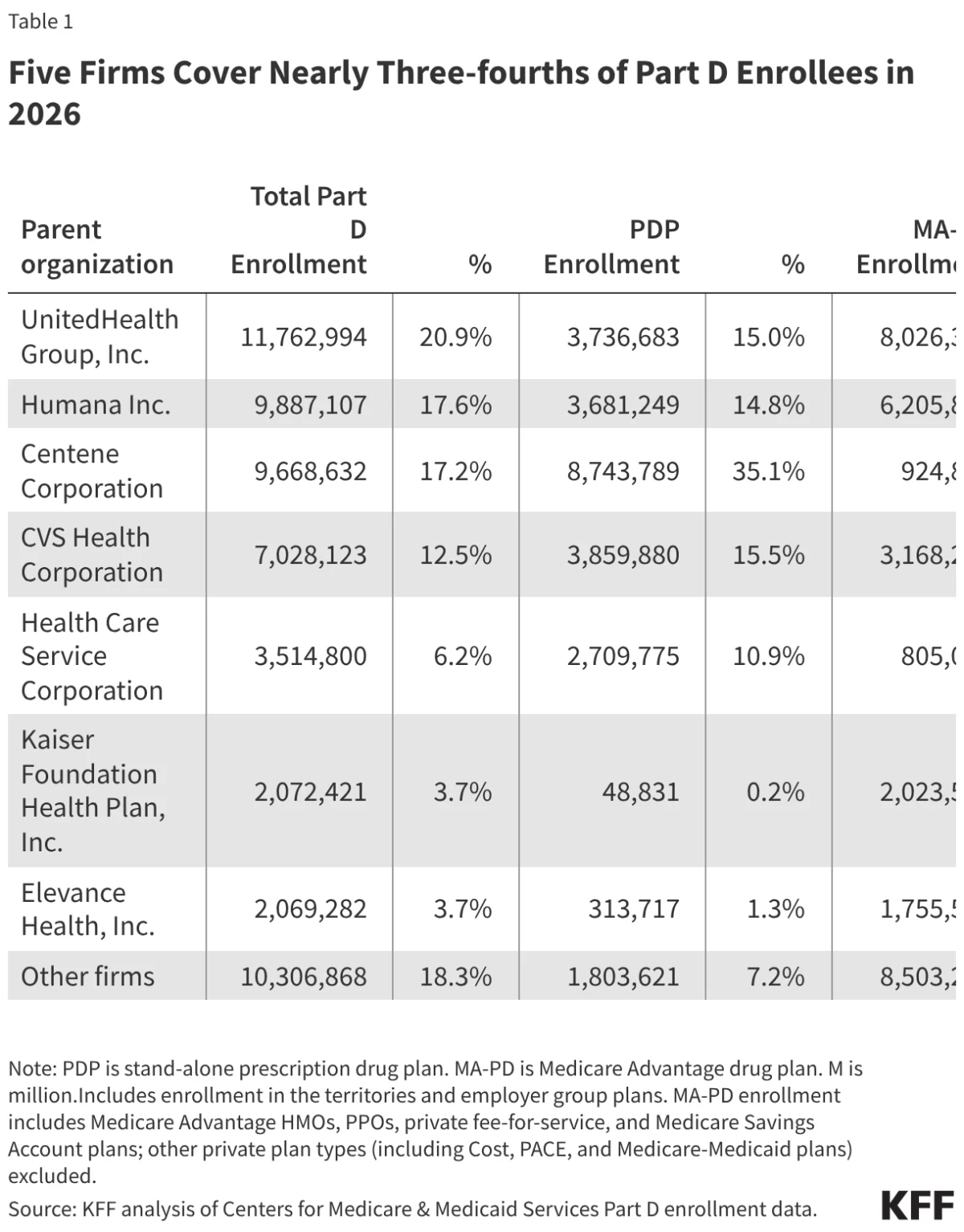

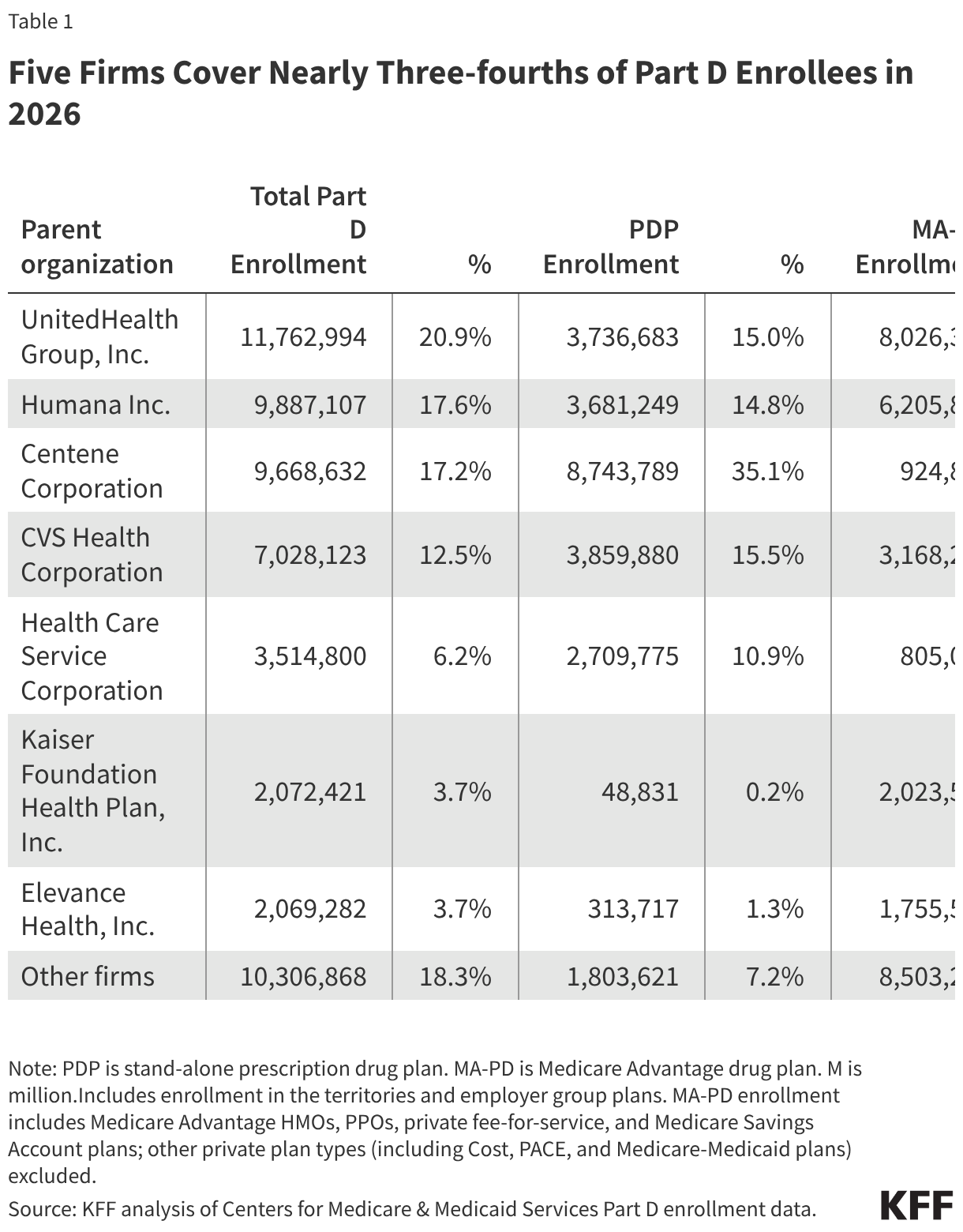

Market Concentration: The Power of Five

The Part D market is characterized by extreme consolidation. In 2026, just five firms—UnitedHealth, Humana, Centene, CVS Health, and their peers—account for 74% of all Part D enrollees, totaling 41.9 million people.

UnitedHealth leads the pack, serving one in five enrollees (11.8 million) across its various product lines. The market segments are distinct: Centene dominates the stand-alone PDP market with over one-third of that sector’s membership, while UnitedHealth maintains its grip on the MA-PD market with 26% of that segment’s share. This concentration raises long-term questions regarding market competition and the ability of smaller insurers to maintain viability against these massive, diversified conglomerates.

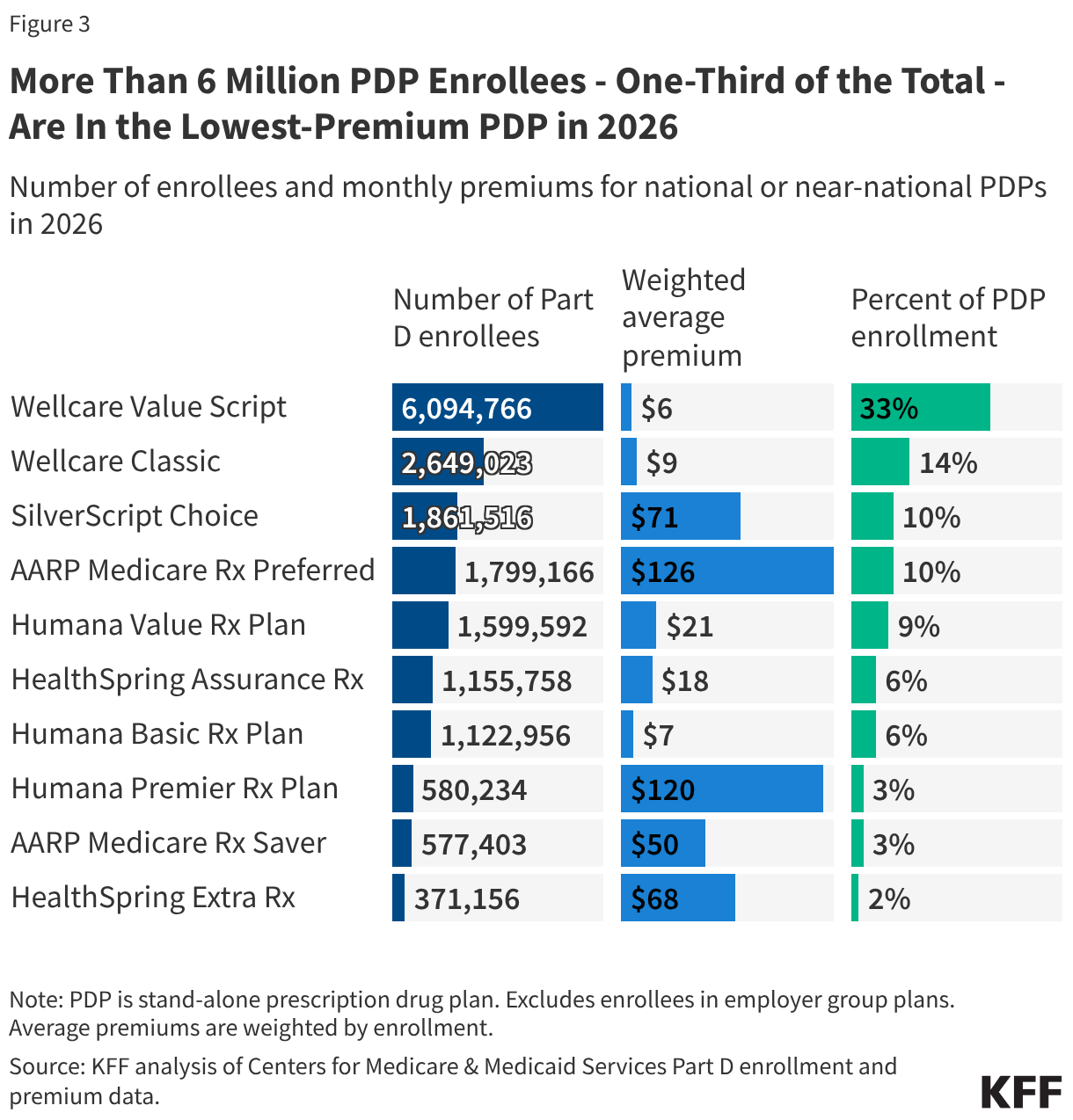

Financial Dynamics and the "Lowest-Premium" Trap

A significant portion of the population is highly sensitive to monthly premiums. In 2026, over 6 million PDP enrollees—one-third of the total—have flocked to the "Wellcare Value Script" plan, which boasts a monthly premium of less than $6.

This behavior highlights a potential disconnect in consumer literacy: while these plans offer the lowest monthly premiums, they are often "enhanced" plans that do not qualify as benchmark plans for LIS beneficiaries. Consequently, LIS enrollees who choose these plans—or are defaulted into them—may face higher total costs in the long run. Only 3% of the 6.1 million enrollees in this popular plan are LIS recipients, proving that the lowest-premium option is often a strategic choice for non-subsidized individuals rather than a catch-all solution for the most vulnerable.

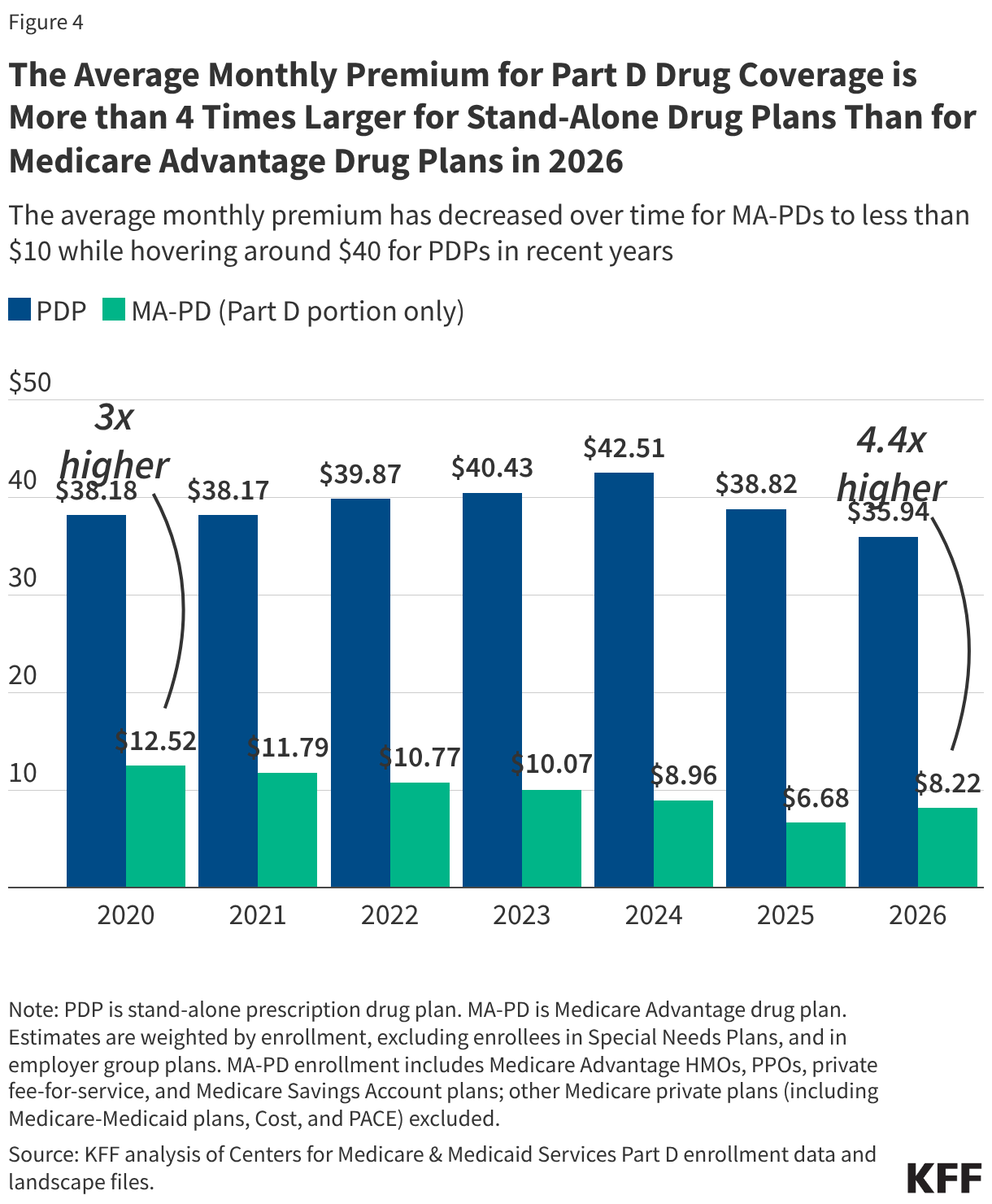

Part D Premiums: The Stabilization Demonstration

The Biden administration’s premium stabilization demonstration, extended by the Trump administration for 2025, has played a critical role in tempering the volatility of PDP premiums. Without this intervention, premium spikes would have been significantly more severe. As it stands, the average monthly PDP premium dropped by 7%, from $39 to $36.

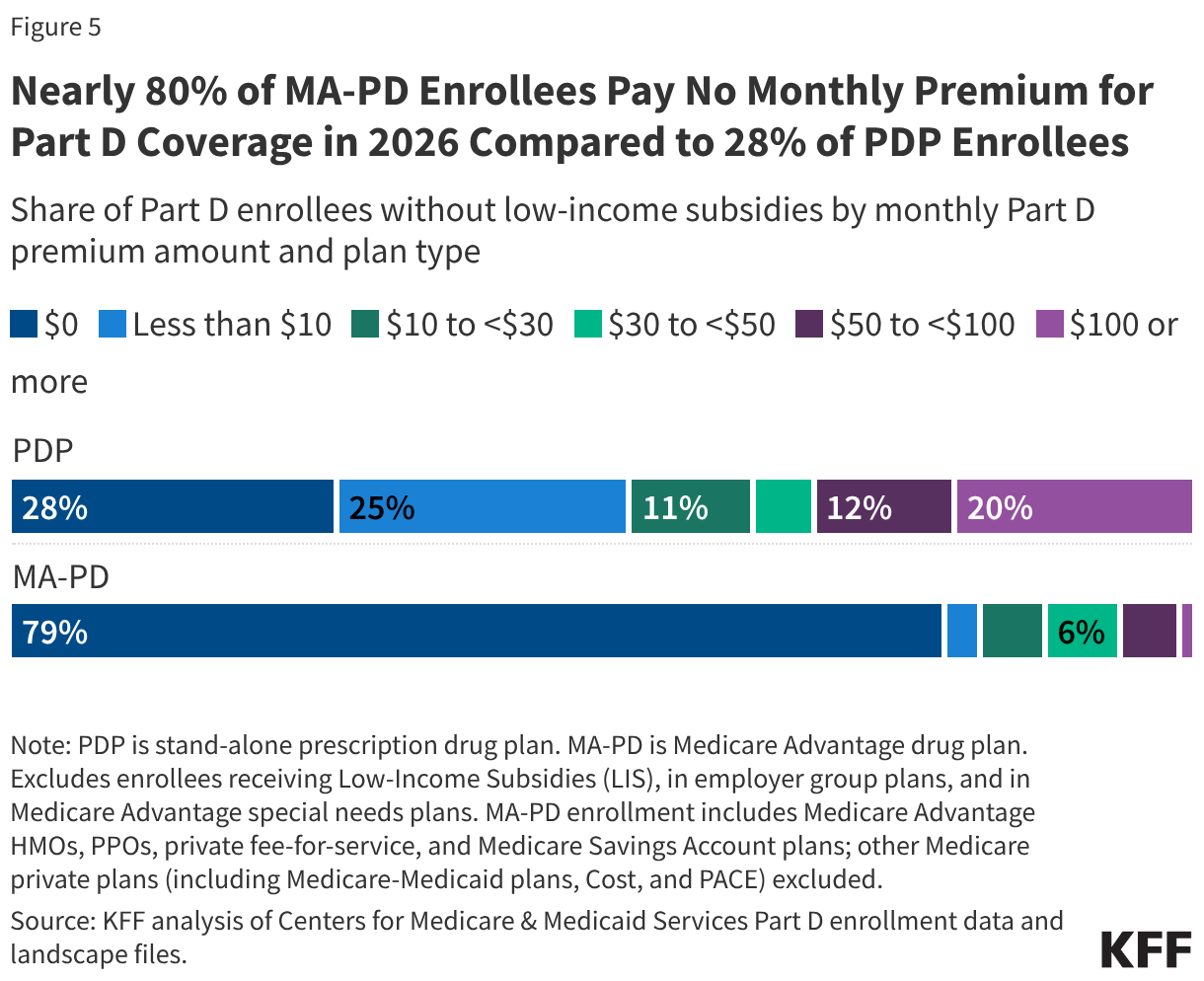

Despite this decline, a chasm remains between PDPs and MA-PDs. The average monthly premium for drug coverage in an MA-PD plan is just $8, compared to $36 for a stand-alone PDP. This disparity is largely fueled by the "rebate" system. Medicare Advantage sponsors use federal rebate dollars—which have tripled since 2015 and now exceed $2,600 per beneficiary—to buy down drug premiums to zero. For the average Medicare beneficiary, 21 out of 32 available MA-PD options currently charge no monthly premium for drug coverage, a stark contrast to the PDP market where only 2 of 11 options are zero-premium.

The Rising Tide of Out-of-Pocket Costs

Perhaps the most concerning trend for 2026 is the rapid escalation of cost-sharing requirements. Under the redesigned Part D benefit architecture, plans are increasingly shifting the financial burden onto enrollees through higher deductibles and a transition from fixed-dollar copayments to percentage-based coinsurance.

The Deductible Surge

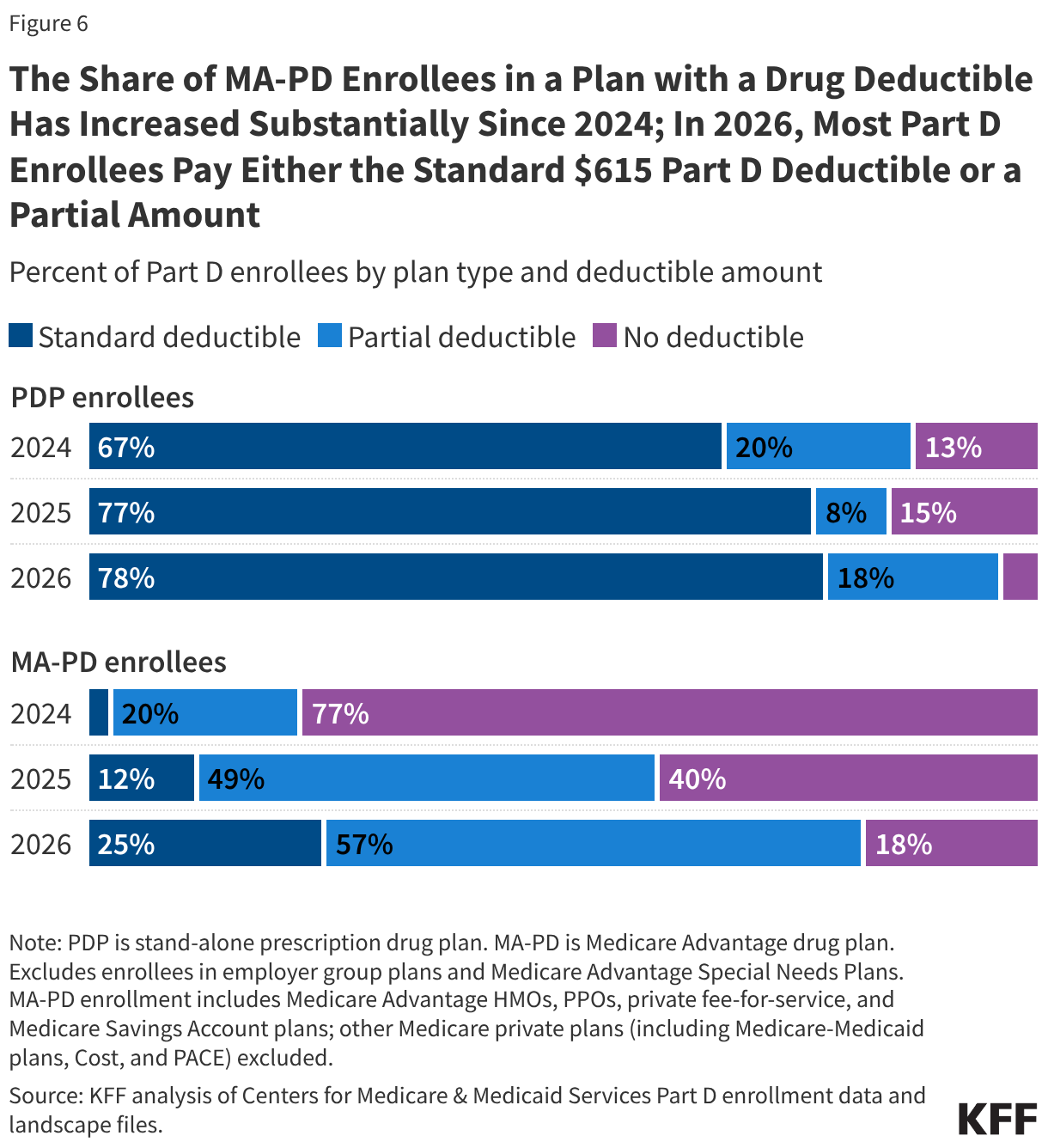

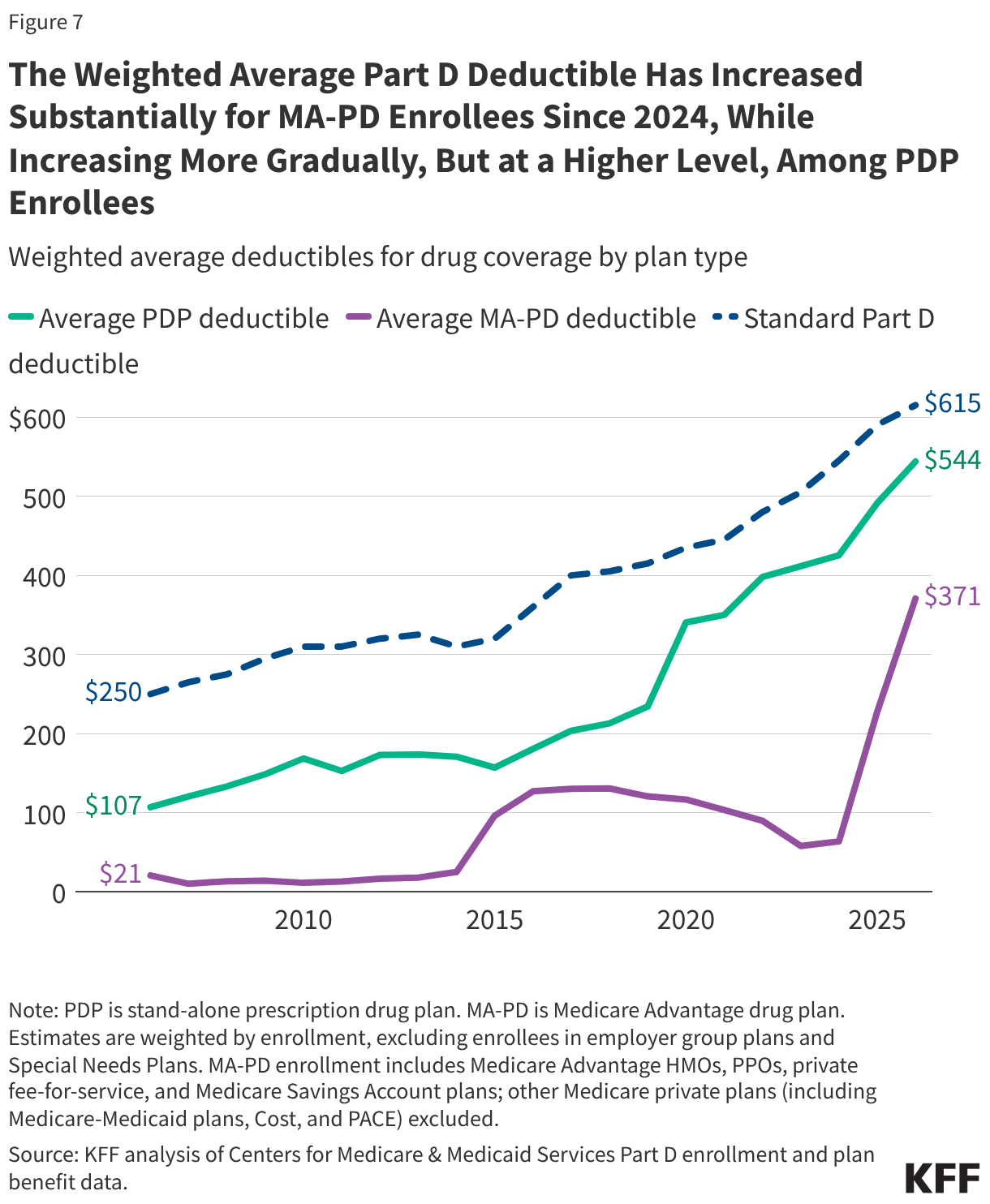

The days of widespread "no-deductible" plans are effectively ending. In 2026, 82% of MA-PD enrollees are in plans that require a drug deductible, a massive leap from just 23% in 2024. The average deductible for MA-PD enrollees has skyrocketed by 481% in two years, reaching $371.

PDP enrollees have fared little better. Nearly all PDP enrollees (96%) now face a deductible, with the average sitting at $544. This reflects a structural shift: as plan sponsors grapple with the IRA’s new cap on out-of-pocket costs ($2,100 in 2026), they are aggressively increasing deductibles to protect their own bottom lines.

Coinsurance vs. Copayments

The transition from simple copayments to complex coinsurance—where the patient pays a percentage of the drug’s price—is making it increasingly difficult for beneficiaries to predict their pharmacy bills. For preferred brands, 97% of PDP enrollees now face coinsurance, with a median rate of 25%. For non-preferred drugs, the shift to coinsurance is near-universal, with median rates reaching as high as 50% in some plans.

Official Responses and Industry Implications

The Centers for Medicare & Medicaid Services (CMS) maintains that the redesign of the Part D benefit—specifically the $2,100 out-of-pocket cap—is a historic win for consumers. By eliminating the "catastrophic" coverage gap, the federal government aims to protect patients with chronic, high-cost conditions from financial ruin.

However, industry groups, including the Pharmaceutical Care Management Association (PCMA), have cautioned that the redesign forces plans to rebalance their risk profiles. "We are seeing the expected market response to higher actuarial risk," noted one industry analyst. "When you cap the patient’s liability at $2,100, the plan must find ways to manage the front-end costs, which leads to higher deductibles and broader application of coinsurance."

Long-term Implications for Beneficiaries

The 2026 data indicates a transition toward a more complex, high-deductible environment for Medicare drug coverage. Beneficiaries are facing a trade-off: they are protected from unlimited catastrophic expenses, but they are paying more for their day-to-day prescriptions through deductibles and coinsurance.

For the average senior, the advice from advocates is clear: "Don’t shop on premiums alone." The allure of a $0 premium MA-PD plan or a $6 PDP premium can be deceptive. Beneficiaries must now scrutinize the "fine print"—the deductible, the coinsurance rates on their specific maintenance medications, and the formulary tiers. As the Part D market continues to consolidate and cost-sharing models become more aggressive, the burden of navigating this complexity is shifting squarely onto the shoulders of the consumer.

As we look toward 2027 and beyond, the success of the Part D program will likely depend on whether the federal government can curb these front-end cost increases without undermining the very stability the premium stabilization programs were designed to protect.