As the federal government continues to shift the landscape of senior healthcare, Medicare Advantage (MA) remains the dominant alternative to traditional Medicare. In 2026, the program continues to evolve, balancing the allure of zero-premium plans and supplemental perks against the administrative friction of prior authorization and restricted provider networks. This analysis, based on recent data from the Kaiser Family Foundation (KFF) and the Medicare Payment Advisory Commission (MedPAC), examines the fiscal and structural realities facing millions of beneficiaries.

Main Facts: The Economic Engine of Medicare Advantage

At its core, Medicare Advantage is a private-sector delivery model for public benefits. The federal government contracts with private insurers to manage the care of Medicare enrollees, paying these companies a monthly, risk-adjusted fee per person. These payments are determined by a complex formula that accounts for the enrollee’s county of residence, health status (risk scores), the plan’s quality star rating, and estimated costs for Part A and Part B services.

In 2026, the financial incentive for insurers to participate in the program is at an all-time high. According to MedPAC, private plans are expected to receive an average of $2,664 per enrollee above their estimated costs for providing core Medicare services. This surplus, known as a "rebate," has more than doubled since 2018. Insurers utilize these funds to subsidize supplemental benefits—such as dental, vision, and hearing coverage—and to drive down premiums, making the plans highly attractive to the average consumer.

Chronology: A Decade of Shifting Costs and Benefits

The trajectory of Medicare Advantage over the last decade has been defined by a steady decline in supplemental premiums, interrupted only recently by minor fluctuations.

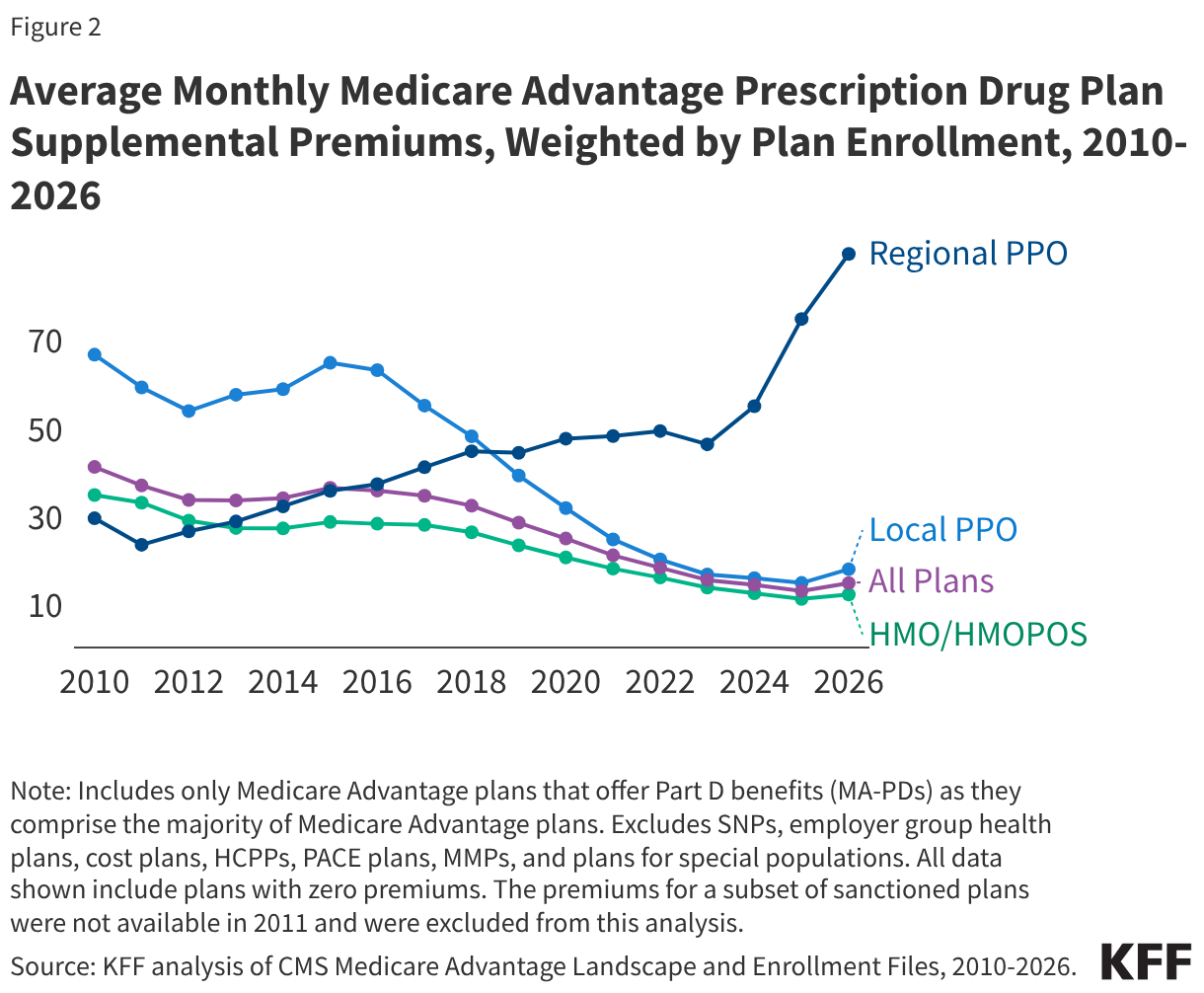

- 2015–2025: During this period, the average supplemental premium for Medicare Advantage Prescription Drug plans (MA-PDs) fell from $36 per month to a low of $13. This trend was fueled by the rapid growth of rebates, which allowed insurers to lower consumer costs aggressively.

- 2026: The trend saw a slight reversal, with average supplemental premiums ticking up to $15 per month. While this remains historically low, it marks a pivot point as insurers face pressure from regulatory changes and rising medical costs.

- The HMO/PPO Dynamic: Over the last ten years, the market has shifted toward HMOs and local PPOs. These plans, which now account for the vast majority of enrollment, have been the primary drivers of premium reductions. However, regional PPOs have bucked this trend, with premiums rising from $36 in 2015 to $89 in 2026, reflecting their niche status and higher operational overhead.

Supporting Data: Where the Money Goes

The financial profile of a 2026 Medicare Advantage plan is characterized by high availability of "extras" and strict financial caps.

Premiums and Rebates

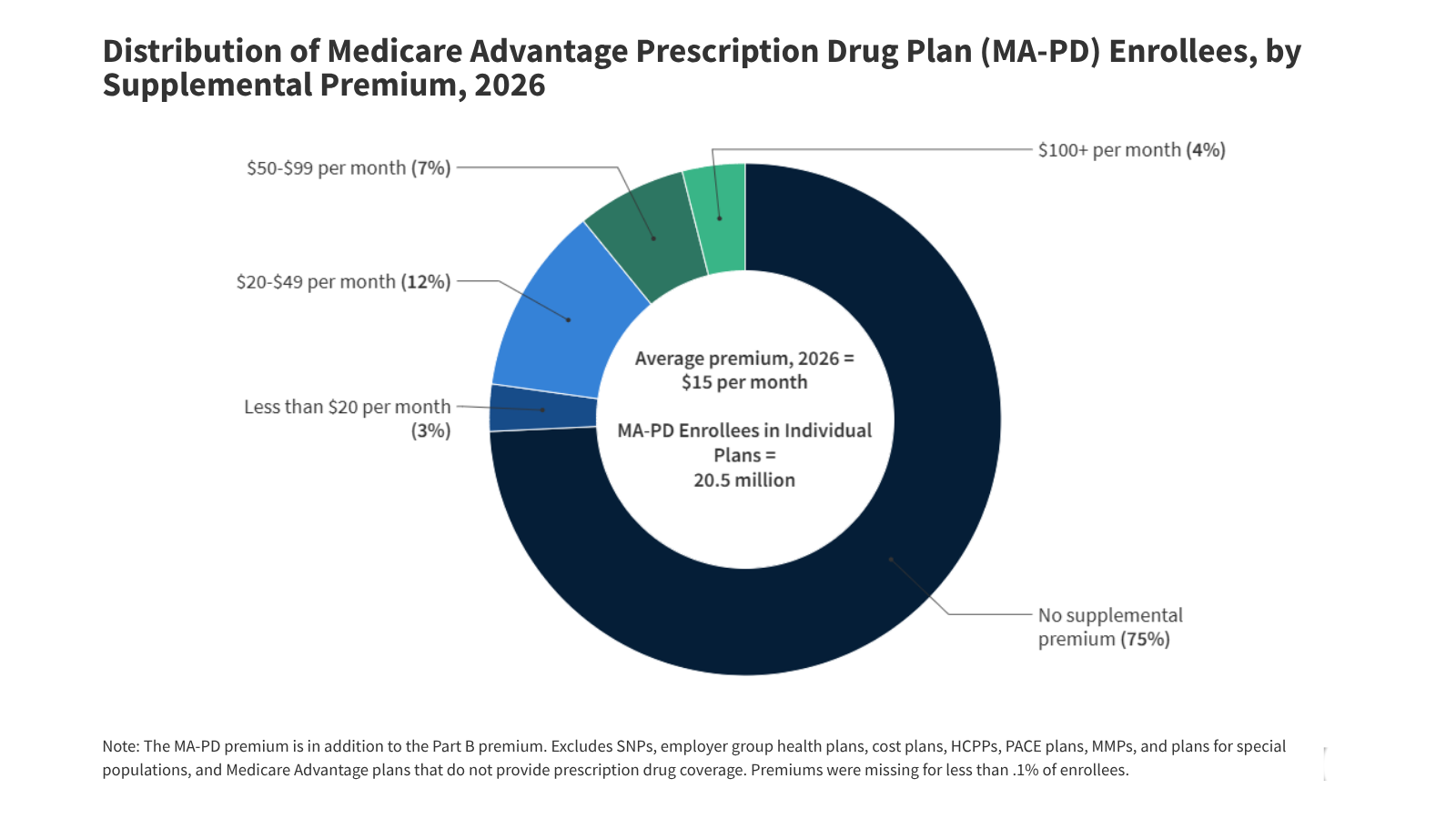

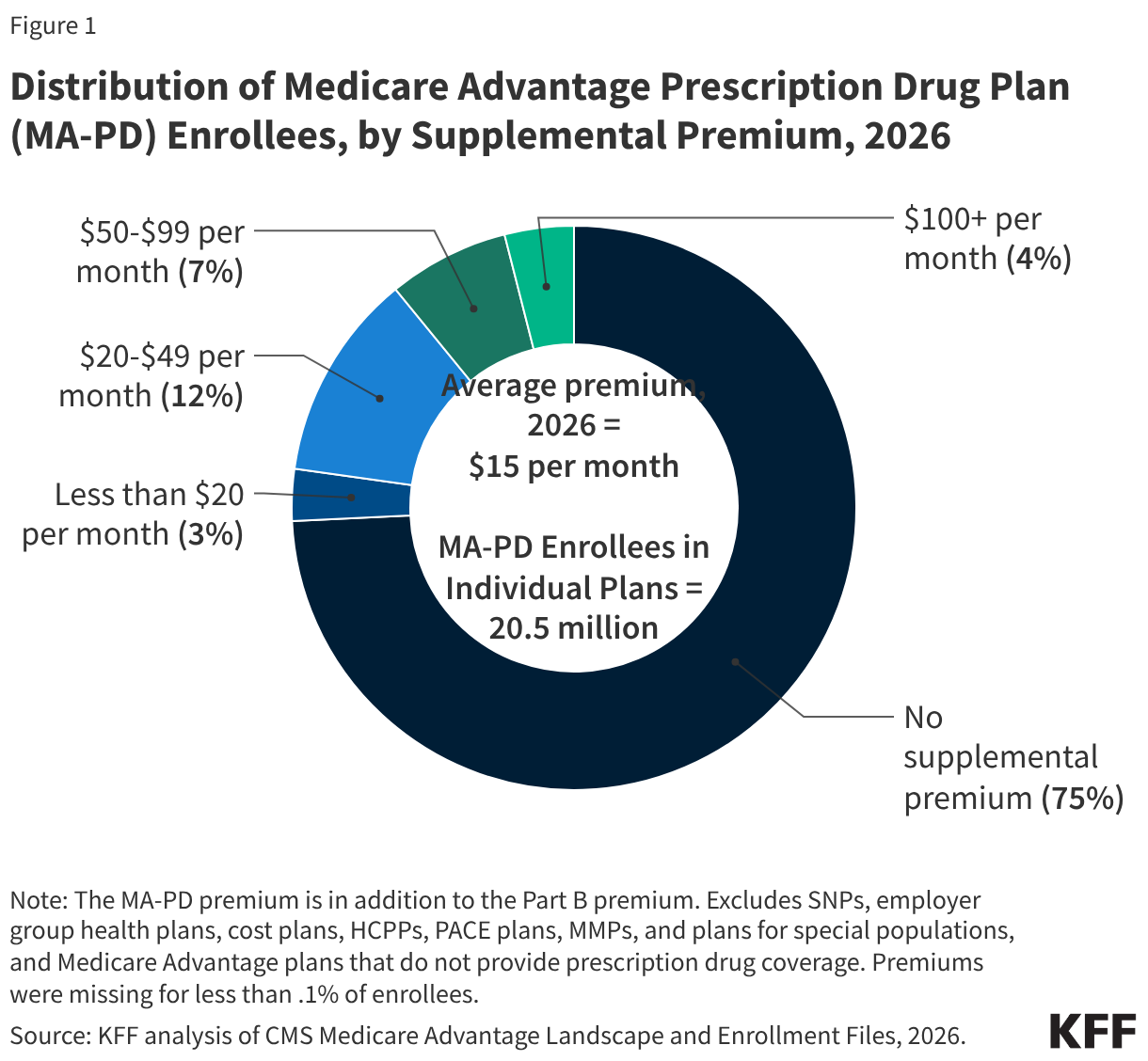

In 2026, 75% of MA-PD enrollees pay no premium beyond the standard Part B premium ($202.90). This is largely due to the $2,400 average rebate per enrollee for individual plans. Of that rebate, 26% is typically diverted to reduce Part D prescription drug premiums, explaining why MA-PD plans are often cheaper than stand-alone prescription drug plans.

Out-of-Pocket Limits

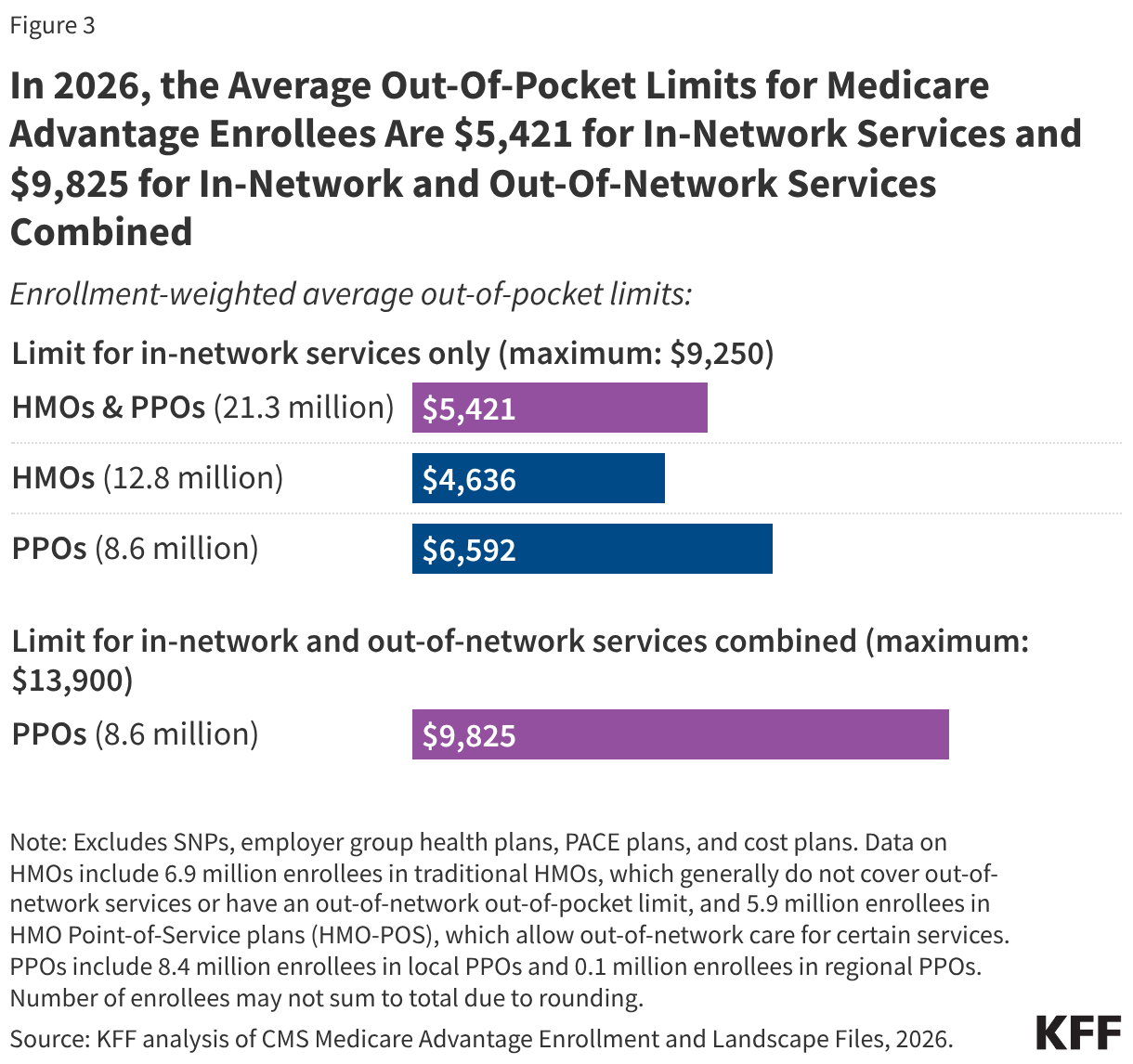

Unlike traditional Medicare, which lacks a hard cap on annual spending, Medicare Advantage plans are federally required to set out-of-pocket (OOP) limits.

- In-Network: The average limit is $5,421.

- Combined (In/Out-of-Network): For PPO plans, the average limit is $9,825.

While these figures represent a safeguard against catastrophic illness, they have trended upward since 2023, rising by approximately $700 in the last three years, which may signal a shift in how insurers manage financial risk.

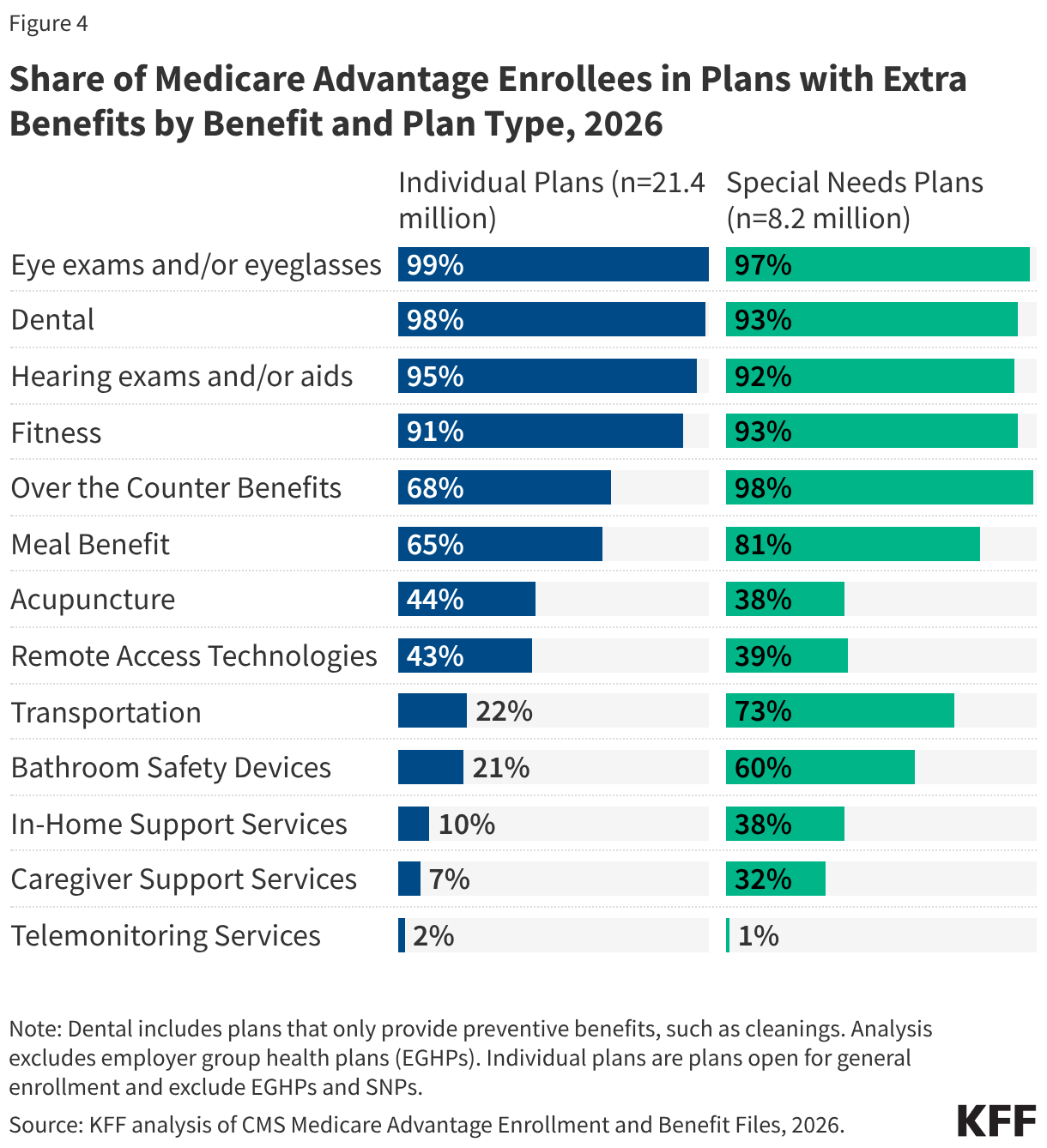

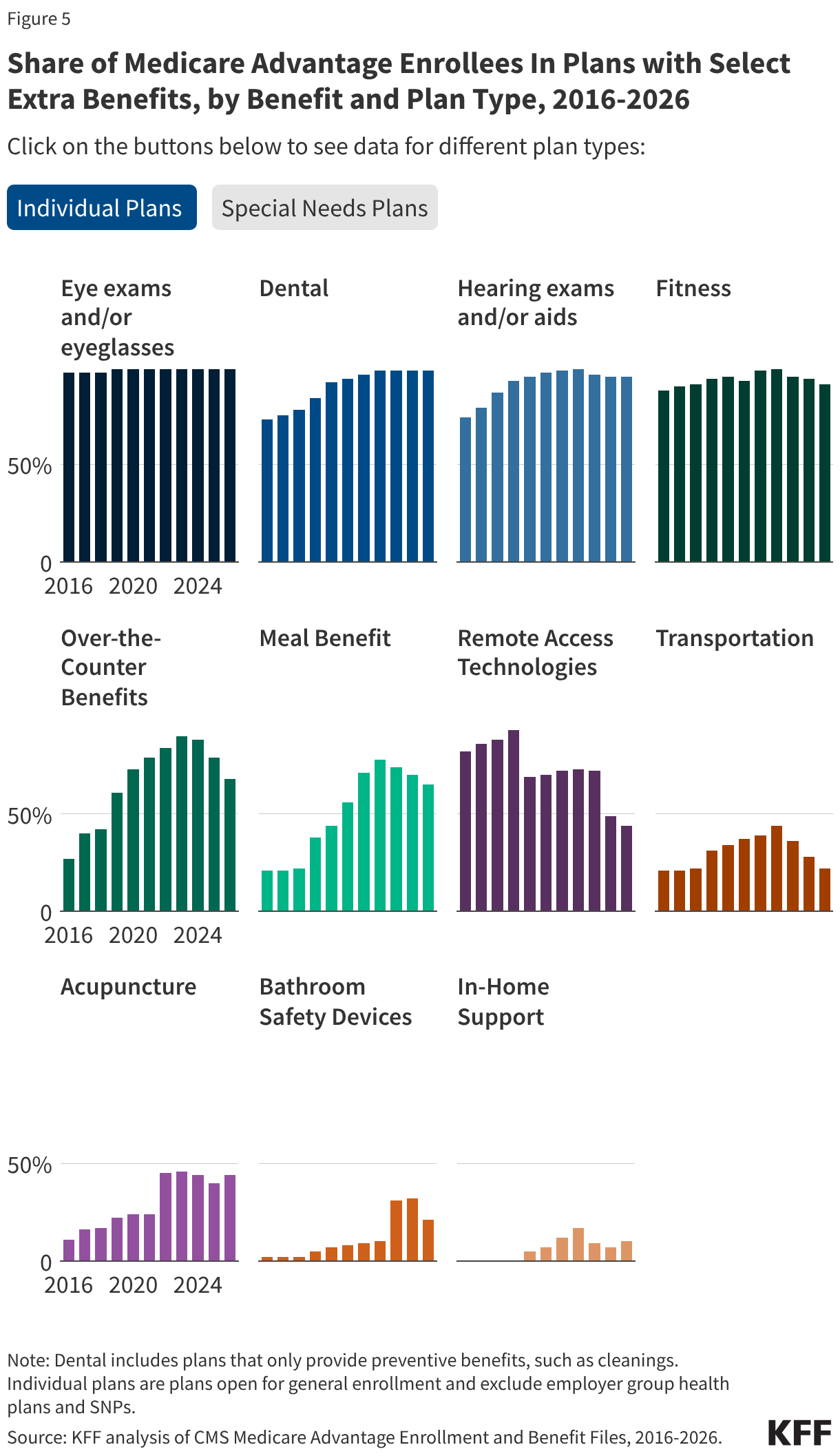

Supplemental Benefits and SSBCI

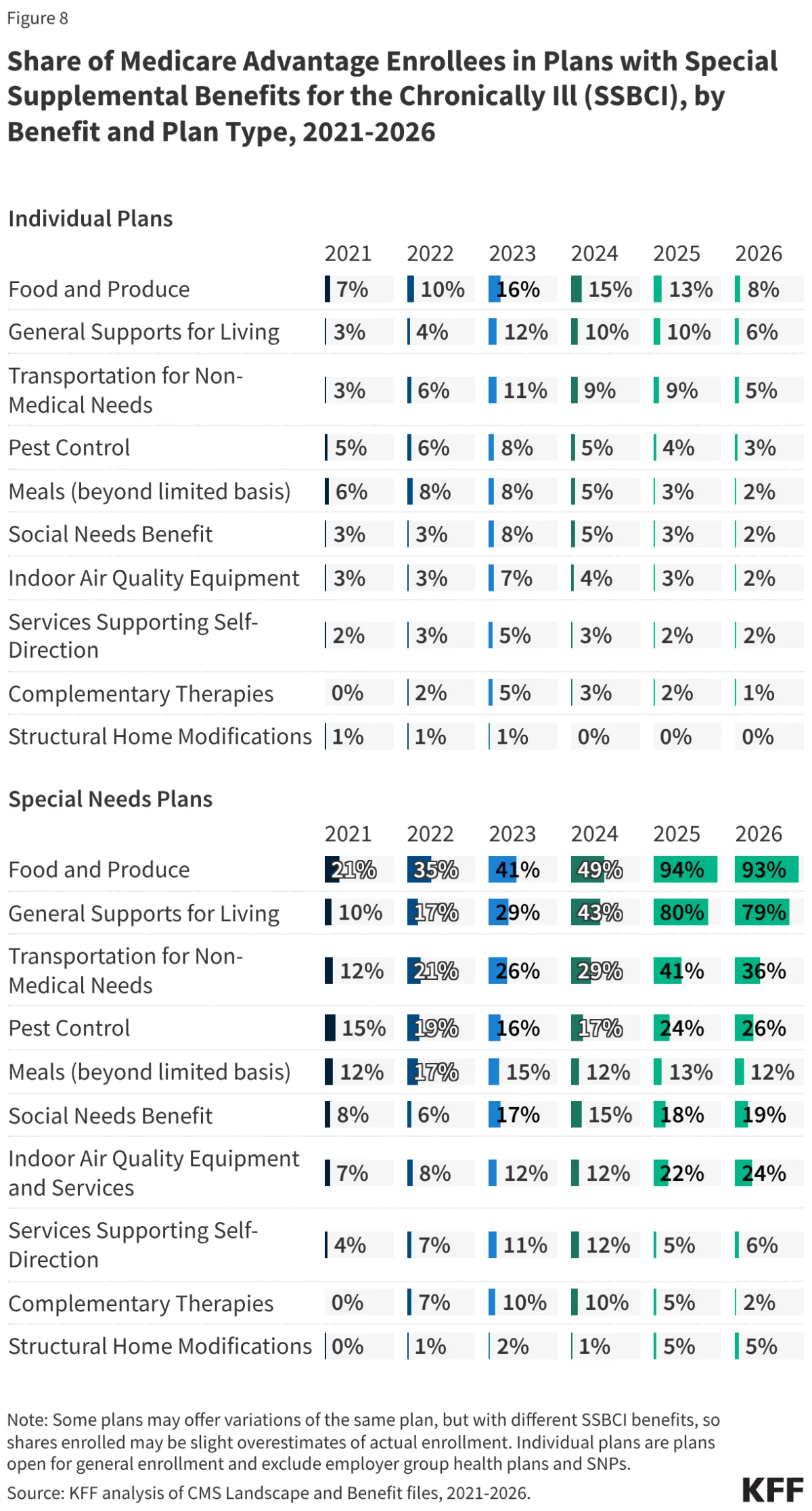

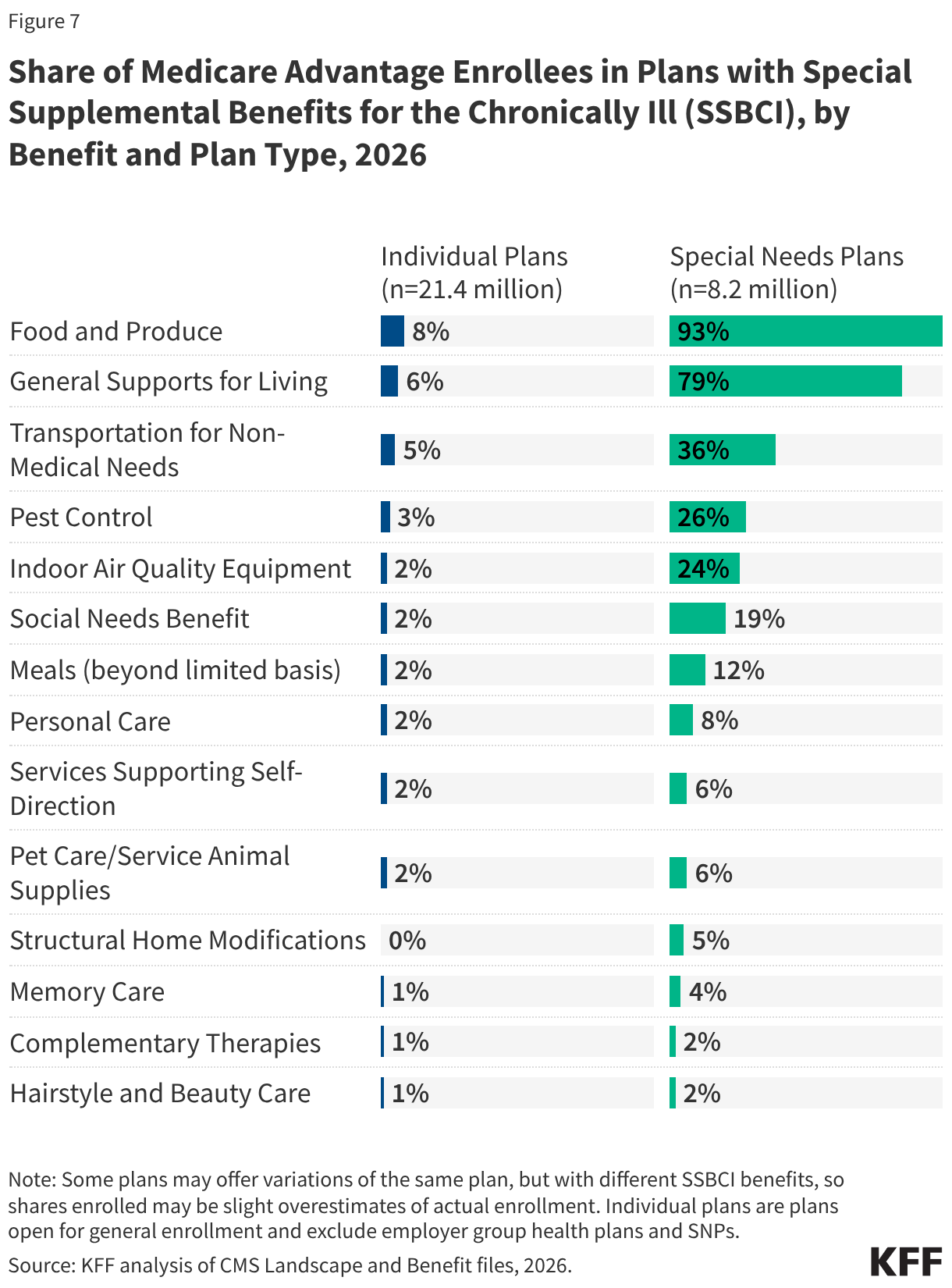

Supplemental benefits have become the primary marketing tool for MA plans. Virtually all individual plans now offer dental, vision, and hearing coverage. However, the generosity of these benefits varies significantly. Special Supplemental Benefits for the Chronically Ill (SSBCI)—such as food, produce, and utility assistance—have seen explosive growth, particularly in Special Needs Plans (SNPs). For instance, 93% of SNP enrollees now have access to food and produce benefits, compared to only 8% of enrollees in standard individual plans.

Official Responses and Regulatory Oversight

The Centers for Medicare & Medicaid Services (CMS) has maintained a dual focus: expanding access to supplemental care while attempting to increase transparency regarding administrative hurdles.

A central point of contention is the use of Prior Authorization (PA). In 2024, insurers processed nearly 53 million PA requests, denying roughly 8% of them. While plans claim these tools are essential to reduce unnecessary spending and ensure medical necessity, critics argue they serve as barriers to care. In 2026, 99% of Medicare Advantage enrollees are in plans that require prior authorization for at least some high-cost services, such as skilled nursing stays or Part B drugs.

While CMS has mandated more reporting on PA timeliness, significant data gaps remain. Researchers and the public still lack access to granular data on how denials vary by specific medical service or enrollee demographic, leaving a "black box" in the evaluation of insurer performance.

Implications for the Future of Medicare

The implications of the current Medicare Advantage model are profound for both the federal budget and the individual beneficiary.

1. The Paradox of Choice vs. Access

While the "extra" benefits offered by Medicare Advantage (gym memberships, vision, dental) are highly popular, they often come with restricted provider networks. Research indicates that the average MA enrollee has access to only about half the number of physicians available to those in traditional Medicare. As these networks continue to narrow, beneficiaries may find that the "value" of their supplemental benefits is offset by the difficulty of finding an in-network specialist.

2. Fiscal Sustainability

MedPAC has expressed consistent concern over the escalating cost of rebates. By paying private plans significantly more than the cost of care in traditional Medicare, the federal government is effectively subsidizing supplemental benefits for seniors, rather than just covering core medical services. As the federal deficit remains a priority for Congress, debates regarding whether to cap these rebates or adjust the benchmark payment formulas are likely to intensify.

3. The "Marketing" of Healthcare

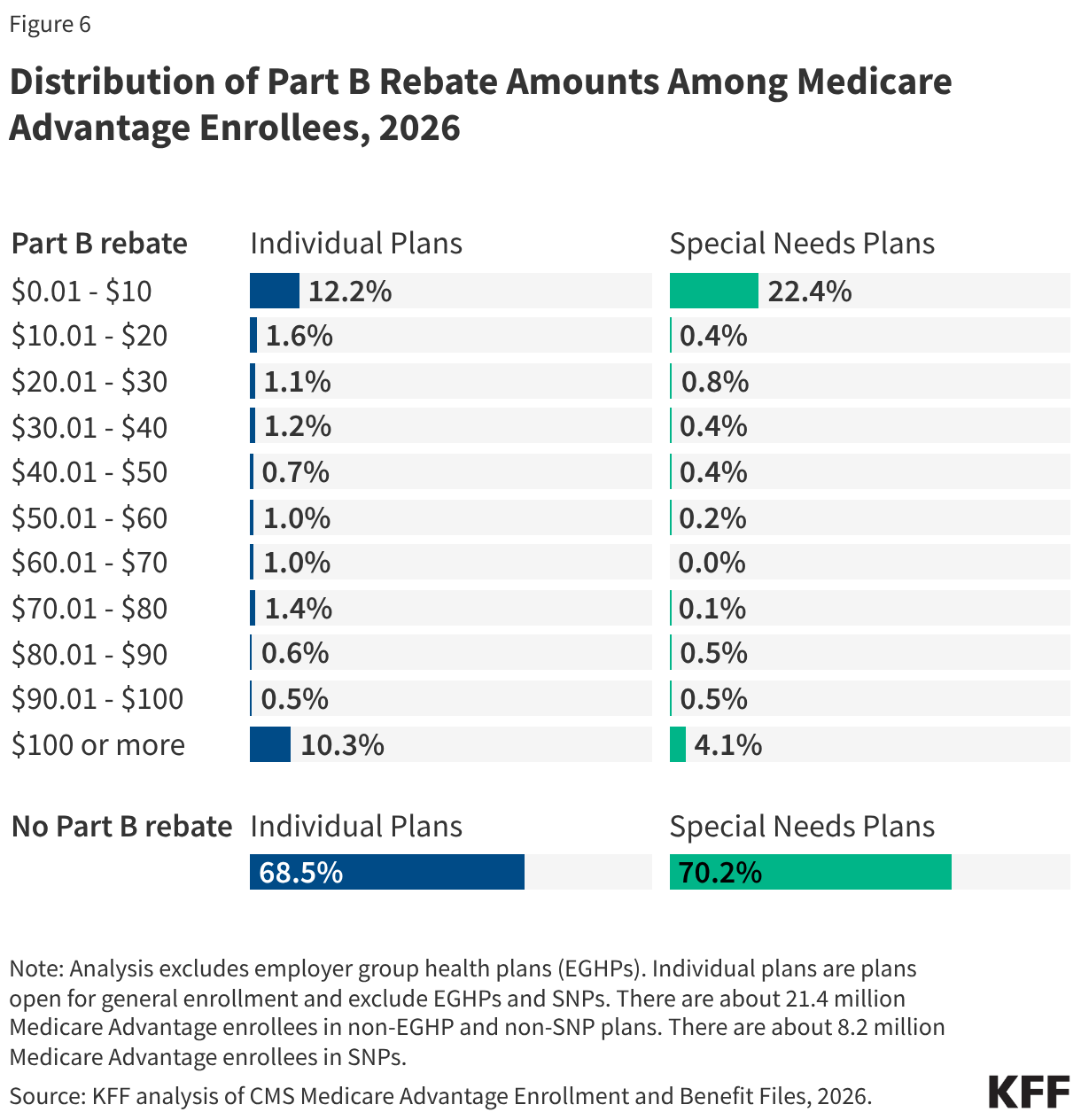

The reliance on Part B premium rebates—often marketed to seniors as "money back in your Social Security check"—remains a point of regulatory scrutiny. While these rebates exist, they are often nominal, with nearly 40% of beneficiaries receiving less than $10 per month. Policymakers are increasingly evaluating whether current marketing guidelines are sufficient to prevent misleading seniors into choosing plans based on small rebates rather than the actual quality of clinical care and network adequacy.

4. The Shift in Special Needs Plans

The surge in SSBCI benefits within SNP plans represents a new frontier in social determinants of health. By integrating food, transportation, and home support into the insurance package, these plans are addressing the root causes of poor health for the most vulnerable populations. However, the lack of data on the actual utilization of these benefits makes it difficult to measure their long-term efficacy in reducing hospital readmissions or improving patient outcomes.

Conclusion

Medicare Advantage in 2026 is a mature, highly integrated system that offers immense value in the form of supplemental benefits and capped out-of-pocket costs. Yet, it operates within a high-stakes financial environment where the cost to the federal government is rising, and the administrative burden on patients—via prior authorization and limited networks—continues to grow. For the millions of Americans navigating their enrollment options, the challenge remains to look past the marketing of "zero-premium" plans and evaluate the actual network access and care management policies that will determine their quality of life in their golden years. As CMS and Congress continue to refine the rules of the road, the balance between private-sector innovation and public-sector oversight will remain the defining feature of the Medicare experience.