In the high-stakes theater of global pharmaceuticals, cash is king—but how that cash is deployed defines the legacy of a CEO. Eli Lilly, currently riding the unprecedented wave of its tirzepatide franchise, has initiated a series of aggressive acquisitions, culminating in the recent deal to purchase CAR-T developer Kelonia Therapeutics for up to $7 billion.

As Lilly expands its footprint beyond metabolic health, industry analysts are asking a critical question: Is this a strategic evolution, or is the company repeating the cautionary tale of Pfizer? Following its pandemic-era spending spree—highlighted by the $43 billion acquisition of Seagen—Pfizer struggled to integrate massive assets while its COVID-19 revenue cratered. Lilly, by contrast, is deploying its windfall while its core growth engine is still accelerating.

Main Facts: A New Chapter for Lilly

The acquisition of Kelonia Therapeutics signals Lilly’s intent to dominate the next generation of immunotherapy. By focusing on in vivo CAR-T technology, Lilly is moving away from the cumbersome, expensive, and time-consuming ex vivo processes that have historically hampered the widespread adoption of cell therapies.

This deal is part of a broader, approximately $18 billion portfolio-building effort. Beyond Kelonia, Lilly has been systematically acquiring or partnering with firms like Morphic Therapeutic, Scorpion Therapeutics, Verve Therapeutics, and SiteOne Therapeutics. Furthermore, the company has entered a $2.75 billion collaboration with Insilico Medicine to harness artificial intelligence in the discovery of novel oral therapeutics.

Lilly’s pivot is underpinned by the staggering success of its metabolic portfolio. In 2025 alone, the company generated $65.2 billion in revenue, with the tirzepatide franchise—Mounjaro and Zepbound—accounting for $36.5 billion. With management guiding for $80 billion to $83 billion in revenue for 2026, Lilly is currently in the enviable position of having more capital than it can easily deploy through internal R&D alone.

Chronology of the Strategic Pivot

The divergence between Lilly and Pfizer’s acquisition philosophies can be traced through their recent corporate timelines:

- 2022–2023 (The Pfizer Peak and Valley): Pfizer, flush with record-breaking cash from Comirnaty and Paxlovid, pursued "big-ticket" acquisitions to fill an impending patent cliff. It acquired Biohaven ($11.6B) and Global Blood Therapeutics ($5.4B), culminating in the $43 billion purchase of Seagen. However, as the pandemic subsided, Pfizer’s revenue collapsed from $100.3 billion in 2022 to $58.5 billion in 2023—a 42% decline that left the company over-leveraged and under pressure.

- 2024 (Lilly’s Foundation): Lilly began its methodical expansion, acquiring Morphic Therapeutic for $3.2 billion to bolster its immunology and gastrointestinal portfolio.

- 2025 (Scaling the Platform): Lilly intensified its focus on early-stage, high-potential platforms, securing deals with Scorpion (up to $2.5B), Verve (approx. $1.3B), and SiteOne (up to $1B).

- April 2026 (The Oral Expansion): The FDA approved Foundayo (orforglipron), Lilly’s oral GLP-1 for obesity, under the National Priority Voucher program. This move solidified Lilly’s dominance in the metabolic space, providing a low-cost, oral alternative to the injectable tirzepatide franchise and adding a new growth vector that is expected to reach Medicare patients by mid-year.

- Late April 2026 (The Kelonia Deal): Lilly announced the acquisition of Kelonia, signaling a transition from pure metabolic focus into the next frontier of oncology and genetic medicine.

Supporting Data: Comparative Financial Performance

The fundamental difference between the two pharmaceutical giants lies in the lifecycle stage of their respective cash cows.

The Revenue Gap

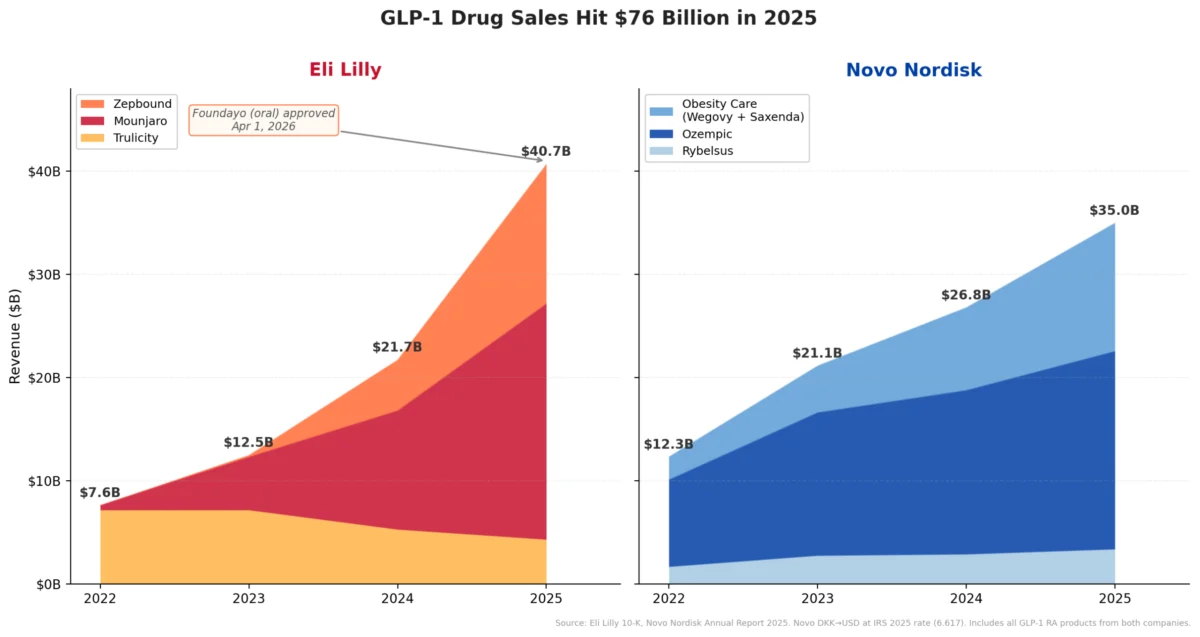

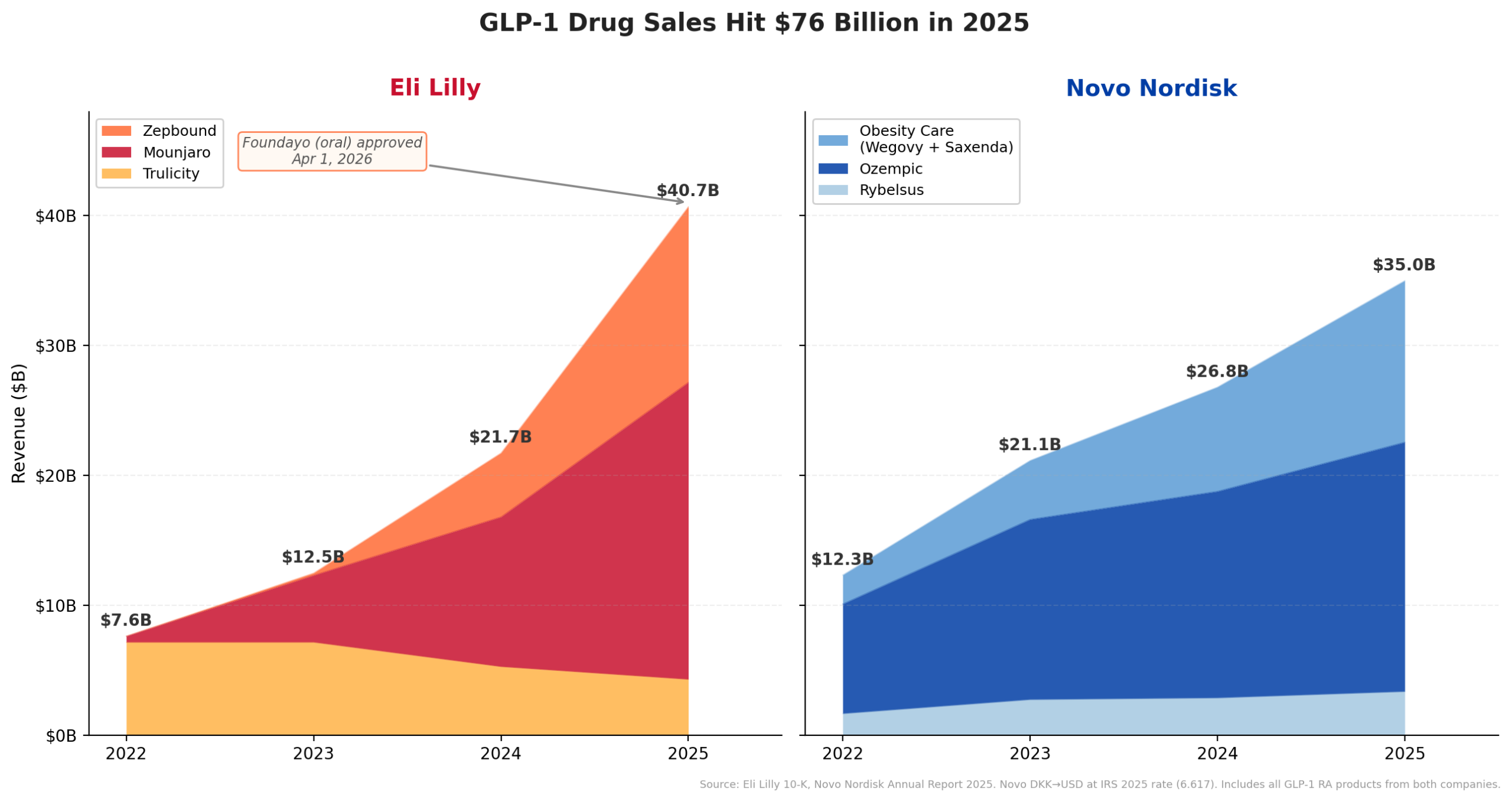

Lilly’s GLP-1 revenue surged from $7.6 billion in 2022 to $40.7 billion in 2025. This trajectory is significantly steeper than Novo Nordisk’s climb, which saw growth from $12.3 billion to $35.0 billion in the same period. While Lilly is guiding for sustained growth into 2026, Novo Nordisk has projected a decline in adjusted sales, highlighting a potential shift in the competitive balance between the two GLP-1 titans.

Acquisition Philosophy

Lilly’s approach is fundamentally different from Pfizer’s in terms of risk profile:

- Pfizer’s Strategy: Focused on "de-risked" assets. The acquisition of Seagen and Biohaven provided Pfizer with already-approved, commercial-stage products. While this provided immediate revenue, it came at a premium cost and required the integration of massive commercial infrastructure during a period of declining sales.

- Lilly’s Strategy: Focused on early-stage innovation. The majority of Lilly’s recent acquisitions (Kelonia, Verve, Scorpion) involve Phase 1 or early-stage assets. By buying at the clinical-trial stage rather than the commercial stage, Lilly pays a lower entry price and maintains the flexibility to integrate these assets into its existing, highly efficient R&D engine.

Official Perspectives and Market Implications

The Management View

Lilly leadership has maintained that their deal-making is not a reaction to market pressure, but a proactive strategy to sustain leadership into the 2030s. By using the massive margins from tirzepatide, they are funding a pipeline that covers immunology, oncology, and cardiovascular disease. The partnership with Insilico Medicine further suggests that Lilly is attempting to "industrialize" the drug discovery process, using AI to shorten the timeline between target identification and clinical trials.

The Analyst View

Market observers are cautiously optimistic. The primary concern with M&A in pharma is the "integration tax"—the tendency for corporate cultures to clash and for administrative bloat to erode the value of the acquired company. However, Lilly’s track record of internal R&D success suggests they are better equipped than most to handle the scientific integration of firms like Kelonia.

The "Pfizer Trap" was essentially a failure of timing: buying expensive assets at the top of a pandemic-driven bubble. Lilly, conversely, is buying during a period of organic growth. Even if the GLP-1 market were to plateau, Lilly’s balance sheet—with $16.8 billion in operating cash flow as of late 2025—provides a significant buffer that Pfizer lacked when its COVID revenue disappeared.

Future Outlook: The Road Ahead

The implications of the Kelonia acquisition go beyond the $7 billion price tag. If Lilly succeeds in bringing in vivo CAR-T therapies to market, it could disrupt the entire oncology sector, making cell therapy a standard, "off-the-shelf" treatment rather than a bespoke, hospital-bound procedure.

With the Q1 2026 earnings call approaching on April 30, investors are looking for two things:

- Margin sustainability: Can Lilly maintain its current profitability while aggressively funding its new, early-stage pipeline?

- Operational discipline: How will the company manage the integration of diverse platforms like Kelonia’s gene-editing technology and Insilico’s AI engine?

In conclusion, while comparisons to Pfizer’s turbulent acquisition cycle are inevitable, the data suggests that Eli Lilly is playing a different game. By avoiding the acquisition of late-stage, high-cost assets in favor of foundational platform technologies, and by executing these deals while its primary revenue engine is still in high gear, Lilly is attempting to rewrite the playbook on how a modern, blockbuster-funded pharmaceutical company evolves.

The next 24 months will be decisive. If the early-stage bets pay off, Lilly will have successfully transitioned from an obesity-focused powerhouse to a diversified, AI-driven innovator. If they fail, the company risks becoming the very thing it seeks to avoid: a giant tethered to a fading blockbuster, struggling to justify the cost of its own ambition. For now, the momentum remains firmly in Lilly’s favor.