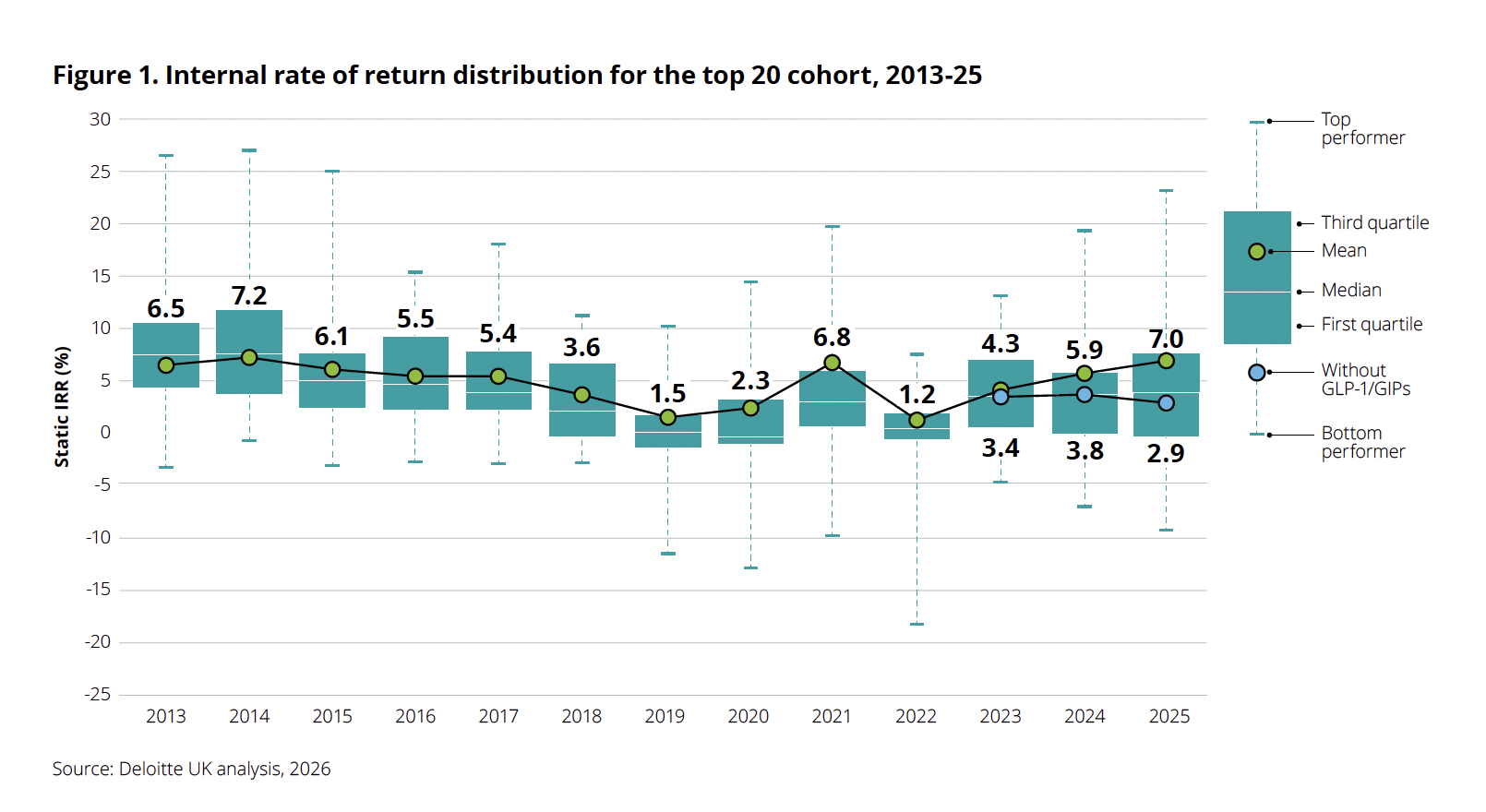

After a prolonged period of "post-pandemic hibernation"—characterized by uneven growth and dwindling R&D returns—the global biopharmaceutical sector is showing signs of a dramatic, if lopsided, recovery. According to the 16th edition of Deloitte’s annual Measuring the Return from Pharmaceutical Innovation report, titled "Navigating the GLP-1 boom," the projected internal rate of return (IRR) on late-stage pipeline assets has climbed for the third consecutive year, reaching 7.0% in 2025. This marks a significant recovery from the 5.9% recorded in 2024.

However, beneath the surface of this optimistic headline lies a stark reality: the industry’s newfound financial health is being propped up by a single therapeutic class. When the hyper-growth of GLP-1 and GIP receptor agonists is stripped away, the sector’s underlying productivity reveals a different, more concerning trajectory.

The Main Facts: A Tale of Two Pipelines

The 2025 data paints a vivid picture of a market dominated by the obesity and metabolic disease revolution. GLP-1/GIP drugs, which have transformed the landscape of weight management and cardiovascular health, now account for an estimated 38% of all projected commercial inflows from the 2025 late-stage pipeline.

The statistical impact of this concentration is profound. If these obesity-focused therapies are removed from the calculation, the headline IRR of 7.0% collapses to a mere 2.9%. To put this into perspective, in 2024, the IRR without GLP-1/GIP drugs stood at 3.8%. This suggests that while the industry is celebrating a return to "spring," the core engines of innovation—outside of the current metabolic craze—are actually losing efficiency.

"There are two different messages here," says Kevin Dondarski, principal for life sciences strategy at Deloitte Consulting. "One, it’s certainly attractive, because the market is valuing the potential impact that those therapies can have on the public. But at the same time, it raises the question of sustainability. As those programs progress, is there going to continue to be that opportunity through the next generation and the next? It will create a responsibility for these companies to find the right assets to replace in the pipeline."

A Chronology of the GLP-1 Surge and Market Volatility

The rise of the GLP-1 class has not been a smooth ascent. It has been marked by massive capital investment, aggressive restructuring, and intense clinical competition.

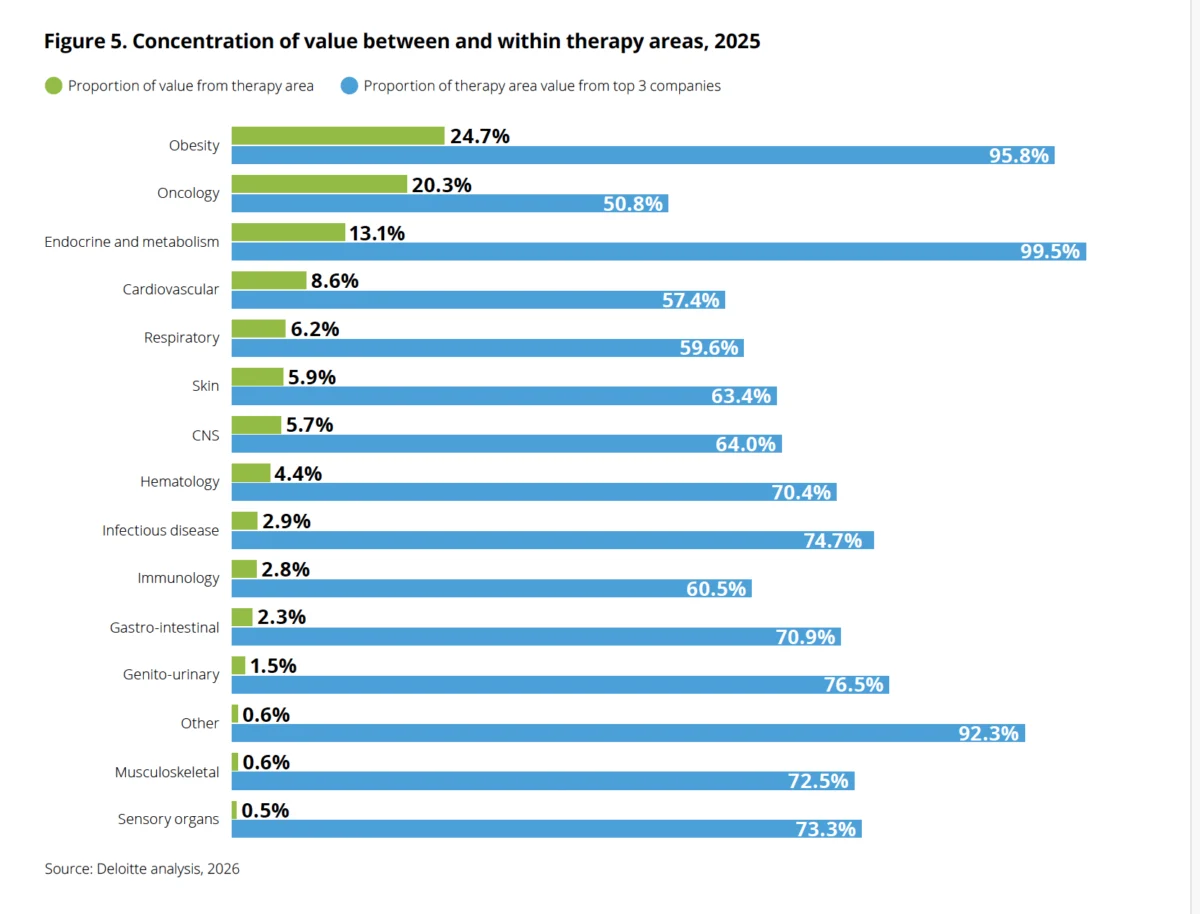

- Early 2025: The sector begins to see the full weight of GLP-1 commercial success, with obesity-related assets claiming the largest share of late-stage pipeline value (24.7%), officially displacing oncology (20.3%) for the first time in the 16-year history of the Deloitte report.

- November 2025: Amidst slowing momentum in certain markets and shifting investor sentiment, Novo Nordisk undergoes a massive leadership and organizational shakeup. Seven board members step down, and the company announces plans to cut 9,000 roles.

- February 2026: A critical setback for the "first-mover" advantage occurs when Novo Nordisk’s CagriSema fails to demonstrate non-inferiority against Eli Lilly’s Zepbound in the REDEFINE 4 Phase 3 head-to-head trial. The failure to hit primary endpoints triggers a wave of investor skepticism regarding the future of next-generation combinations.

- April 2026: Eli Lilly launches its oral GLP-1, Foundayo (orforglipron), as the market continues to grapple with the "price-volume" trade-off. Despite raising full-year revenue guidance to $82–$85 billion, Lilly’s stock faces a 10–13% decline year-to-date, reflecting investor anxiety about the sustainability of current profit margins.

- May 2026: New data confirms that while volume for GLP-1s is soaring, realized prices are under downward pressure due to Medicare and Medicaid pricing agreements, including the introduction of the "TrumpRx" pricing schedule.

Supporting Data: The Cost of Innovation

The Deloitte report highlights that the average cost to bring a drug from discovery to launch has ballooned to $2.67 billion, up from $2.23 billion in 2024. This trend is not confined to a few outliers; 17 out of the 20 companies surveyed reported significant increases in R&D spending.

Three primary factors are driving this escalation:

- Inflationary Pressure: R&D labor and material costs continue to outpace general inflation metrics.

- M&A Bloat: Large-scale acquisitions, while necessary to fill pipelines, are inflating the R&D cost base without necessarily yielding immediate improvements in clinical success rates.

- High Attrition: A 4–5% reduction in the total number of late-stage programs suggests that companies are either failing more often or becoming more selective, yet the cost of the remaining "winners" continues to rise.

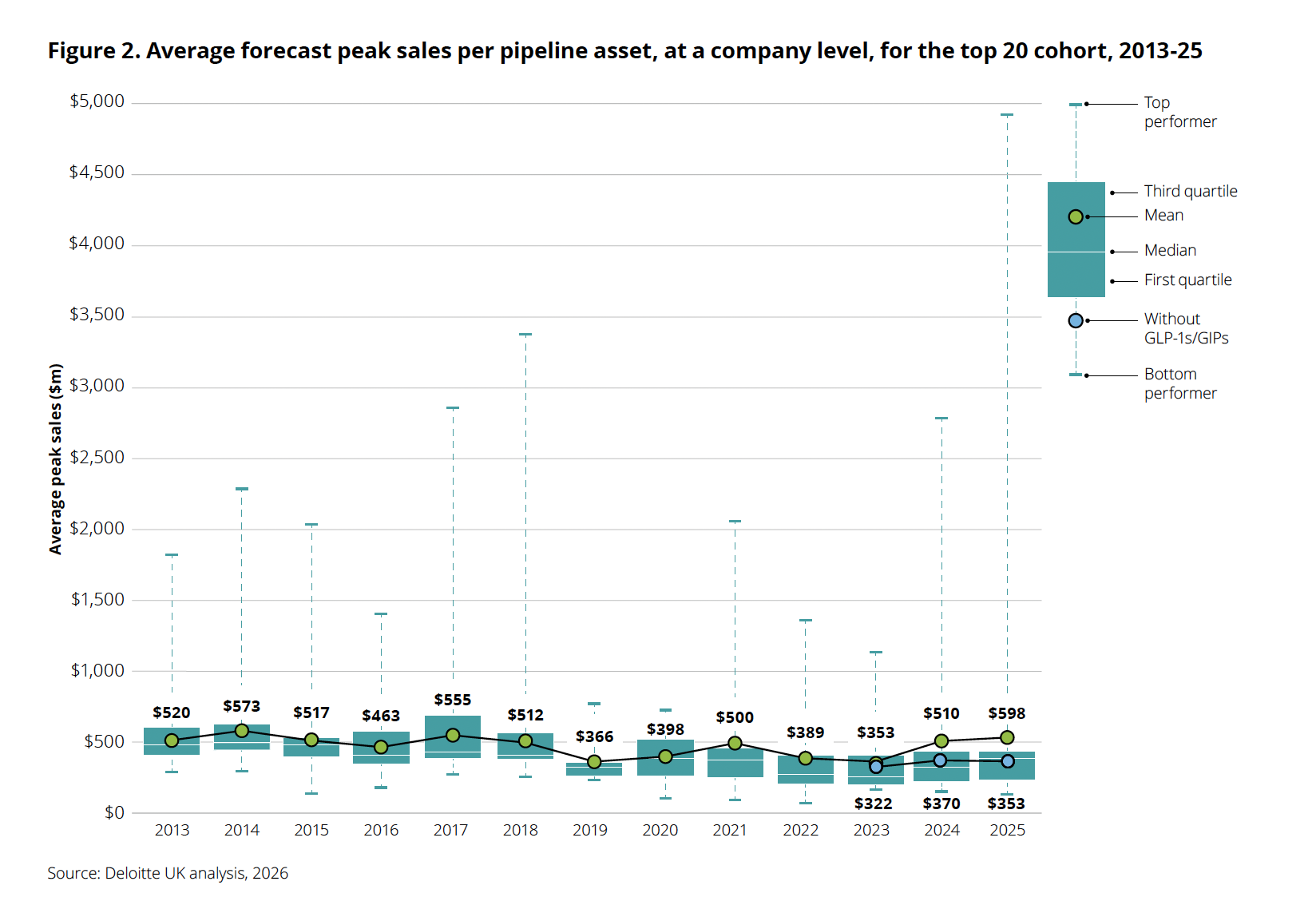

Perhaps most tellingly, the average forecast peak sales per pipeline asset jumped to $598 million in 2025. However, the distribution is skewed by the GLP-1 juggernauts. If the obesity blockbusters are excluded, the average forecast peak sales figure drops to $353 million—a decline from the previous year. This confirms that for the "non-GLP" portion of the industry, productivity is not just stagnant; it is actively declining.

Official Responses and Strategic Implications

Industry leaders are now facing a period of introspection. The reliance on a single, albeit massive, drug class is creating a "responsibility gap." Companies are being forced to decide whether to double down on the metabolic space—which is currently dominated by just three major players—or pivot back to traditional therapeutic pillars like oncology and neurology.

The competitive landscape within the obesity market is also becoming increasingly cutthroat. With 96% of the value in the obesity pipeline concentrated among three firms, the "barrier to entry" for newcomers is effectively becoming a moat. For companies like Novo Nordisk and Eli Lilly, the strategy has shifted from pure R&D volume to manufacturing scale and "price-volume" optimization. As noted by the 13% decline in realized prices for Lilly, the era of unbridled pricing power for GLP-1s appears to be ending, replaced by the realities of public health mandates and Medicare price negotiations.

The AI Disconnect: Promise vs. Reality

Perhaps the most sobering finding in the 2025 report concerns Artificial Intelligence. Last year, the industry was exhorted to "be brave, be bold" and utilize AI to break the cycle of declining R&D productivity.

Despite the surge in AI adoption, the data shows that the clinical cycle times remain "stubbornly long." Deloitte’s analysis concedes that the promise of AI to fundamentally reduce development costs and timelines has not yet materialized at scale. The report attributes this failure to a "pilot-driven, function-by-function approach." Instead of a holistic, enterprise-wide transformation, AI is currently being used for isolated tasks, which prevents the industry from capturing the compound efficiency gains necessary to lower the $2.67 billion average cost per asset.

"Everybody’s actively focusing on AI, and everybody’s had some degree of success," says Dondarski. "But from our vantage point, there’s a good amount of variability in the velocity at which organizations are scaling those efforts to maximize value creation."

Future Outlook: The Sustainability Imperative

The pharmaceutical industry stands at a crossroads. The "GLP-1 boom" has provided a much-needed financial infusion, allowing many companies to weather the turbulence of the post-pandemic years. However, the reliance on a single, high-concentration class of drugs is a structural vulnerability.

As the industry moves toward 2027, the primary challenge will be to diversify the pipeline without sacrificing the profitability that the obesity market has provided. If the sector fails to integrate AI and advanced analytics into the core of its R&D process—moving beyond "pilot projects" into full-scale operational transformation—the rising costs of development will eventually erode the gains made by the current metabolic wave.

For investors and patients alike, the next three years will be defined by one question: Can the industry find the "next" GLP-1, or will it be forced to confront a future where the cost of innovation is no longer sustainable? The "spring" may have arrived, but as the Deloitte report suggests, the biopharma sector has yet to prove that this season of growth is anything more than a temporary reprieve from a long and difficult winter.