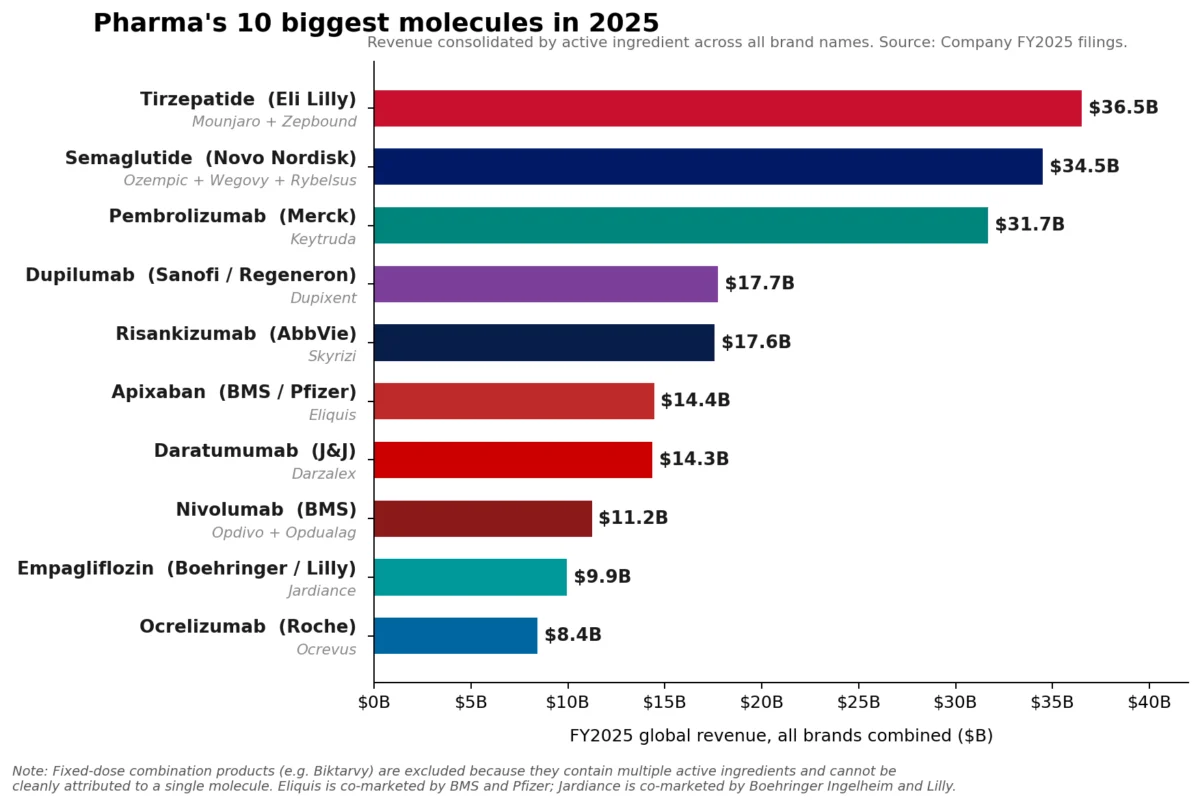

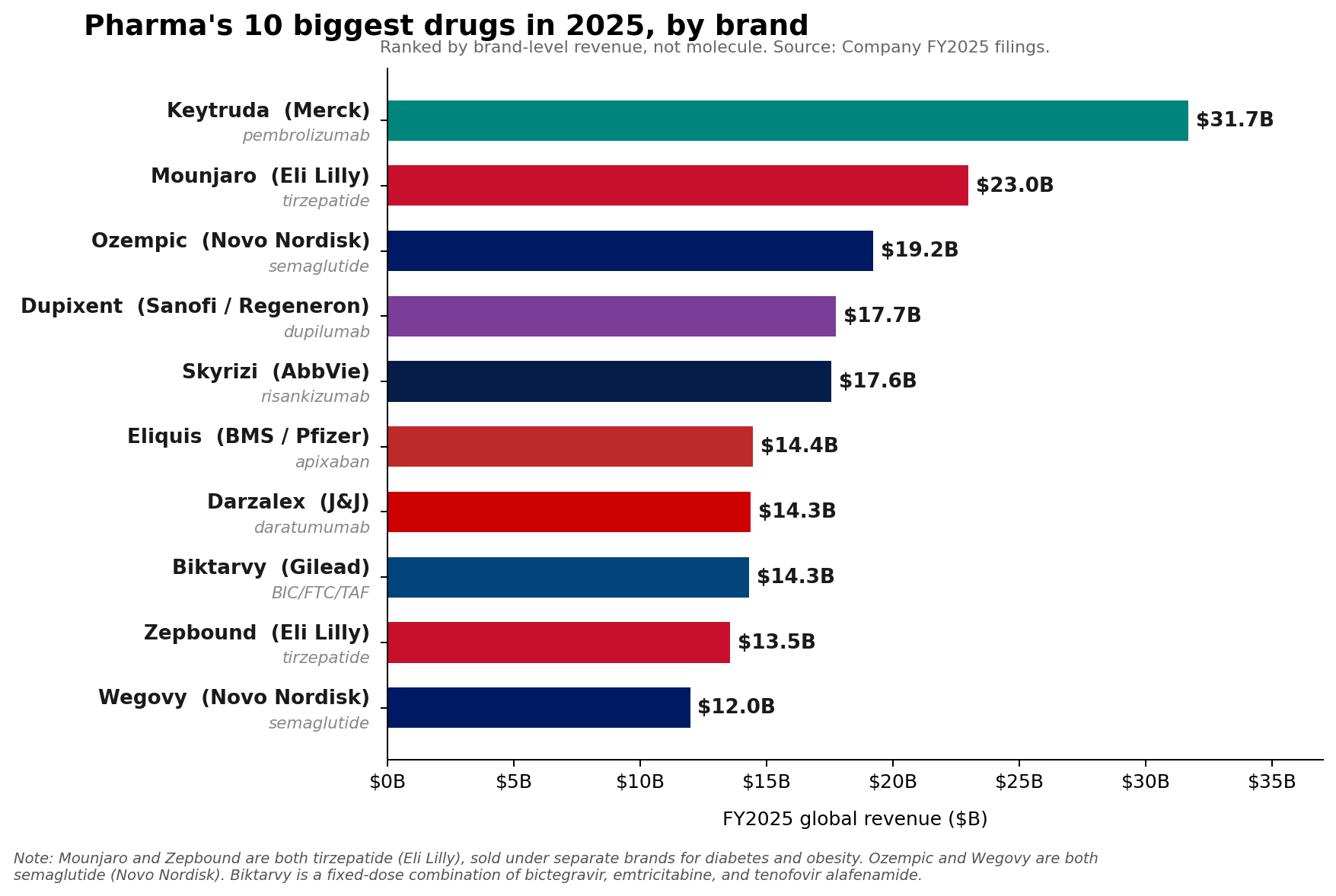

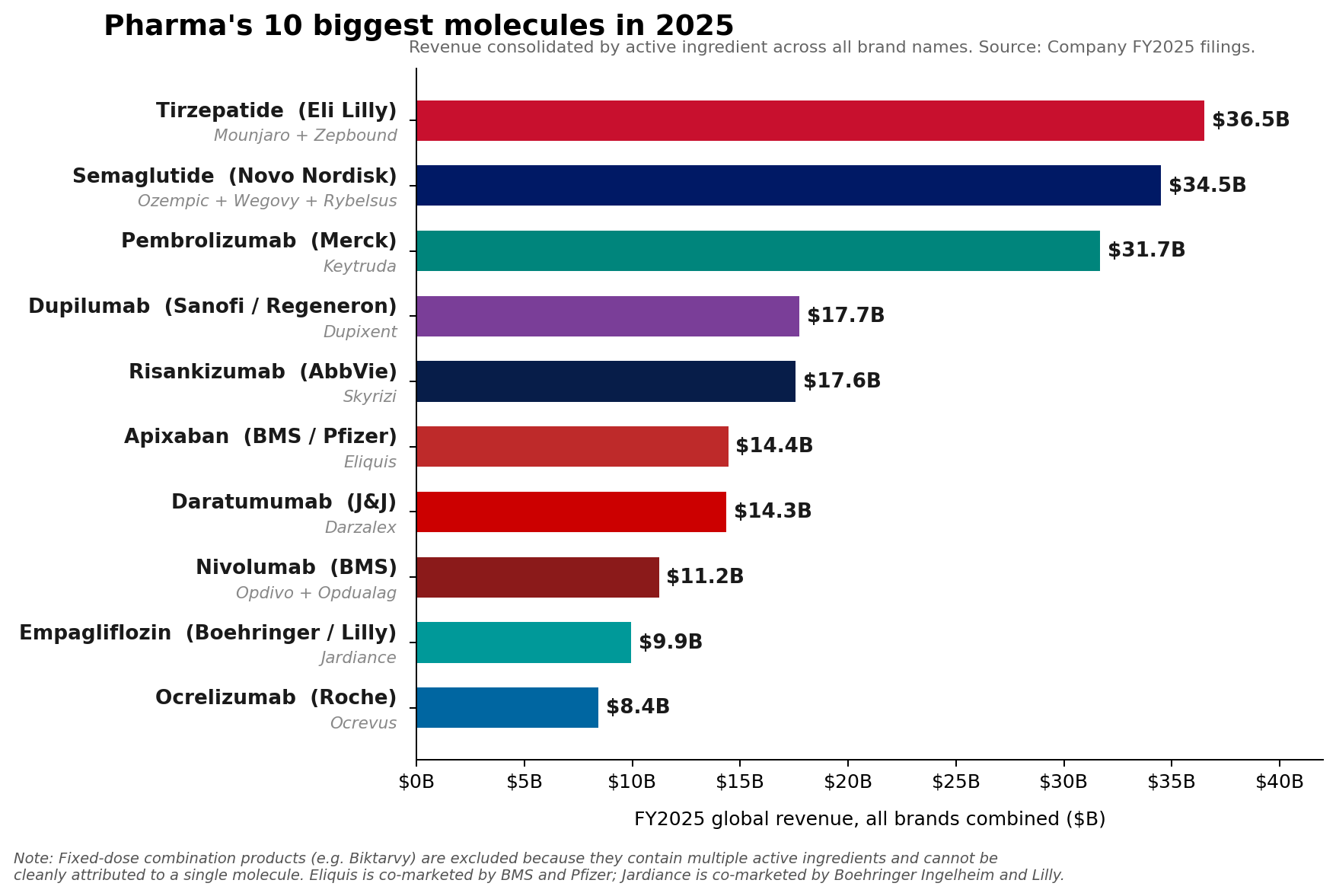

The global pharmaceutical landscape has undergone a seismic shift. For years, Merck & Co.’s oncology powerhouse, Keytruda (pembrolizumab), stood unchallenged as the undisputed sovereign of the drug industry. However, the fiscal year 2025 results confirm a historic transition: while Keytruda remains the top-selling individual brand with $31.7 billion in revenue, it has been eclipsed at the molecule level by the dual-engine weight-loss franchises of Eli Lilly and Novo Nordisk.

As the industry pivots toward metabolic health and high-growth immunology, the traditional "blockbuster" model is being redefined. The rise of GLP-1 receptor agonists and the compounding success of specialty immunology drugs suggest that the future of pharma will be defined not by a single dominant monopoly, but by deep, multi-product franchises that command billions across diverse patient populations.

Main Facts: The New Revenue Hierarchy

In FY2025, the pharmaceutical industry’s revenue hierarchy underwent a dramatic reordering. Merck’s Keytruda, while still posting an impressive 7% growth, has officially ceded its status as the highest-grossing therapeutic entity.

- The GLP-1 Dominance: Eli Lilly’s tirzepatide franchise—encompassing the blockbuster products Mounjaro ($22.965 billion) and Zepbound ($13.542 billion)—reached a combined annual revenue of approximately $36.5 billion. Simultaneously, Novo Nordisk’s semaglutide portfolio, anchored by Ozempic, Wegovy, and Rybelsus, surged to roughly $34.5 billion.

- The Immunology Counter-Movement: Beyond the obesity craze, immunology remains a bastion of stability and growth. AbbVie’s Skyrizi ($17.562 billion) and Rinvoq ($8.304 billion) continue to demonstrate that established therapeutic areas can still produce massive, durable revenue streams.

- The Shift in Pipeline Strategy: According to Citeline’s 2026 R&D review, the overall number of pipeline assets has contracted, yet the anti-obesity sector has seen a "gut-busting" 30.7% expansion, now encompassing 588 active compounds.

Chronology: The Road to the 2026 Shift

The current state of the market is the result of a multi-year trajectory defined by high-stakes R&D and aggressive commercial execution.

- 2018: Eli Lilly secures a pivotal research and licensing agreement with Chugai, acquiring the rights to what would become orforglipron. This set the stage for a strategic move into oral, small-molecule GLP-1 therapy.

- 2023–2024: The "GLP-1 Boom" dominates public discourse and investor sentiment, as supply chain constraints and manufacturing expansion dictate the ceiling for Mounjaro and Wegovy sales.

- January 2026: Novo Nordisk officially launches its new oral Wegovy pill, signaling a strategic pivot to diversify its delivery methods beyond injectables.

- April 1, 2026: The FDA grants approval to Lilly’s Foundayo (orforglipron). This landmark approval introduces the first once-daily oral small-molecule GLP-1 agonist, effectively launching a new chapter in the obesity wars.

- April 6, 2026: Commercial shipping of Foundayo begins in the United States, positioning it as the primary strategic wildcard for the remainder of the 2026 fiscal year.

Supporting Data: By the Numbers

The financial data from FY2025 and the guidance for 2026 highlight the bifurcation between established oncology leaders and the new metabolic wave.

The Revenue Leaderboard (FY2025)

| Drug/Franchise | 2025 Revenue (USD) | Status |

|---|---|---|

| Tirzepatide (Lilly) | ~$36.5 Billion | #1 Molecule |

| Semaglutide (Novo) | ~$34.5 Billion | #2 Molecule |

| Keytruda (Merck) | $31.7 Billion | #1 Single Brand |

| Skyrizi (AbbVie) | $17.562 Billion | Immunology Leader |

Comparative Growth Drivers

- Merck’s Outlook: Despite Keytruda’s growth, Merck’s FY2026 revenue guidance of $65.5–$67 billion fell slightly below Wall Street’s aggressive expectations, highlighting the market’s anxiety regarding Keytruda’s eventual loss of exclusivity.

- Lilly’s Scale: Eli Lilly is guiding toward $80–$83 billion in total 2026 revenue. The sheer scale of this target underscores the transition from "single-drug dependency" to a diversified portfolio of metabolic blockbusters.

- Novo’s Paradox: Interestingly, Novo Nordisk projects adjusted sales growth between -5% and -13% for 2026 at constant exchange rates (CER). This reflects a complex environment of pricing pressure, heightened competition, and U.S. market access hurdles, serving as a reminder that volume growth does not always equate to top-line margin expansion.

Official Responses and Strategic Perspectives

Merck: Managing the "Hill, Not a Cliff"

Merck CEO Rob Davis has been vocal in his attempts to reassure investors about the long-term viability of the company’s pipeline. By characterizing the expiration of Keytruda’s patent protection as "more of a hill than a cliff," Davis is signaling that Merck’s strategy—which includes the development of subcutaneous delivery methods like QLEX and a push into new oncology indications—is designed to bridge the gap. However, the market remains skeptical, as reflected in the cautious reaction to recent revenue guidance.

Eli Lilly: The Strategic Wildcard

The launch of Foundayo (orforglipron) represents a critical strategic inflection point. Lilly leadership has emphasized that while the drug is a "major strategic variable," the immediate 2026 growth will remain dominated by the established momentum of Mounjaro and Zepbound. The goal with orforglipron is not necessarily to replace these injectables immediately, but to capture a new segment of the market that may be hesitant about self-injection, thereby expanding the overall "funnel" of patients.

AbbVie: The Power of Immunology

AbbVie’s success serves as the primary counter-narrative to the "GLP-1 monoculture" theory. By scaling Skyrizi and Rinvoq to a combined $25.866 billion—representing over 42% of the company’s total revenue—AbbVie has proven that immunology franchises can match the scale of the biggest oncology brands. This strategy of "compounding" existing franchises provides a blueprint for stability in an otherwise volatile sector.

Implications: The Future of the Pharmaceutical Market

1. The End of the "Single-Drug" Era

For years, the industry was obsessed with finding the next "Keytruda"—a single, massive-revenue-generating asset. The 2025-2026 data indicates a shift toward "franchise-based" success. Companies are no longer relying on a single molecule to anchor their valuation; they are relying on portfolios (like Lilly’s tirzepatide or Novo’s semaglutide) that can be iterated upon through new doses, new delivery methods, and new therapeutic indications.

2. The Weight-Loss Market as a Commodity or Utility?

As the obesity market grows to include more players and delivery methods (oral vs. injectable), the competitive landscape will inevitably shift from "who has the best drug" to "who has the best access, supply chain, and price point." The entry of Foundayo will force a recalibration of pricing strategies across the entire GLP-1 sector.

3. Resilience in Immunology and Oncology

The data from Citeline regarding the expansion of the immunology pipeline (up 20.6%) suggests that pharma is not putting all its eggs in the metabolic basket. Large, durable franchises in immunology and oncology remain the bedrock of the industry. The "leaderboard" is becoming increasingly crowded, which is a positive indicator for long-term industry health, as it limits the systemic risk associated with the decline of any single therapeutic class.

4. The Wall Street Disconnect

Perhaps the most significant implication of the 2026 data is the widening gap between internal company guidance and market expectations. As pharma companies pivot their R&D toward faster-growing but more competitive areas like obesity, the traditional models used by analysts to predict revenue are being challenged. The volatility in revenue guidance from leaders like Merck and Novo Nordisk signals that the industry is in a transition period where previous growth benchmarks may no longer apply.

Conclusion: A New Equilibrium

The pharmaceutical industry of 2026 is one defined by high-stakes competition and, paradoxically, greater depth. While Keytruda’s time as the undisputed king has ended, the rise of the GLP-1 class and the persistent strength of immunology show an industry that is more capable than ever of generating massive, multi-billion-dollar franchises. For investors and patients alike, the next few years will be defined by how these companies navigate the delicate balance of sustaining high-volume metabolic growth while investing in the next generation of life-saving innovations.