As the pharmaceutical industry navigates a transformative era defined by the meteoric rise of metabolic blockbusters, Eli Lilly and Company finds itself at a pivotal crossroads. Flush with record-breaking revenues from its tirzepatide franchise—the engine behind Mounjaro and Zepbound—Lilly has embarked on a high-stakes acquisition spree. The most recent move, a deal to acquire CAR-T specialist Kelonia Therapeutics for up to $7 billion, marks a bold shift toward next-generation oncology.

However, for industry observers, this aggressive dealmaking invites inevitable comparisons to Pfizer’s $43 billion acquisition of Seagen. That 2023 deal, once lauded as a cornerstone of Pfizer’s post-pandemic strategy, has since become a cautionary tale of timing, market saturation, and the dangers of betting on the wrong horse during a revenue cliff. As Lilly charts its path, the question looms: Is it successfully building a foundation for sustainable growth, or is it merely recreating the structural vulnerabilities that defined Pfizer’s recent struggles?

The Core Facts: A New Chapter in Oncology

Eli Lilly’s acquisition of Kelonia represents a significant pivot toward in vivo CAR-T cell therapy. By bringing Kelonia’s proprietary platform into its fold, Lilly aims to simplify the notoriously complex and expensive manufacturing processes that have historically hampered cell therapies.

This deal is not an isolated incident but part of a broader, multi-billion-dollar strategy. Alongside the Kelonia news, Lilly recently finalized a collaboration with Insilico Medicine potentially worth $2.75 billion, focusing on AI-originated preclinical oral therapeutics. These moves underscore a clear mandate from Lilly’s leadership: utilize the massive cash flows currently generated by metabolic disease treatments to dominate the future of oncology and precision medicine.

A Tale of Two Strategies: Chronology of the Deals

To understand the current sentiment, one must look at the divergent timelines of these two pharmaceutical giants.

The Pfizer Trajectory (2022–2024)

Pfizer’s acquisition spree was, by all accounts, a reactionary effort to deploy the massive windfall from its COVID-19 franchise. In 2022, Comirnaty and Paxlovid propelled the company to a record $100.3 billion in revenue. Sensing that this demand would evaporate, management moved quickly, acquiring Biohaven ($11.6B) and Global Blood Therapeutics ($5.4B), culminating in the $43 billion purchase of Seagen.

The strategy was predicated on the belief that these assets would provide a "new" core business. However, the timing was suboptimal. By the time the Seagen deal closed, the COVID-19 demand had cratered; revenue for 2023 plummeted to $58.5 billion. Pfizer found itself burdened with high debt and a portfolio that was not yet generating enough organic growth to offset the loss of its pandemic-era earnings.

The Lilly Trajectory (2025–2026)

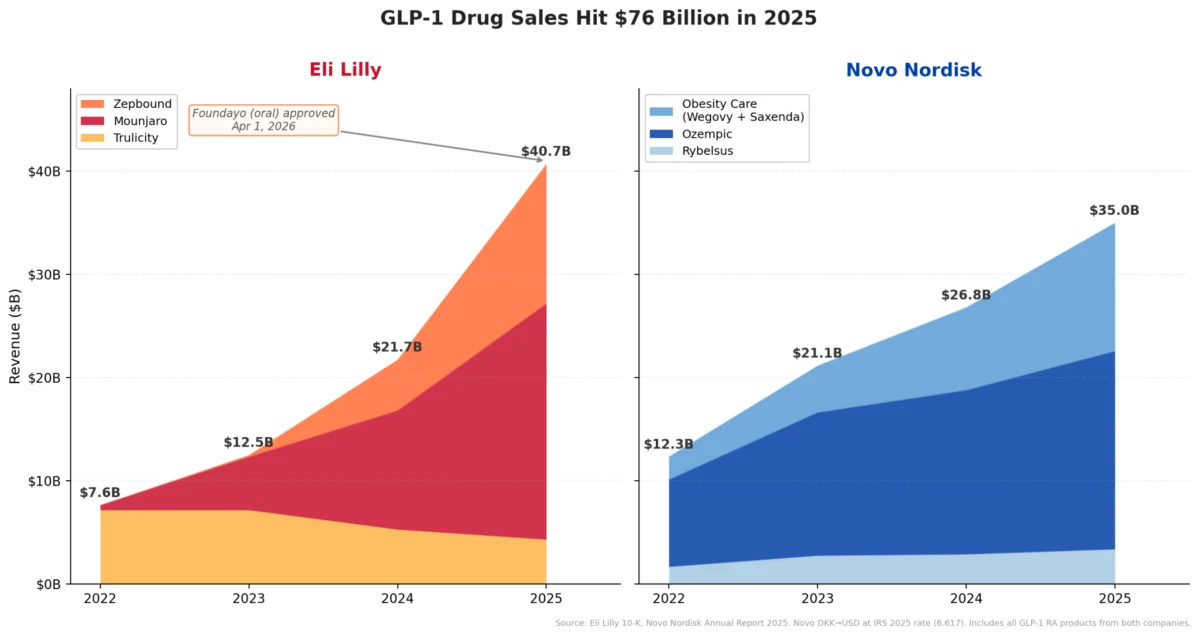

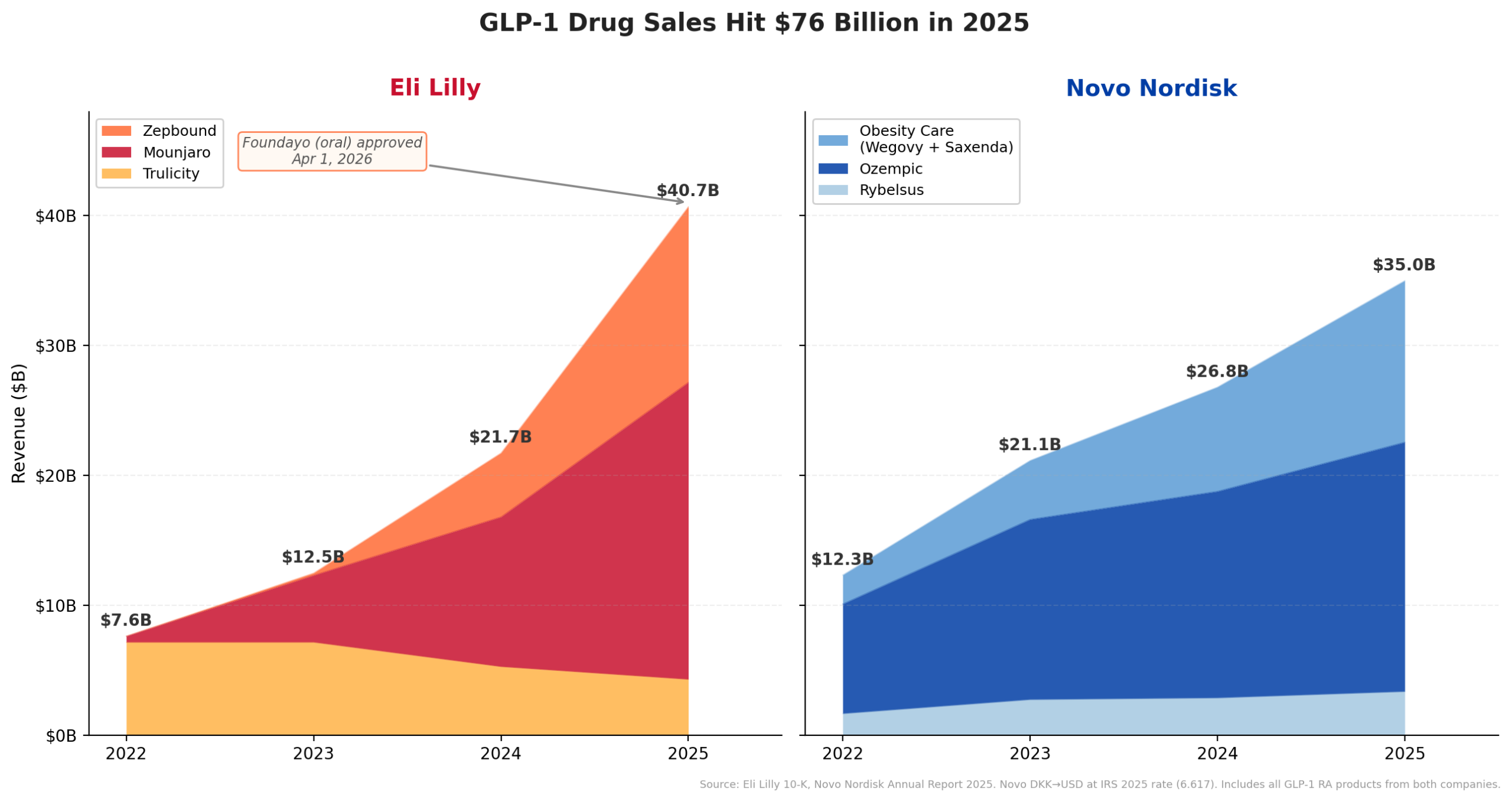

In contrast, Lilly’s current expansion is taking place while its flagship franchise is still accelerating. In 2025, tirzepatide alone generated approximately $36.5 billion of Lilly’s $65.2 billion total revenue. Unlike Pfizer, which was buying assets to replace falling revenue, Lilly is buying assets to diversify a growing one.

Furthermore, on April 1, 2026, the FDA approved Foundayo (orforglipron), Lilly’s oral GLP-1 for obesity. By securing approval under the National Priority Voucher program in record time, Lilly has effectively added an oral growth vector to its existing injectable portfolio, setting the stage for even greater market penetration as Medicare Part D coverage expands in July.

Supporting Data: The Growth Gap

The divergence between the two companies is best illustrated through their financial performance metrics.

Revenue Trajectory (2022–2025)

- Eli Lilly: Revenue has seen a staggering upward climb, with GLP-1 sales surging from $7.6 billion in 2022 to $40.7 billion by the end of 2025. The company’s guidance for 2026 sits between $80 billion and $83 billion.

- Novo Nordisk: Often seen as the primary rival, Novo has also seen success, moving from $12.3 billion to $35.0 billion in GLP-1 sales over the same period. However, current projections show a softening, with expected sales declines of 5% to 13% for 2026.

Portfolio Maturity

The fundamental difference in the deals lies in the "stage" of the assets:

- Pfizer’s Assets: Largely commercialized or late-stage. These assets (like Nurtec and Oxbryta) were designed to provide immediate revenue but required significant capital outlays that strained the balance sheet during a downturn.

- Lilly’s Assets: Predominantly early-stage, platform-based investments. By focusing on Phase 1 and Phase 2 assets—such as Kelonia, Morphic, and Scorpion—Lilly is building a pipeline that is cheaper to acquire today and holds significantly higher upside potential for the next decade.

Official Responses and Strategic Rationale

Lilly’s leadership has been transparent about the intent behind these acquisitions. In recent investor calls, the focus has remained on "durability." By investing in AI-driven drug discovery (Insilico) and next-gen cell therapy platforms (Kelonia), the company is essentially hedging its bets against a future where the current GLP-1 dominance might face generic competition or market saturation.

Analysts suggest that Lilly is avoiding the "Pfizer trap" by maintaining a disciplined debt-to-equity ratio. While Pfizer had to defer share buybacks to de-leverage its balance sheet after the Seagen acquisition, Lilly’s operating cash flow—$16.8 billion as of the last report—provides a significantly higher safety net, allowing them to fund these acquisitions without compromising core R&D or financial stability.

Implications: Can the Growth Last?

The implications of this strategy are profound for both the investor community and the healthcare sector.

1. The Risk of Platform-Based M&A

While early-stage platform bets (like Kelonia) offer higher potential ROI, they carry significant scientific risk. Unlike the established, FDA-approved drugs that Pfizer acquired, Lilly’s new assets may never reach the market. The success of this strategy rests entirely on the company’s ability to integrate these technologies into its existing clinical excellence framework.

2. The Competitive Landscape

Lilly’s ability to rapidly push drugs like Foundayo through the FDA’s National Priority Voucher program indicates a level of regulatory and operational efficiency that its competitors currently lack. By making its oral GLP-1 available through LillyDirect, the company is effectively cutting out traditional pharmacy benefit managers (PBMs) in certain channels, creating a direct-to-patient pipeline that could redefine pharmaceutical margins.

3. Avoiding the "One-Hit Wonder" Syndrome

The primary lesson from Pfizer’s post-COVID decline is that companies that rely on a singular, massive revenue source without a clear, mid-stage pipeline are highly vulnerable to market shifts. By aggressively acquiring early-stage technology, Lilly is intentionally "de-risking" its future. They are not waiting for their GLP-1 sales to peak; they are reinvesting those profits before the peak even arrives.

Conclusion: A More Durable Playbook?

Comparing Eli Lilly today to the Pfizer of 2023 is a study in financial timing and strategic foresight. While Pfizer was forced into an acquisition spree by the rapid evaporation of its COVID-19 revenue, Lilly is currently in the enviable position of being able to choose its targets from a place of strength.

The acquisition of Kelonia is not merely an oncology play; it is a signal that Lilly intends to lead the next generation of precision medicine. Whether this strategy will avoid the pitfalls that plagued Pfizer remains to be seen, but the data suggests that the "Lilly Playbook"—characterized by early-stage platform investments, high-margin oral alternatives, and disciplined balance sheet management—is fundamentally different. As the company prepares for its Q1 2026 earnings release on April 30, the market will be looking for confirmation that these investments are indeed the right engines to sustain the next decade of growth.

For now, Lilly appears to be the master of its own destiny, using its metabolic success not as a cushion to rest on, but as a launchpad for a much larger, more diverse future.