The landscape of American health insurance underwent a seismic shift in 2026. Following the expiration of enhanced premium tax credits, the Affordable Care Act (ACA) Marketplace has seen its most significant volatility since its inception. New data from the Kaiser Family Foundation (KFF) paints a concerning picture: a record-breaking spike in deductibles, a mass exodus from comprehensive silver-tier plans, and a looming threat of widespread coverage loss for millions of Americans.

As household budgets tighten under the weight of higher premiums and increased cost-sharing, the structural integrity of the ACA Marketplace is being tested. With enrollment potentially poised to drop by nearly five million people this year, policy experts are bracing for a ripple effect that could increase medical debt, reduce access to preventative care, and deepen the divide in healthcare affordability across the United States.

The Main Facts: A Financial Turning Point

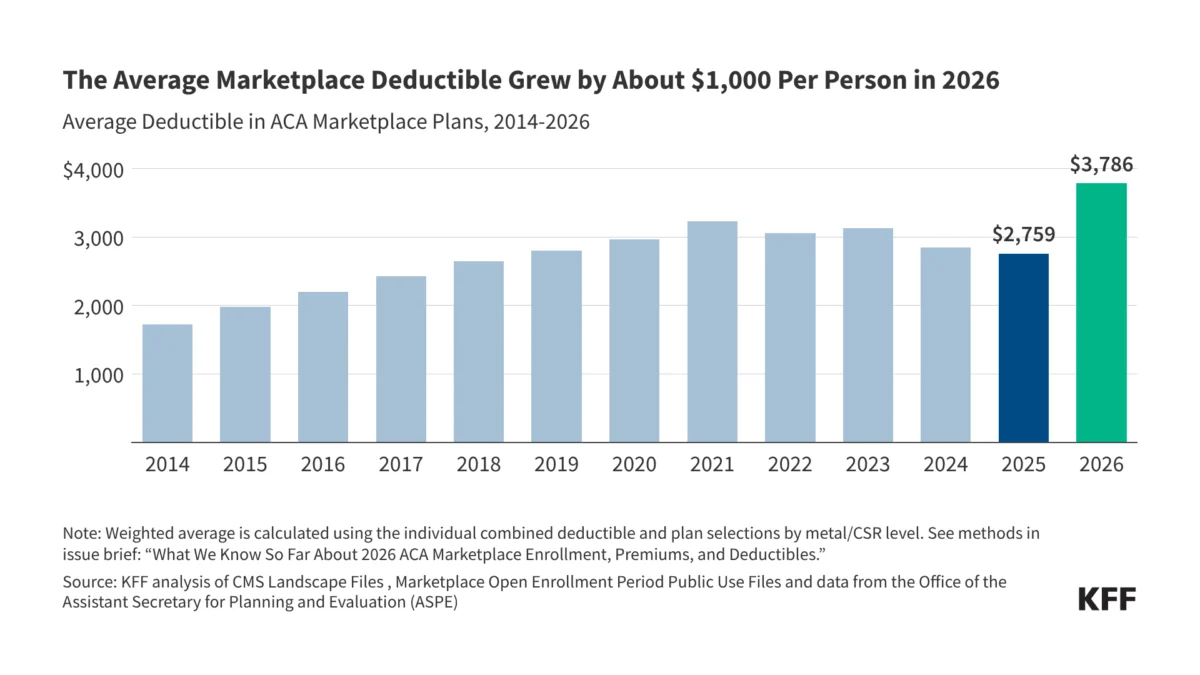

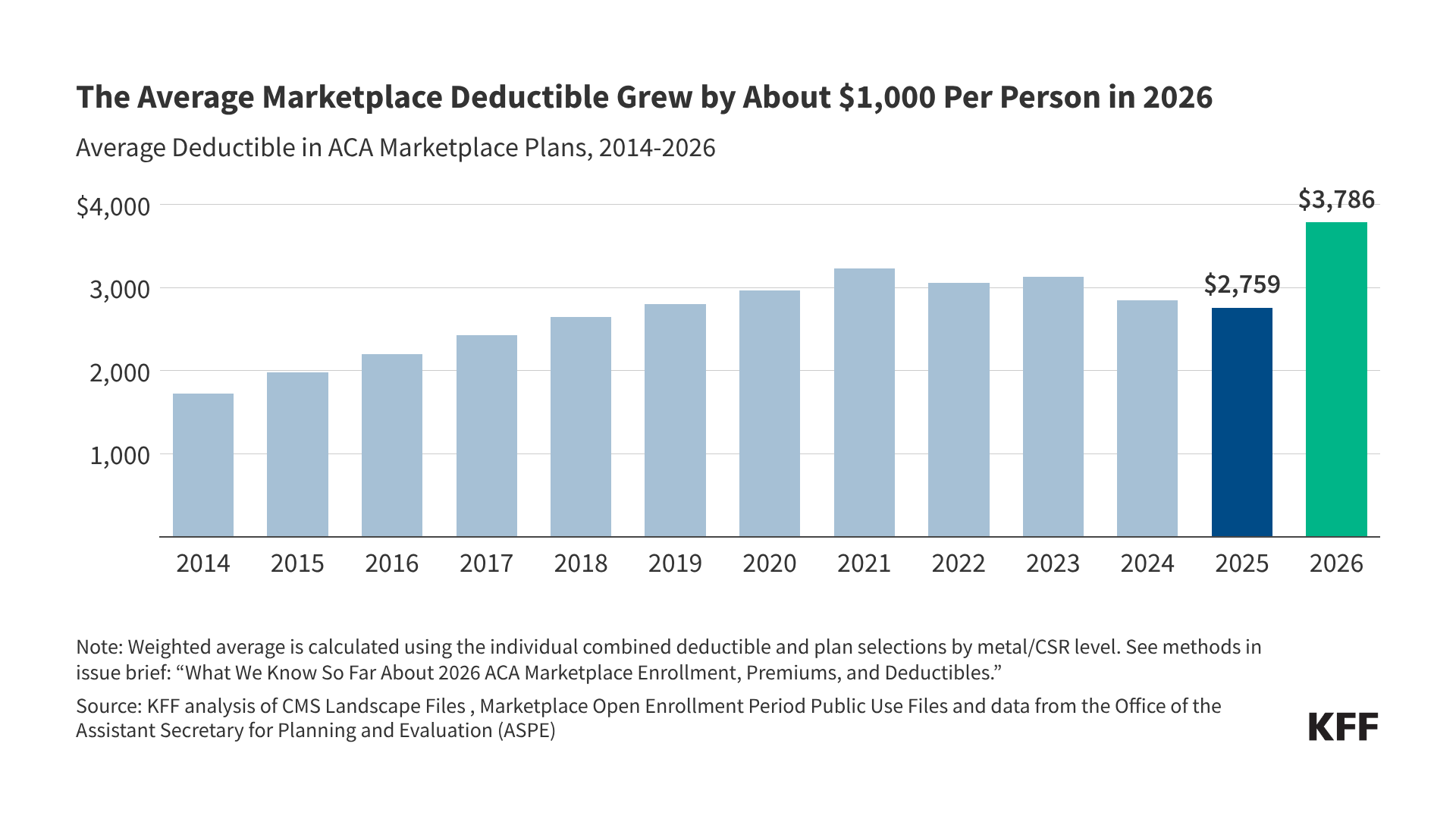

The primary driver of the 2026 volatility is the expiration of the enhanced premium tax credits, which had previously artificially suppressed costs for millions of enrollees. With these credits gone, the average ACA Marketplace deductible has surged by 37%, climbing from $2,759 in 2025 to $3,786 in 2026. This represents a staggering $1,027 increase for the average enrollee, a financial blow that has fundamentally altered consumer behavior.

The financial burden does not stop at the deductible. Monthly premium payments, which had been stabilized by the federal government, have jumped by an average of 58%, rising from $113 to $178. For millions of families living paycheck to paycheck, this sudden increase in fixed costs has rendered the previous standard of care—the "Silver" plan—effectively unaffordable.

Chronology: The Road to the 2026 "Subsidy Cliff"

To understand the current crisis, one must look back at the legislative trajectory of the ACA.

- 2021–2024: The American Rescue Plan Act and subsequent extensions provided robust, enhanced tax credits that lowered premiums to historic lows, regardless of income level. This led to record-shattering enrollment numbers, peaking at 22.3 million in 2025.

- Late 2025: As the expiration date for these credits approached, legislative gridlock in Washington D.C. prevented a renewal of the enhanced subsidies.

- Open Enrollment 2026: As the new year began, consumers were met with the harsh reality of "market-rate" premiums. The reemergence of the "subsidy cliff"—where individuals earning over 400% of the federal poverty level ($62,600 for an individual) face the full weight of insurance costs—began to force millions out of the system.

- Mid-2026: Projections now suggest a sustained "attrition phase," where many who managed to secure coverage during Open Enrollment will be forced to drop it mid-year as they fail to keep up with the new, higher monthly premium obligations.

Supporting Data: Shifts in Plan Selection

The data reveals a clear trend: when faced with higher costs, consumers are opting for "bare-bones" coverage, a move that exposes them to significant financial risk.

The Rise of Bronze Plans

Sign-ups for Bronze plans—which feature lower premiums but substantially higher out-of-pocket costs—have surged. Between 2025 and 2026, the share of total plan selections for Bronze plans jumped from 30% to 40%. In raw numbers, this accounts for an increase from 7.3 million to 9.2 million enrollees.

The Decline of Silver and CSR Plans

Conversely, Silver plans, traditionally the "gold standard" for middle-income families due to their balanced premium-to-deductible ratio, have hit an all-time low. Enrollment fell from 57% to 43%, a reduction of nearly four million people. Even more concerning is the drop in Cost-Sharing Reduction (CSR) silver plans. These plans, designed to reduce deductibles and copayments for low-income families, saw their share of the market fall to 37%—the lowest level since the inception of the ACA.

Regional Disparities

The impact has not been felt uniformly across the country. 41 states reported declines in Marketplace sign-ups. The most severe drops occurred in North Carolina (22%), Ohio (20%), and West Virginia (17%). Conversely, states that operate their own exchanges, such as California and Massachusetts, have demonstrated more resilience. These state-based exchanges have utilized supplemental state-funded subsidies and more aggressive outreach, acting as a buffer against the federal volatility.

Implications: The Human Cost of Market Correction

The shift away from comprehensive plans is not merely a statistical anomaly; it is a public health concern. Higher deductibles act as a barrier to care. When a patient is faced with a $3,786 deductible, they are statistically less likely to seek preventative screenings, manage chronic conditions, or pursue elective procedures until they become emergencies.

A KFF survey conducted just prior to the expiration of the credits found that 67% of Marketplace enrollees would be forced to cut spending on basic household necessities—such as groceries, rent, or utilities—if their health costs increased by just $1,000. That threshold has now been met or exceeded for the average enrollee.

Furthermore, the "subsidy cliff" has disproportionately affected the middle class. While individuals with incomes below the poverty line often retain access to safety-net programs, those in the middle-income bracket are increasingly finding themselves in a "coverage gap" of their own making: they earn too much to receive significant government assistance, yet too little to absorb the massive premium increases. This demographic accounted for nearly half of the total decline in enrollment.

Official Responses and Future Outlook

While federal officials have maintained that the ACA remains a "vital pillar" of American healthcare, the legislative silence regarding the expiration of the enhanced credits suggests a shift in political priority. Industry analysts at the Wakely Consulting Group warn that the worst is yet to come.

"We are looking at a potential 21.5% decline in total enrollment by the end of this calendar year," the report states. When accounting for the projected mid-year drop-offs due to unpaid premiums—a phenomenon known as "churn"—the individual market could see a total reduction of up to 26% compared to 2025.

What Lies Ahead?

The 2026 healthcare market is essentially in a state of forced retrenchment. Policy experts suggest three primary outcomes for the remainder of the year:

- Increased Medical Debt: As more enrollees move to high-deductible plans, the incidence of medical bankruptcy and unpaid hospital bills is expected to rise sharply.

- Increased Uninsured Rates: The "missing" five million people are unlikely to find affordable alternatives in the employer-sponsored market, likely leading to a net increase in the national uninsured rate.

- State-Level Innovation: Given the success of state-based exchanges in retaining enrollees, there is growing pressure for more states to decouple from the federal marketplace and develop bespoke, state-subsidized systems to insulate their residents from federal policy shifts.

Conclusion

The expiration of enhanced ACA subsidies has triggered a "correction" that is proving far more painful than many policymakers anticipated. By prioritizing fiscal austerity over subsidized stability, the current healthcare environment has traded short-term federal savings for long-term individual financial instability. As the year progresses, the focus will shift from enrollment numbers to health outcomes, and whether the American healthcare system can sustain such a drastic reduction in accessible coverage without suffering systemic damage.