In the high-stakes world of global biopharmaceuticals, the line between visionary expansion and costly overreach is often drawn by the timing of an acquisition. Eli Lilly and Company, currently riding an unprecedented wave of success fueled by its blockbuster GLP-1 receptor agonist franchise, has signaled its next major move: an agreement to acquire CAR-T innovator Kelonia Therapeutics in a deal valued at up to $7 billion.

As Lilly leverages its massive cash reserves to pivot toward the next frontier of genetic medicine and oncology, the industry is left with a burning question: Can Lilly avoid the “Pfizer trap”—the historical tendency for pharma giants to overspend on massive acquisitions just as their primary revenue drivers begin to wane?

The Main Facts: A Bold Leap into In Vivo CAR-T

The acquisition of Kelonia represents a strategic pivot for Lilly. While the company has historically dominated the metabolic space with tirzepatide (Mounjaro and Zepbound), the Kelonia deal signals a commitment to the next generation of oncology: in vivo CAR-T cell therapy. By bringing Kelonia’s proprietary platform into the fold, Lilly aims to simplify the complex, costly, and time-consuming process of traditional ex vivo CAR-T therapies—where patient cells are modified in a lab—by enabling the modification of cells directly within the patient’s body.

This deal is not an isolated incident. Alongside the Kelonia news, Lilly has solidified a $2.75 billion collaboration with Insilico Medicine, focusing on AI-originated preclinical oral therapeutics. These moves underscore a clear mandate from the C-suite: transform the massive windfall from obesity and diabetes treatments into a diversified, high-growth pipeline that extends well into the 2030s.

A Tale of Two Deal Waves: Chronology and Context

To understand the significance of Lilly’s current strategy, one must look back at the immediate post-pandemic era. Pfizer’s acquisition of Seagen for $43 billion in 2023 serves as the cautionary tale of the decade. Pfizer, flush with record-shattering cash from its COVID-19 vaccine (Comirnaty) and antiviral (Paxlovid), utilized its windfall to consolidate its oncology footprint.

However, the timing proved disastrous. By the time the Seagen deal was finalized, the COVID-19 revenue “bubble” had already begun to burst. Pfizer saw its revenue plummet from $100.3 billion in 2022 to $58.5 billion in 2023, a 42% contraction. The massive debt incurred to fund its deal-making spree coincided with a sharp decline in the very products that funded the acquisitions, leaving investors wary of the company’s capital allocation strategy.

Lilly, by contrast, is operating from a position of “offensive” strength. As of early 2026, its tirzepatide franchise is not merely stable; it is accelerating. With revenue guidance for 2026 projected at $80 billion to $83 billion, Lilly is deploying capital while its engine is at peak performance, rather than as a defensive maneuver to offset a collapsing business unit.

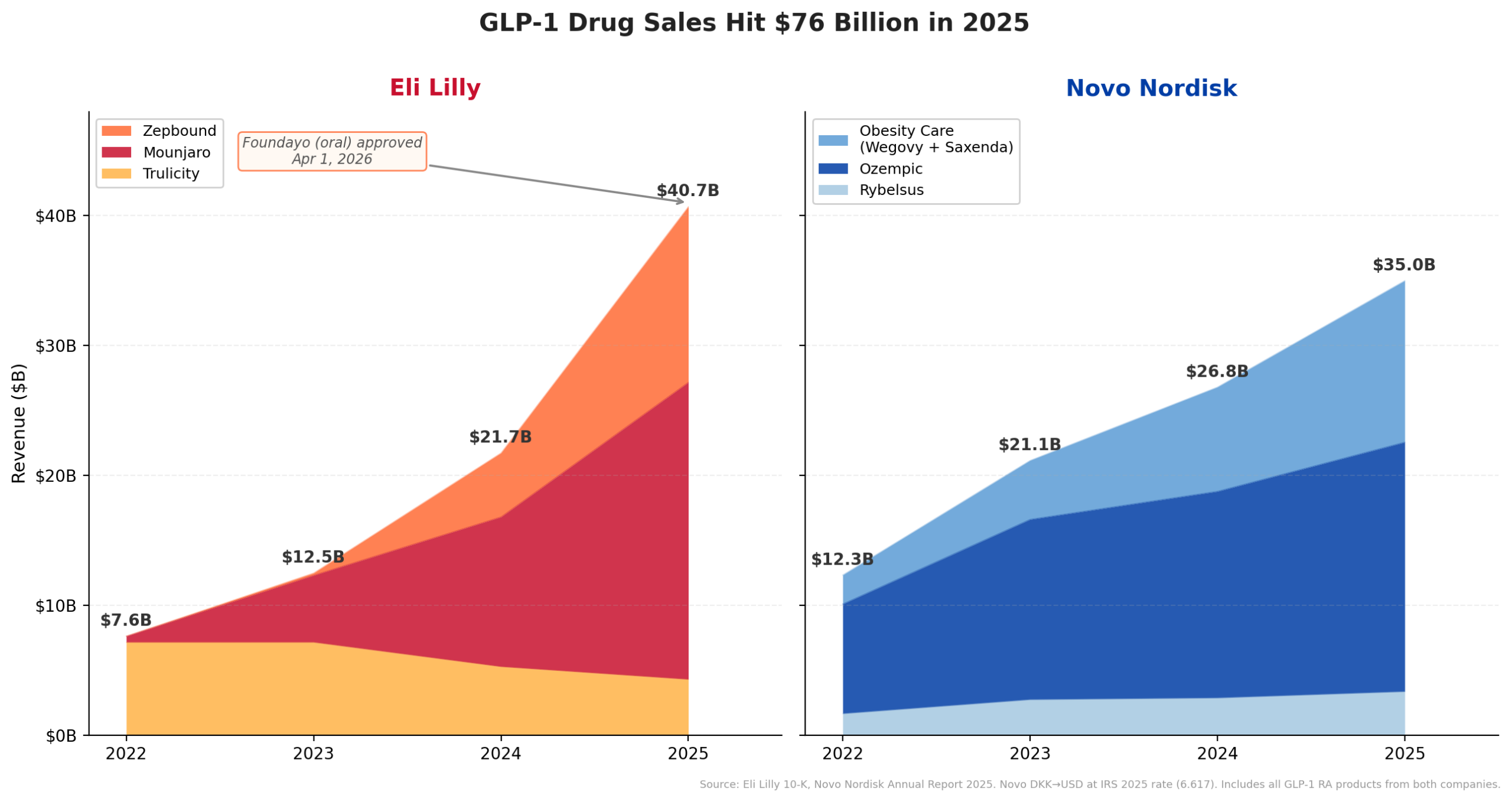

Data Analysis: The Engine of Growth

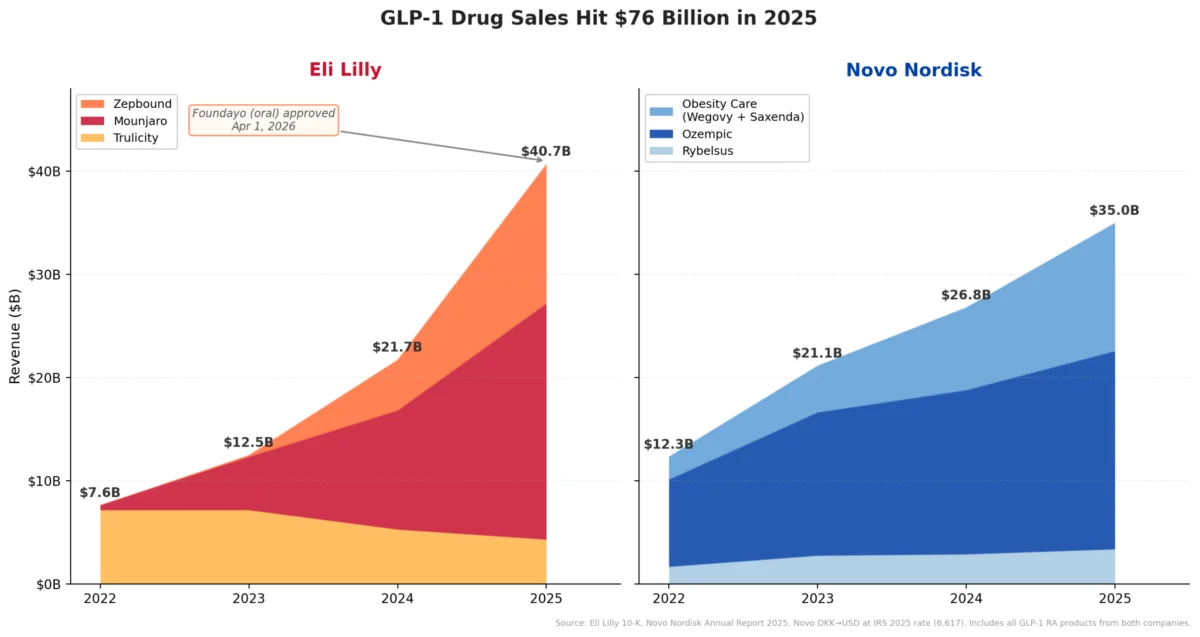

The disparity between the two companies’ financial trajectories is best captured by their GLP-1 performance. Between 2022 and 2025, Lilly’s GLP-1 revenue exploded from $7.6 billion to $40.7 billion. During the same period, Novo Nordisk—the industry’s other titan—saw its semaglutide portfolio grow from $12.3 billion to $35.0 billion.

Lilly’s growth curve is not only steeper but appears more durable, particularly with the recent FDA approval of Foundayo (orforglipron). Approved under the National Priority Voucher program just 50 days after filing, this oral GLP-1 therapy offers a critical growth vector that bypasses the supply-chain bottlenecks often associated with injectables. With a price point of $149/month and pending Medicare Part D coverage, Lilly is effectively capturing both the high-end and the mass-market segments of the obesity crisis simultaneously.

Comparative Financial Metrics (2025/2026 Snapshot)

| Metric | Eli Lilly | Pfizer |

|---|---|---|

| 2025 Revenue | $65.2 Billion | ~$58.5 Billion |

| Cash Engine | Tirzepatide ($36.5B) | COVID-19 Products (Declining) |

| Recent Deal Value | ~$18 Billion (Portfolio) | ~$60 Billion (Consolidated) |

| Acquisition Focus | Early-Stage (Ph 1/2) | Commercial/Late-Stage |

| Market Cap (2026) | $830B – $880B | ~$155 Billion |

Official Responses and Strategic Rationale

Lilly’s management team, led by CEO David Ricks, has maintained that their acquisition strategy is centered on "filling the gaps" of the future rather than buying revenue today. While Pfizer sought to buy existing commercialized products—such as those from Biohaven and Seagen—to plug immediate holes in their balance sheet, Lilly is aggressively hunting for platform technologies.

The acquisition of Kelonia, along with previous bets like Morphic ($3.2B), Scorpion ($2.5B), and Verve ($1.3B), prioritizes clinical-stage innovation over immediate commercial revenue. By focusing on Phase 1 and 2 assets, Lilly is aiming to build its own future blockbusters from the ground up, rather than paying a premium for mature assets that may be nearing their patent cliffs.

In recent investor communications, the company has emphasized that its financial posture remains robust. With $16.8 billion in operating cash flow and a clear path to sustained revenue growth, Lilly is in the rare position of being able to invest heavily in R&D and M&A without deferring shareholder returns or over-leveraging its balance sheet—a stark contrast to the de-leveraging posture Pfizer has been forced to adopt.

The Implications: Why This Strategy Differs

The primary risk for any pharmaceutical company engaged in a deal spree is "integration fatigue" and the loss of scientific focus. Pfizer’s integration of Seagen required a massive organizational restructuring that shifted resources away from other internal R&D programs.

Lilly’s strategy, however, appears to be "hub-and-spoke." By acquiring smaller, specialized firms like Kelonia, they are embedding highly specific expertise into their existing infrastructure. The collaboration with Insilico Medicine further highlights this; rather than trying to build an in-house AI engine from scratch, Lilly is outsourcing the high-risk, high-complexity innovation to partners, thereby maintaining its own operational agility.

Furthermore, the "oral" revolution represented by Foundayo changes the competitive landscape. By moving to an oral delivery method, Lilly is not just competing with Novo Nordisk; it is creating a new category of convenience that significantly lowers the barriers to patient adoption. This reduces the risk of "cannibalization" and ensures that as the market for weight-loss drugs matures, Lilly remains the primary beneficiary.

Conclusion: A New Blueprint for Pharma M&A

Lilly’s $7 billion bet on Kelonia is more than just a purchase of technology; it is a declaration of intent. While the industry is often wary of "mega-mergers" due to the specter of past failures, Lilly’s approach is fundamentally different. It is a calculated, aggressive, and highly timed deployment of capital.

If the past decade in pharma taught us anything, it is that cash is not a replacement for innovation. Pfizer attempted to buy its way out of a decline, whereas Lilly is using its success to buy its way into the next era of medicine. Whether this strategy will yield the anticipated long-term value remains to be seen, but for now, Eli Lilly has set a new gold standard for how a pharmaceutical giant can transform a temporary windfall into a permanent competitive advantage. As the market awaits the Q1 2026 earnings results on April 30, all eyes will be on whether this growth remains as sustainable as the company’s leadership suggests.