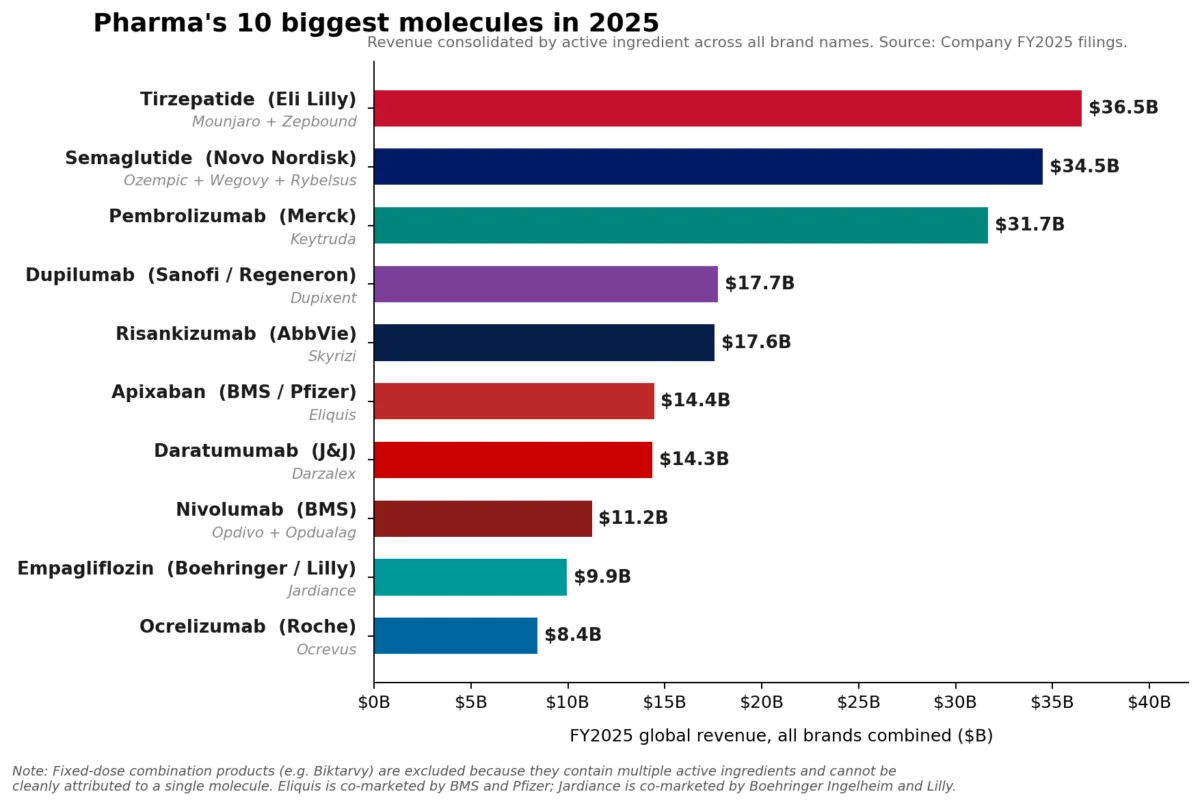

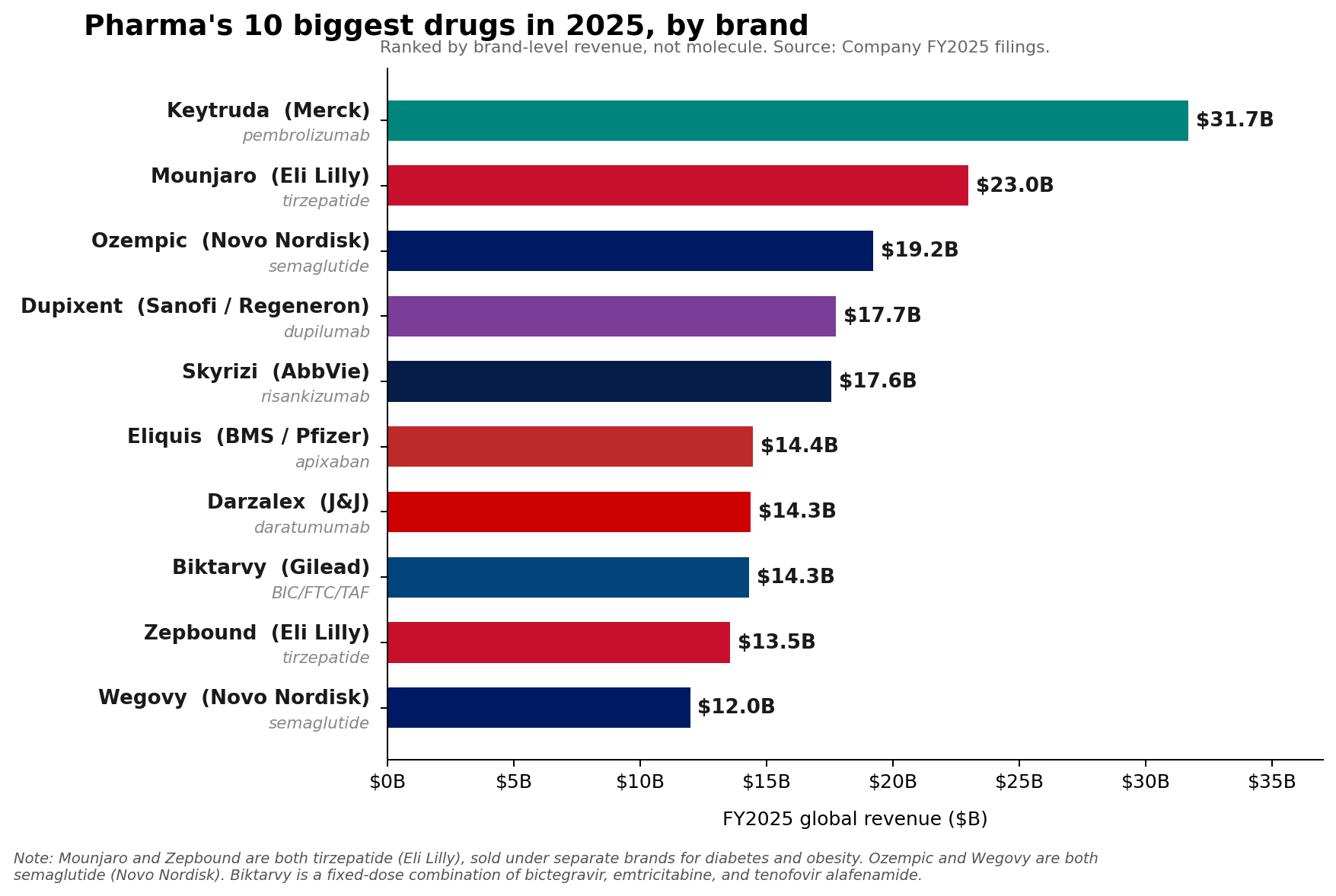

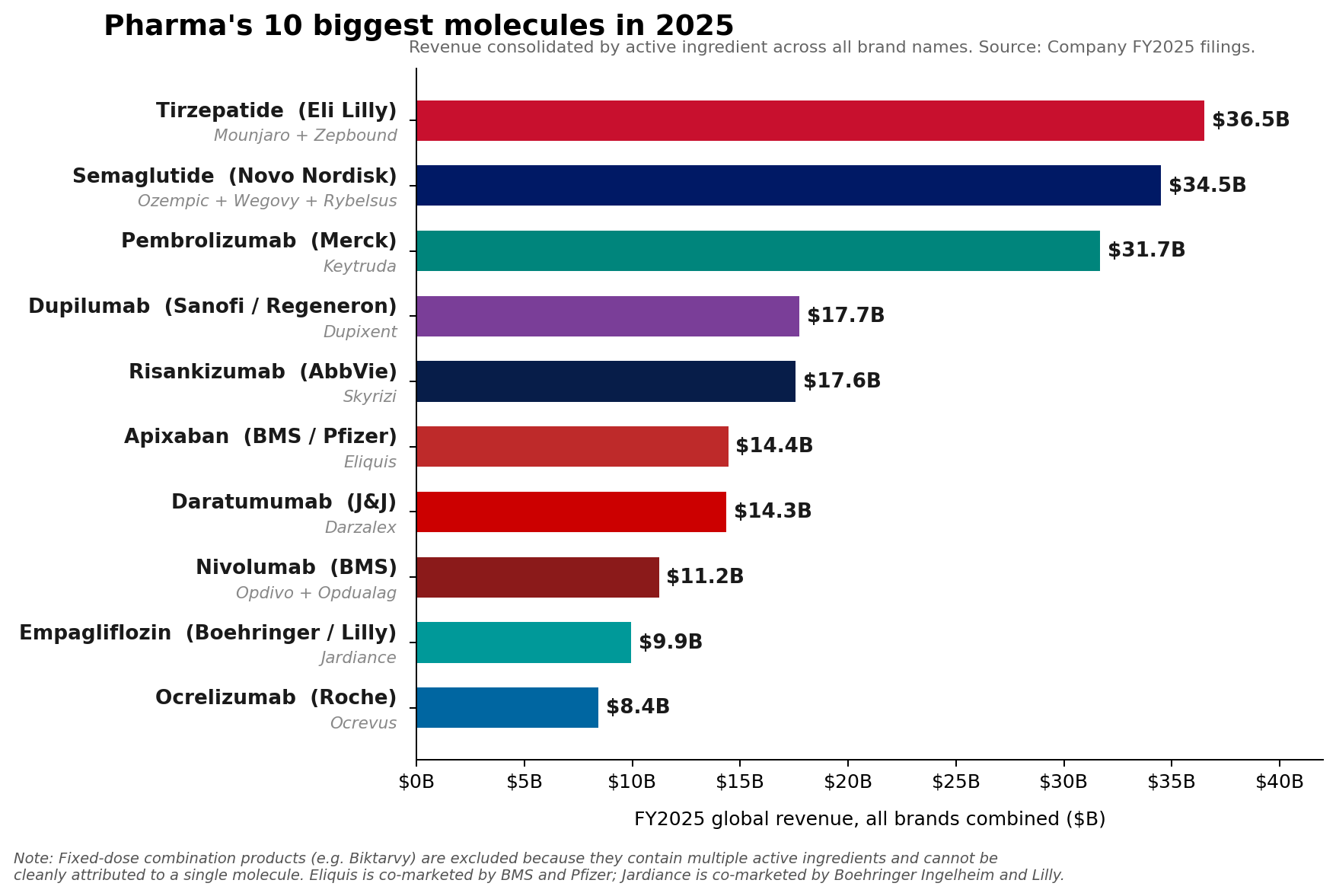

The pharmaceutical industry has reached a historic inflection point. For years, the oncology juggernaut Keytruda (pembrolizumab) has reigned supreme as the undisputed king of the pharmaceutical landscape. However, as of the close of Fiscal Year 2025, the narrative of industry dominance has shifted. While Merck’s Keytruda retains its title as the top-selling individual brand with a staggering $31.7 billion in revenue, it has been eclipsed at the molecular level by the combined weight of two massive metabolic franchises: Eli Lilly’s tirzepatide and Novo Nordisk’s semaglutide.

This realignment signals more than just a change in leadership; it marks the emergence of metabolic disease—specifically obesity and type 2 diabetes—as the primary engine of pharmaceutical growth. As the industry navigates this transition, the competitive landscape is becoming defined by a paradox: while the "GLP-1 gold rush" dominates headlines and capital allocation, the traditional pillars of oncology and immunology remain resilient, compounding growth in ways that suggest a more diverse, multi-polar future for the sector.

The Shift in Molecular Dominance

In FY2025, the market hierarchy underwent a structural reorganization. Eli Lilly’s tirzepatide franchise—encompassing both the diabetes-indicated Mounjaro ($22.965 billion) and the obesity-indicated Zepbound ($13.542 billion)—hit a combined revenue of roughly $36.5 billion. Simultaneously, Novo Nordisk’s semaglutide portfolio, anchored by Ozempic, Wegovy, and Rybelsus, reached an aggregate of approximately $34.5 billion.

Combined, these molecules represent a shift in the center of gravity for global healthcare spending. While Keytruda remains a vital, growing asset for Merck, its growth rate of 7%—though impressive for a drug of its maturity—is being outpaced by the explosive, demand-driven expansion of the GLP-1 receptor agonist class.

A Chronology of the 2025–2026 Transition

The transition from a mono-product dominance to a diversified "mega-franchise" model did not happen overnight. The following timeline illustrates the key milestones that set the stage for the current market environment:

- Q1–Q4 2025: The "Year of the GLP-1." Eli Lilly and Novo Nordisk struggled to keep pace with unprecedented global demand, leading to massive investments in manufacturing capacity and supply chain infrastructure.

- January 2026: Novo Nordisk officially launches the oral version of Wegovy, signaling a strategic shift toward user-friendly administration as the primary differentiator in a crowded market.

- February 2026: Merck reports FY2025 financial results, highlighting Keytruda’s $31.7 billion haul. CEO Rob Davis clarifies the company’s "hill, not a cliff" strategy regarding upcoming loss-of-exclusivity (LOE) concerns.

- April 1, 2026: A pivotal date for the industry. The FDA grants approval to Eli Lilly’s Foundayo (orforglipron), the first once-daily oral small-molecule GLP-1.

- April 6–9, 2026: Commercial availability of Foundayo begins, marking the next phase of the obesity market competition.

Supporting Data: The Resilience of Immunology

While GLP-1s command the spotlight, the data provided by the 2026 Citeline Pharma R&D Annual Review reveals a nuanced reality: the industry is not becoming a "GLP-1 monoculture."

Immunology remains a massive, compounding therapeutic category. AbbVie’s performance in 2025 serves as the primary case study for this durability. With Skyrizi generating $17.562 billion and Rinvoq adding $8.304 billion, AbbVie has successfully transitioned away from its historic reliance on Humira. Together, these two drugs account for nearly 42% of AbbVie’s total $61.16 billion annual revenue.

Other notable performers include:

- Sanofi: Dupixent continues its ascent, reaching €15.714 billion in annual sales.

- Novartis: Kisqali demonstrated a remarkable 58% growth rate, reaching $4.783 billion, underscoring that oncology remains a high-growth sector for targeted therapies.

According to Citeline, the total number of active compounds in the R&D pipeline has dipped across several categories; however, the immunological segment expanded by 20.6%. This indicates that pharmaceutical giants are doubling down on chronic, high-cost inflammatory conditions as a hedge against the volatility of the weight-loss market.

Official Responses and Strategic Guidance

The leadership at these pharmaceutical giants has been clear about their strategies for the coming fiscal year.

Merck’s "Hill" Strategy:

Merck CEO Rob Davis has been vocal in managing investor expectations regarding Keytruda’s eventual patent expiration. By framing the revenue decline as a "hill" rather than a "cliff," Davis emphasizes the company’s lifecycle management—specifically the development of subcutaneous formulations like QLEX. Despite this, Merck’s FY2026 revenue guidance of $65.5 billion to $67.0 billion fell short of aggressive Wall Street estimates, reflecting the market’s underlying anxiety about the post-Keytruda era.

Lilly’s Aggressive Expansion:

Lilly has guided to an ambitious $80 billion to $83 billion in 2026 revenue. The strategic importance of Foundayo cannot be overstated. By moving from injectables to a small-molecule oral pill, Lilly is attempting to capture a segment of the patient population that has previously been hesitant to initiate treatment due to needle phobia or lifestyle constraints. However, management remains cautious, noting that while Foundayo is a strategic "wildcard," the primary revenue growth in 2026 will likely still be driven by the existing momentum of Mounjaro and Zepbound.

Novo Nordisk’s Reality Check:

In contrast to Lilly’s optimism, Novo Nordisk has provided more conservative guidance for 2026, forecasting adjusted sales growth between negative 5% and negative 13% at constant exchange rates (CER). This guidance reflects the harsh realities of the current pharmaceutical environment: increased pricing pressure, intense competition from Lilly, and shifting U.S. market access dynamics.

Implications for the Future of Pharma

The implications of this data-driven landscape are threefold:

1. The Death of the "Blockbuster" Concept

We have moved past the era where a single drug can define a company’s entire valuation. Today, success is defined by "franchise dominance"—the ability to bundle multiple products (like Skyrizi and Rinvoq or Mounjaro and Zepbound) to create a moat that competitors cannot easily cross.

2. The Weight of Obesity R&D

The anti-obesity pipeline has seen a "gut-busting" 30.7% expansion, with 588 active compounds now in development. This is a staggering shift in capital allocation. For mid-sized biotech firms, the challenge is no longer just discovering a novel compound, but proving that it can compete with the massive, vertically integrated commercial infrastructure of Eli Lilly and Novo Nordisk.

3. The Pricing and Access Squeeze

The negative growth guidance from Novo Nordisk serves as a warning for the entire industry. As these drugs become "lifestyle" and chronic-management staples, the pressure from payers, government regulators, and pharmacy benefit managers (PBMs) will only intensify. The high margins that defined the early, supply-constrained phase of the GLP-1 era are likely to compress as the market matures and competition becomes commoditized.

Conclusion

The pharmaceutical industry is currently in a state of productive tension. On one side, we have the metabolic revolution, which is reshaping the top-line numbers of the industry’s largest players. On the other, we have the persistent, foundational growth of oncology and immunology, which continues to provide the stability required to fund high-risk, high-reward R&D.

As we look toward the remainder of 2026, the question is not whether GLP-1s will continue to dominate the headlines—they undoubtedly will—but rather which company can most effectively transition from the "growth at any cost" phase to the "sustainable profitability" phase. Merck’s attempt to manage its Keytruda transition, combined with the launch of Foundayo and the continued expansion of AbbVie’s immunology engine, suggests that the next decade will be defined not by a single dominant drug, but by the battle for market share within highly sophisticated, multi-billion-dollar therapeutic franchises.

For investors, clinicians, and patients alike, the landscape has never been more dynamic, nor more challenging to navigate. The "Pharma 50" of 2026 is a testament to an industry that, despite the inevitable cycle of patent cliffs and regulatory scrutiny, remains remarkably adept at reinventing itself.