By Jonathan Gardner | Published July 8, 2026

In a strategic maneuver that highlights the persistent allure of the Chinese pharmaceutical market despite escalating geopolitical headwinds, British pharmaceutical titans AstraZeneca and GSK have announced a fresh series of collaborative agreements with domestic Chinese counterparts. These deals, disclosed on Wednesday, signal a deepening integration between U.K. drugmakers and China’s rapidly maturing biotech ecosystem, even as Western lawmakers and regulatory bodies increase their scrutiny of such cross-border alliances.

The moves come at a precarious time for global life sciences companies. With the United States and other Western nations expressing growing concern over intellectual property security and supply chain dependencies, the decision by AstraZeneca and GSK to expand their footprints in China represents a calculated bet on the long-term potential of the world’s second-largest pharmaceutical market.

Main Facts: The New Partnerships

The announcements center on two distinct, yet complementary, strategies: direct drug development and commercial market penetration.

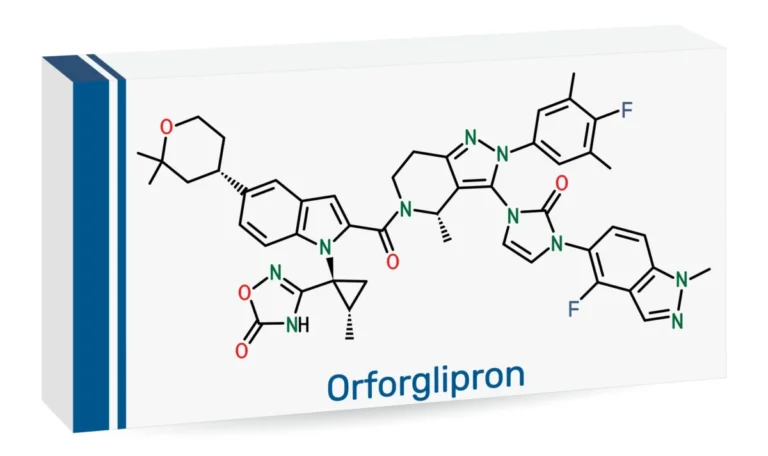

AstraZeneca, long the most prominent Western player in the Chinese pharmaceutical landscape, has entered into a licensing agreement for TQC3721, a promising respiratory candidate currently under development by Sino Biopharmaceutical. The drug is classified as a PDE 3/4 inhibitor, a therapeutic class that has generated significant interest in the global medical community for its potential in treating chronic obstructive pulmonary disease (COPD).

Simultaneously, GSK has formalized an alliance with Sino to bolster the distribution and commercialization of its established respiratory portfolio within China. Under the terms of this deal, Sino will take on the mantle of importing, promoting, and distributing GSK’s flagship respiratory medicines, Trelegy and Anoro. By leveraging Sino’s extensive domestic network, GSK aims to accelerate the adoption of these therapies among China’s massive patient population.

Chronology: A Deepening Relationship

The latest deals are not isolated events but rather the latest chapters in a long-running narrative of investment and collaboration.

- Mid-2024: AstraZeneca began aggressively diversifying its China strategy, moving beyond mere sales to include significant investments in local R&D infrastructure.

- Late 2025: Merck & Co. set a high-water mark for the respiratory sector by acquiring Verona Pharma for $10 billion, validating the potential of PDE 3/4 inhibitors—the same class of drug AstraZeneca has now licensed.

- Early 2026: AstraZeneca and its frequent collaborator, CSPC Pharmaceutical Group, deepened their existing alliances, further solidifying AstraZeneca’s position as a local powerhouse.

- July 8, 2026: Both AstraZeneca and GSK announce their latest strategic alignments with Sino Biopharmaceutical, marking a significant consolidation of U.K.-Chinese pharmaceutical interests.

Supporting Data: Why Respiratory Medicine Matters

The focus on respiratory health is not incidental. As global populations age and environmental factors continue to impact lung health, the market for COPD and asthma treatments is ballooning.

For AstraZeneca, the licensing of TQC3721 is a tactical play. Clinical data from a Phase 2 study in China demonstrated that the addition of TQC3721 to standard-of-care therapies significantly improved lung function compared to conventional treatments and placebos. Given the high prevalence of respiratory disease in the region, the potential for a "best-in-class" therapeutic is substantial.

GSK’s focus is equally data-driven. The company is seeking to maximize the revenue potential of its existing blockbuster drugs:

- Trelegy: In 2025, Trelegy generated global sales of approximately £3 billion ($3.9 billion), with roughly 16% of that revenue originating outside the U.S. and European markets.

- Anoro: GSK recorded £542 million ($714 million) in global sales for Anoro in 2025, with 18% of those sales coming from emerging territories outside of the U.S. and Europe.

By handing over the logistics and promotional heavy lifting to a domestic player like Sino, GSK is aiming to capture a larger share of the "untapped" 82% of these products’ respective markets, specifically by overcoming the regulatory and distribution hurdles that often plague foreign firms in China.

Official Responses and Strategic Intent

Executives from both sides of the agreements have been quick to emphasize the mutual benefits of these collaborations.

Sino Biopharmaceutical issued a formal statement highlighting the global aspirations of the partnership, noting that the deal is designed to "maximize the potential clinical and commercial value of this potential best-in-class medicine to benefit more patients worldwide." The phrasing is critical; it suggests that the partnership is not merely intended for the Chinese market but is a launchpad for bringing Chinese-developed innovations into the global fold.

AstraZeneca has maintained a consistent narrative regarding its China strategy. Having already committed $15 billion toward drug discovery, research, and local manufacturing facilities, the company views China as an essential hub of global innovation. Their leadership maintains that the ability to tap into Chinese scientific talent and clinical infrastructure is a competitive advantage that outweighs the geopolitical risks.

Implications: A High-Stakes Balancing Act

The implications of these deals extend far beyond the balance sheets of AstraZeneca and GSK. They represent a litmus test for the future of "globalized" pharmaceutical research.

1. The Regulatory Tightrope

In the United States, lawmakers are increasingly concerned about the flow of capital and data into the Chinese biotech sector. Legislation aimed at restricting partnerships with "biotech companies of concern" is currently being debated in various committees. AstraZeneca and GSK’s expansion in China may trigger further scrutiny from U.S. regulators, who worry that these partnerships could indirectly facilitate the transfer of critical dual-use technology or sensitive genetic data.

2. The Shift in R&D Power

Historically, the flow of innovation was unidirectional: from Western labs to global markets. These deals suggest a reversal. By licensing a drug developed in China (TQC3721) and relying on a Chinese partner to scale Western brands, U.K. pharma is acknowledging that the Chinese pharmaceutical ecosystem is no longer just a "market" but a "generator."

3. Supply Chain Resilience

By manufacturing locally, AstraZeneca and GSK are hedging against supply chain disruptions. Should trade tensions escalate, having a domestic Chinese manufacturing presence ensures that their medicines remain available to the Chinese public, insulating them from potential export bans or tariffs that could disrupt shipments from Europe or the U.S.

4. Competitive Pressure

For competitors who have been more cautious about entering the Chinese market, the success of these U.K. giants could serve as a catalyst. If AstraZeneca and GSK succeed in capturing significant market share while navigating the complex regulatory environment, it may force a reassessment of "China-light" strategies currently favored by other multinational pharmaceutical companies.

Conclusion

As the global pharmaceutical landscape undergoes a period of profound restructuring, the actions of AstraZeneca and GSK highlight the tension between commercial necessity and geopolitical reality. While the risks of operating in China have never been higher, the potential rewards—access to a massive, aging population and a burgeoning R&D infrastructure—are simply too great for these companies to ignore.

The coming years will likely determine whether these partnerships are models for a new era of collaborative global medicine or if they are the last vestiges of an era of unfettered international pharmaceutical integration. For now, the U.K. giants remain committed to their course, betting that clinical efficacy and market scale will ultimately supersede the political friction of the day. As these new alliances take root, the entire industry will be watching closely, mindful that the cost of failure in this market could be measured not just in dollars, but in the loss of one of the world’s most vital growth engines.