By Financial Policy Desk

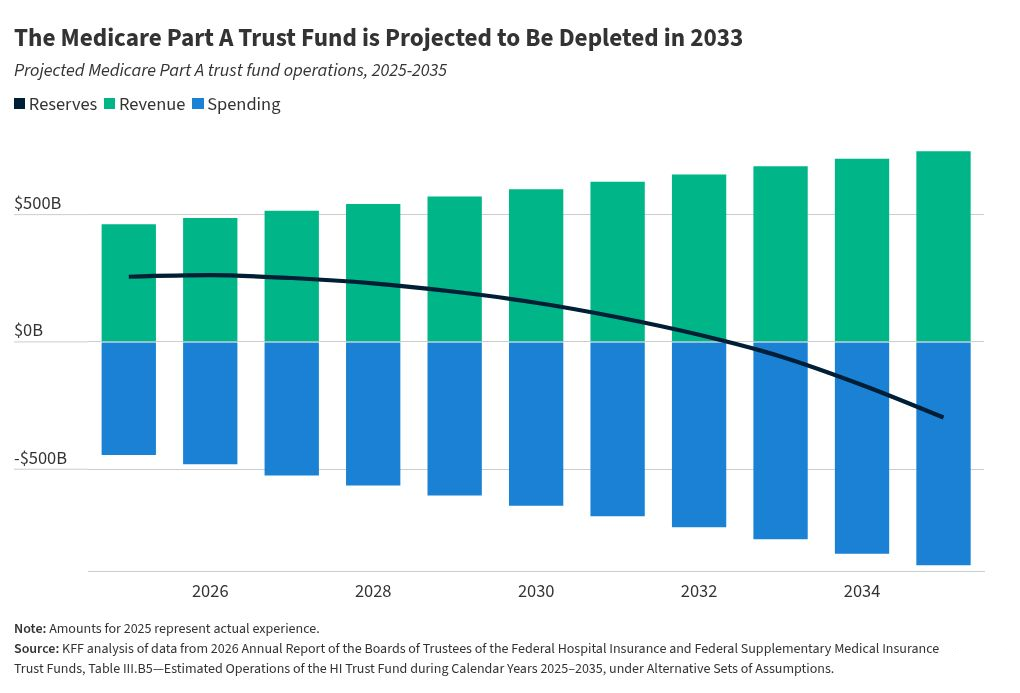

On June 9, 2026, the Medicare Trustees released their annual report on the financial health of the nation’s premier health insurance program for seniors and individuals with disabilities. The report paints a picture of a system in transition, characterized by rapidly shifting delivery models, the emergence of high-cost specialty pharmaceuticals, and a persistent fiscal countdown. With the Medicare Part A trust fund—the backbone of inpatient hospital coverage—now projected to be depleted by the second quarter of 2033, policymakers and stakeholders are once again forced to confront the structural pressures facing the program.

Main Facts: A System Under Fiscal Pressure

The core finding of the 2026 report is the revised depletion date for the Hospital Insurance (Part A) trust fund. The Trustees now estimate that reserves will be exhausted in 2033, one quarter earlier than last year’s estimate. This acceleration is primarily attributed to downward revisions in projected Social Security tax revenue, a consequence of recent legislative changes under the 2025 budget reconciliation bill (H.R. 1).

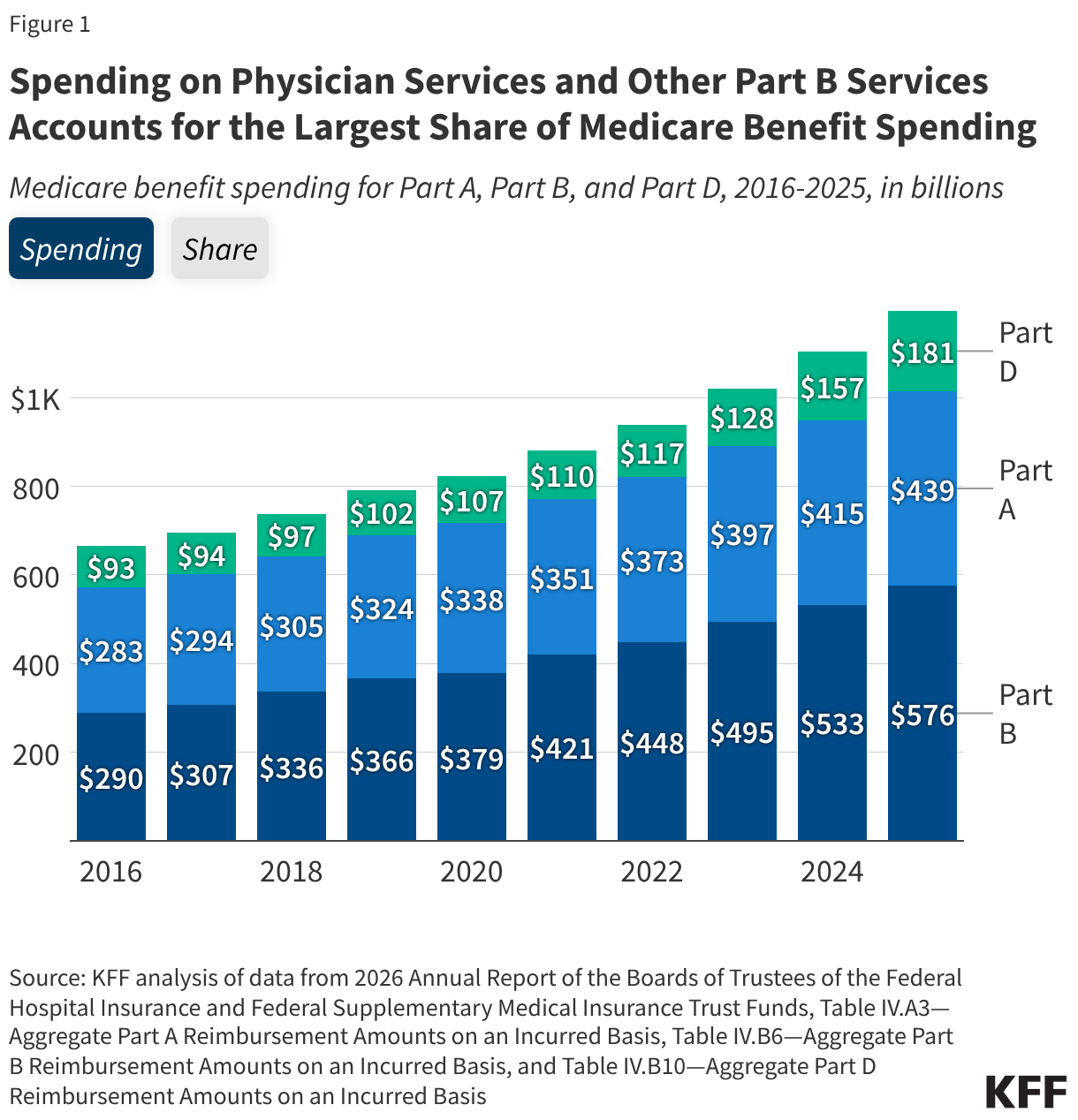

The report confirms that Medicare is no longer simply a program for acute hospital stays; it is increasingly defined by outpatient services, complex drug regimens, and the massive expansion of the Medicare Advantage (MA) private insurance market. In 2025 alone, total Medicare benefit payments reached a staggering $1.2 trillion—nearly double the expenditure of a decade prior. As the program matures, the balance of power between traditional Medicare and private managed care continues to tilt, with over half of all Medicare spending now flowing through Medicare Advantage plans.

Chronology: A Decade of Spending Transformation

To understand the current fiscal outlook, one must look at the historical trajectory of Medicare spending.

- 2016–2020: The program saw a steady transition as practice patterns shifted. Inpatient hospital services, once the undisputed titan of Medicare spending, began to decline as a percentage of total costs. This was driven by advancements in surgical technology and a clinical move toward outpatient care.

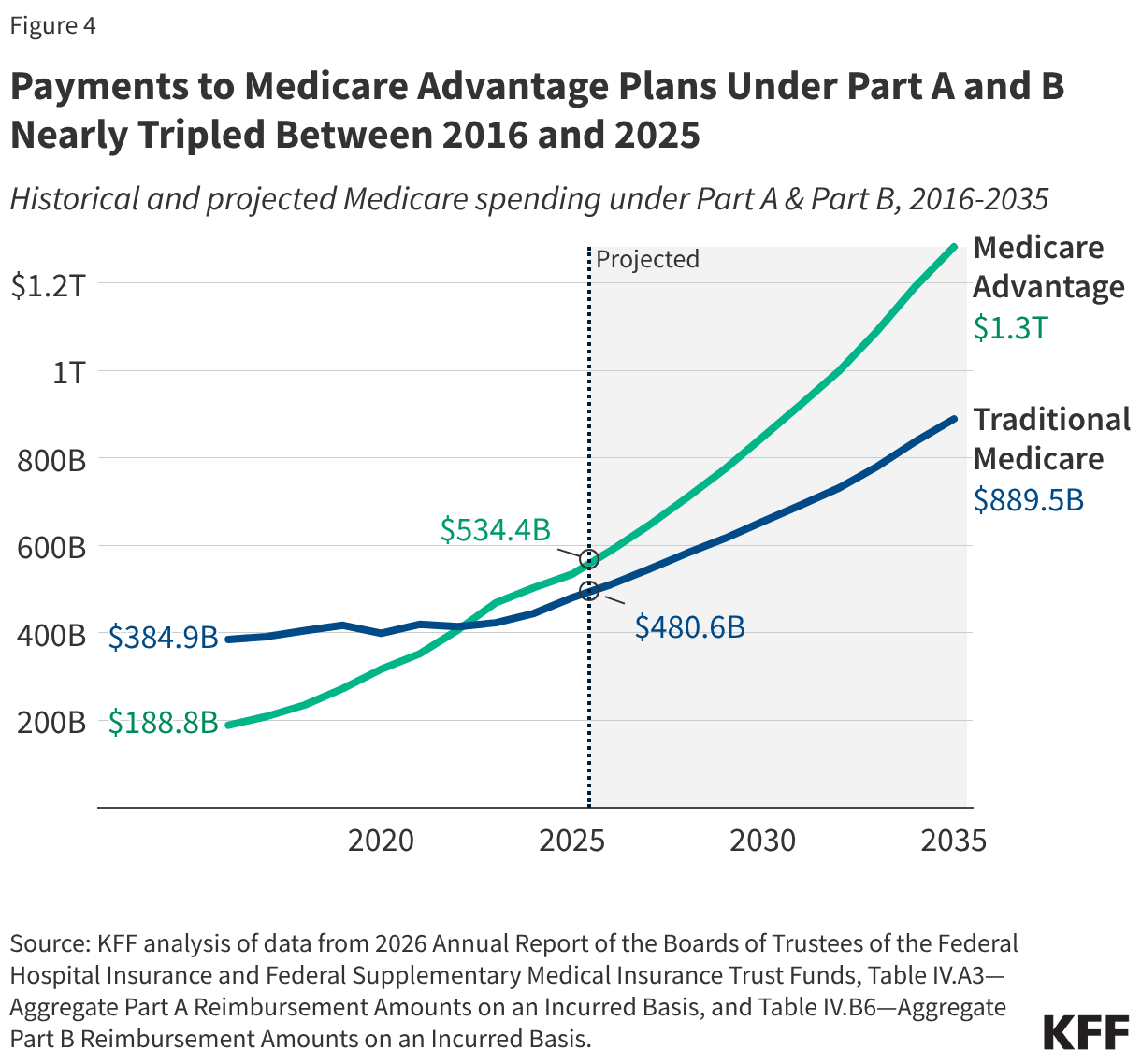

- 2021–2024: The Medicare Advantage market surged, with enrollment rates climbing from roughly one-third of eligible beneficiaries to over 54%. During this period, federal payments to private plans ballooned as enrollment grew and coding intensity—the practice of documenting sicker patients to secure higher risk-adjusted payments—became a focal point of federal oversight.

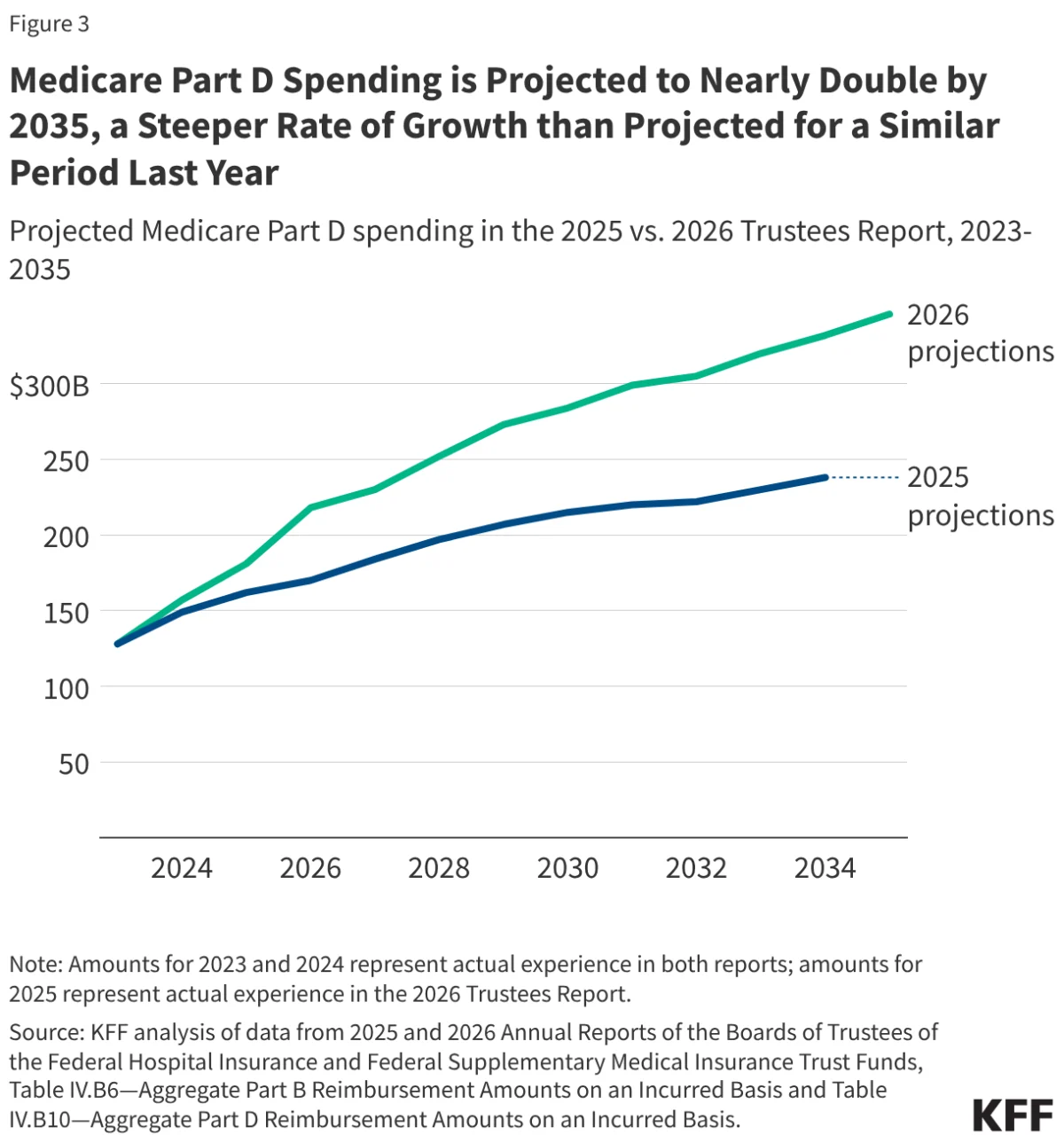

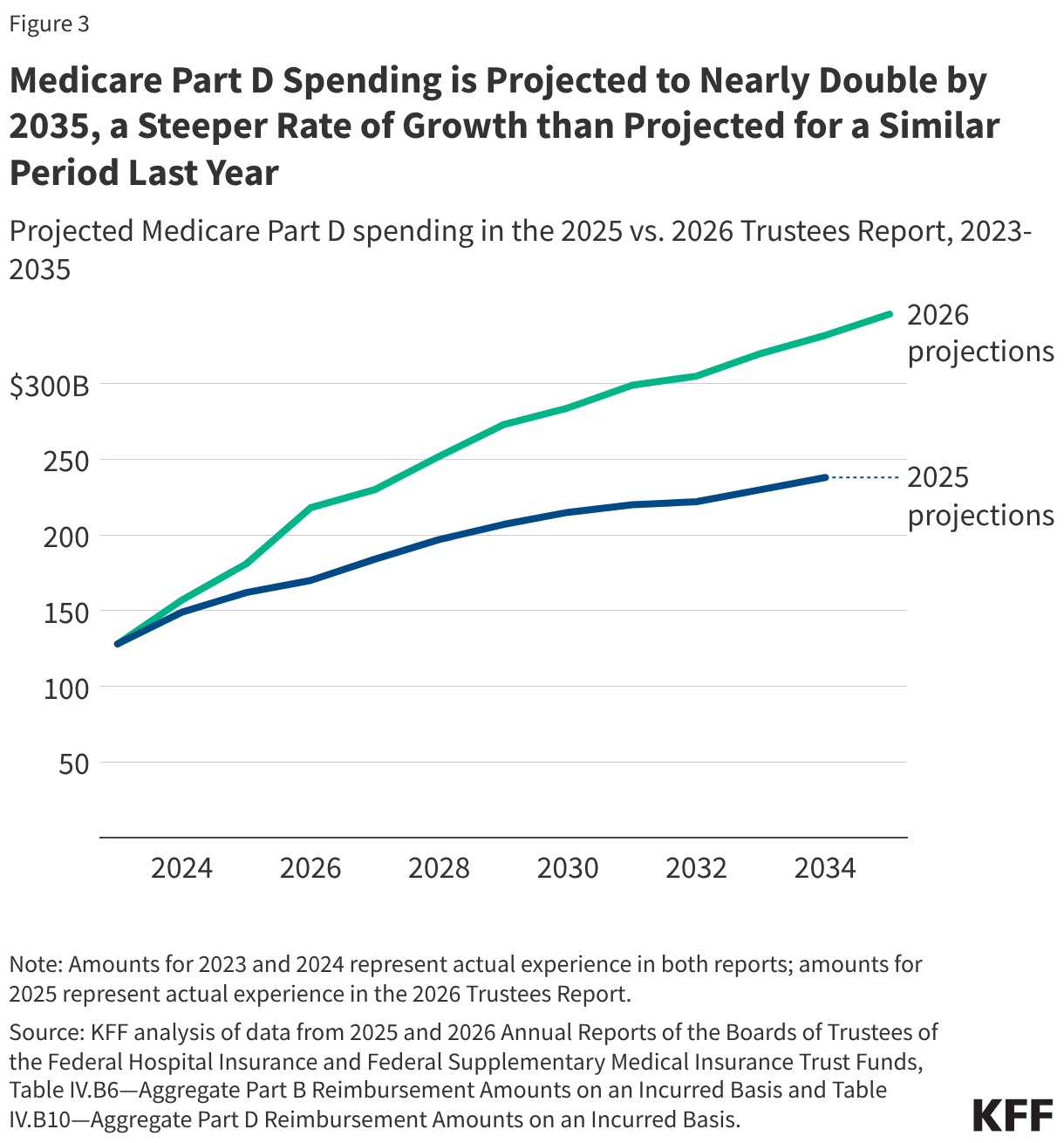

- 2025: A landmark year where Medicare benefit payments hit $1.2 trillion. The Part D prescription drug benefit, previously a stable 12–13% of total spending, jumped to 15%, signaling the beginning of an era defined by high-cost specialty drugs and GLP-1 medications.

- 2026 and Beyond: The current projection window forecasts a near-doubling of Part D spending by 2035, with Medicare Advantage spending expected to command 59% of all Part A and Part B outlays within the same timeframe.

Supporting Data: The Breakdown of Benefit Spending

The data provided by the Trustees reveals a stark shift in where federal dollars are being directed.

Part B Dominance: Physician services, outpatient care, and physician-administered drugs (all under Part B) now account for 48% of total benefit spending. This has been the dominant category since 2015. Conversely, Part A services—inpatient hospital care, skilled nursing, and hospice—have seen their share of the pie shrink from 43% in 2016 to 37% in 2025.

The Traditional Medicare vs. Advantage Split: In traditional Medicare, inpatient hospital services remain the largest single cost category, representing 33% of that specific bucket. However, the Medicare Advantage sector has effectively outpaced the traditional program in total federal funding, receiving $534 billion in 2025. The Trustees noted that Medicare pays roughly 14% more per enrollee in the private Advantage system than it would for that same individual in traditional Medicare—a "premium" that totaled $76 billion in additional spending for the 2026 calendar year alone.

The Part D Trajectory: The projection for prescription drug spending is perhaps the most volatile element of the report. The Trustees anticipate an average annual growth rate of 6.7% through 2035, significantly higher than the 4.8% projected just one year ago. This increase is driven by the utilization of high-cost specialty medications, the redesign of the Part D benefit (which shifted more financial liability to the federal government), and legislative exemptions for certain orphan drugs.

Official Responses and Policy Drivers

The Medicare Trustees, in their analysis, highlighted specific legislative actions that have altered the fiscal landscape. The 2025 budget reconciliation bill (H.R. 1) is a significant point of discussion. While the legislation sought to manage federal deficits, its impact on revenue sources for the Part A trust fund has been negative, contributing to the earlier-than-expected depletion date.

Furthermore, the Trustees pointed to the "pharmacy price concessions" policy. While intended to lower point-of-sale costs for beneficiaries, the policy has had the unintended side effect of reducing rebate revenue for Part D plans. To compensate for this, federal subsidies for these plans have increased, placing additional pressure on the Treasury.

However, the report also notes that these costs are being partially mitigated by the Inflation Reduction Act (IRA). The implementation of drug price negotiations and inflation rebates is providing a "cushion," slowing what would otherwise be an even more aggressive surge in drug spending.

Implications: The Burden on the Beneficiary

The most pressing implication of these fiscal trends is the direct impact on the American senior. Medicare is not an island; it is tethered to the economic reality of its participants.

Rising Premiums and Deductibles: For 2027, the Trustees project the monthly Part B premium to rise to $210, up from $203 in 2026. While a percentage-based increase might seem incremental, it follows a sharp 9.7% hike between 2025 and 2026. Similarly, deductibles for both Part A and Part D are slated to increase.

The Affordability Gap: For millions of Americans, these costs are not trivial. With seven million beneficiaries already spending more than 10% of their annual income on Part B premiums alone, there is growing concern that the program is becoming unaffordable for those with fixed incomes. As the gap between healthcare inflation and personal income growth widens, the pressure on the federal government to intervene—either through subsidies or structural reform—will likely intensify.

The Solvency Crisis: The 2033 deadline serves as a political "ticking clock." When the Part A trust fund reaches insolvency, it does not mean the end of Medicare; however, it does mean that the program will only be able to pay for the services it can afford with the tax revenue coming in that year. This would necessitate a choice: either a sharp reduction in payments to hospitals and nursing homes—which would likely lead to access issues for patients—or a significant injection of general tax revenue, which would require legislative action from Congress.

Conclusion: A Call for Long-Term Reform

The 2026 Medicare Trustees Report is more than a collection of financial statistics; it is a roadmap of the challenges inherent in providing universal healthcare to an aging population. As the shift toward Medicare Advantage continues and the cost of pharmaceutical innovation rises, the traditional funding mechanisms of the 20th century are showing their age.

Whether the solution lies in further empowering the government’s drug negotiation authority, reforming the risk-adjustment models that drive Medicare Advantage payments, or increasing payroll taxes to bolster the Part A trust fund, the path forward is clear. Without significant policy intervention before 2033, the Medicare program will face an era of forced austerity that could fundamentally alter the quality and accessibility of care for millions of Americans. For now, the report stands as a formal warning: the fiscal horizon is closing, and the time for sustainable, long-term planning is dwindling.